Are American value stocks, which have become junk stocks, not far from bottoming out and reversing?

分析认为,关键价值股指标已跌至 200 日均线附近,这在历史上是一个明显的反弹信号;美联储很可能在年内开启降息周期,美国经济加速恢复的预期升温,同样有利于价值股反弹。

美国价值股近日对投资者的吸引力无异于垃圾股,但市场分析显示,它们可能要触底反弹了。

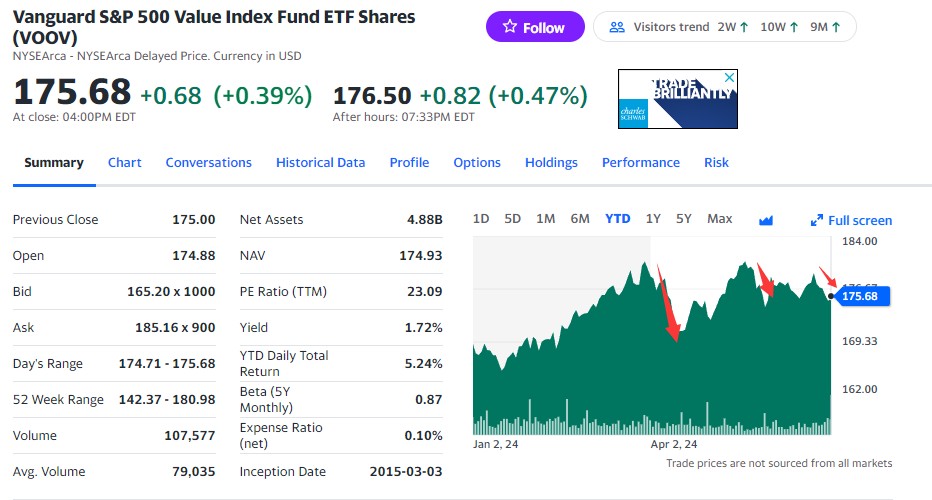

追踪标普 500 指数中市盈率较低股票的先锋标普 500 价值指数基金 ETF(VOOV),今年以来的涨幅仅为 5%,这与准普 500 指数整体 15% 的涨幅相比,表现明显较差。尽管这些价值股普遍被认为价格合理或低估,但它们在股市中的表现甚至没有达到大盘的水平。

实际上,该价值基金曾有过几次短暂的反弹,但每当价格达到 180 美元时,总会遭遇一波抛售。截止发稿,周二下午的价格是 175.68 美元。

分析认为,该关键价值股指标已跌至 200 日均线附近,这在历史上是一个明显的反弹信号;美联储很可能在年内开启降息周期,美国经济加速恢复的预期升温,同样有利于价值股反弹。

22V Research 分析师 Dennis DeBusschere 在最新公布的报告中列出了届时可能会反弹的价值股,包括通用汽车、联合航空、美国航空、福特汽车、景顺和大都会人寿。

跌至 200 日均线附近,反弹信号出现?

目前 VOOV 的股价已经异常的低,仅比其 200 日移动平均线 166 美元高出不多,而这通常被市场视为一个积极的信号。

根据 FactSet 的数据,除非遭遇像疫情或 2022 年初美联储开始的一系列快速加息这样的重大不利事件,在过去 20 年或更长的时间里,投资者通常会在股价触及 200 日移动平均线时买入。

这一模式表明,如果市场没有出现意外的严重负面冲击,VOOV 有望在当前水平附近找到支撑。

此外,VOOV 目前以大约 15.8 倍的市盈率交易,比标普 500 指数的 21.1 倍低约 26%。在过去 10 年中,根据媒体使用 FactSet 数据的计算,该价值股基金相对于更广泛指数的折扣平均约为 17%。

联储降息在即,价值股反弹有望?

值得注意的是,价值股往往属于成熟企业,其利润更多受到消费者和企业需求变化的影响,而不是受行业特定因素的驱动,比如银行业。因此,价值股的表现通常与经济周期紧密相连,在经济增长放缓和利率高企的情况下,这些股票可能会承受更大的下行压力。

然而,当前经济正在面临增长放缓的窘境。市场普遍预期,随着通胀压力减轻,美联储可能会降息,以刺激经济增长。然而,这种预期并非板上钉钉,降息的具体时间和幅度仍然充满变数。

这种不确定性带来了持续的担忧:如果经济增长持续放缓,而利率依然保持在较高水平,这将对价值股构成双重打击。

经济预期的变动,如通过债市所体现的,可能会引发价值股的剧烈波动。

根据圣路易斯联储的数据,目前两年期美债收益率比 10 年期=高出大约 0.3 个百分点,为今年以来最大的倒挂幅度。这种异常现象反映出投资者对于美联储可能长期维持高短期利率以对抗通胀的担忧,这可能会抑制消费者和企业对商品和服务的需求。

与此同时,长债收益率低于短债,这表明市场担心美联储的现行政策可能会导致经济持续疲软,进而降低长期的通胀预期。

分析认为,一旦美联储发出首次降息信号,两年期美债收益率应会下降,市场将对长期经济增长更有信心,这将推高 10 年期美债收益率。收益率曲线倒挂的情况随之改善,这通常对经济有利。

鲍威尔稍早前表示,美联储在通胀方面取得了相当大的进展,但希望看到更多进展,然后才有足够的信心开始降息。鲍威尔拒绝就美联储的首次降息时间给出任何具体信息。目前市场更倾向于 9 月进行年内的首次降息。

22V Research 分析师 Dennis DeBusschere 在报告中写道:

收益率曲线应该会有所陡峭化,以支持价值股反弹。