Microsoft: AI only sees "spending money" and not "returning money"

$Microsoft(MSFT.US) On July 30, the U.S. stock market announced its financial report for the first quarter of the 2025 fiscal year ending September 30. Due to the company's change in financial disclosure standards from the 2025 fiscal year, some performance indicators are not comparable to past data, which investors need to be aware of. Overall, Microsoft's performance this time, while meeting expectations with all indicators slightly exceeding or aligning with market expectations, lacks significant growth highlights and profit pressure has begun to show. The key points are as follows:

1. AI support, Azure growth instead declines: The year-on-year and constant currency growth rates for Azure this quarter are 33% and 34%, respectively, both down 1 percentage point from the previous quarter. Although this aligns with the company's prior guidance and market expectations, it does not indicate strong cloud demand growth like Google's GCS. As previously noted by Dolphin Investment Research, GCS, as a "younger brother" and share gainer, may not reflect the overall industry growth.

In detail, the revenue growth contribution from AI this quarter reached 12 percentage points, slightly up 1 percentage point from the previous quarter, but the growth of traditional demand slowed by 2 percentage points. What further dampens market sentiment is that Microsoft's guidance for Azure's growth next quarter is expected to slow by another 1-2 percentage points. This indicates that AI seems not only unable to significantly boost Azure's growth but is also continuously slowing down.

Dolphin Investment Research speculates that possible reasons include: ① A large amount of AI-related demand has yet to be recognized as revenue and remains in pending contract amounts; the GPU supply bottleneck still limits Azure's growth; ② After the most severe phase of GPU supply not meeting demand has passed, the significant decline in computing power rental prices has dragged down revenue growth; ③ Azure's leading advantage in AI has been diminished by AWS and GCS, possibly losing market share.

2. Office business growth is mediocre, Copilot 2.0 did not bring rapid penetration: The Office 365 business, closely tied to AI, saw revenue growth of 15% this quarter (16% growth in constant currency), which is flat compared to the previous quarter. Guidance for the next quarter also indicates a 2 percentage point decline in growth. Similarly, this quarter's growth lacks highlights, and the outlook for the future is further declining. Although Office Copilot recently launched a new 2.0 feature update, it still has not led to a rapid increase in user adoption. The commercialization capability of AI in consumer productivity tools still seems unproven.

3. Advertising business continues to grow rapidly, is search still the best route for AI? The personal computing segment saw revenue growth of 16.8% year-on-year this quarter, accelerating by 2.3 percentage points from the previous quarter, making it the most noticeable revenue acceleration among the three major segments. This also exceeds market expectations by nearly 5%, being the largest beat among the three major segments The advertising business has significantly accelerated after the integration of Copilot Pro. Excluding customer acquisition costs, the growth rate of the advertising business this quarter increased by 3 percentage points quarter-on-quarter, reaching 18%. Both in terms of absolute growth and marginal trends, the performance is quite impressive. It appears that AI features are still primarily utilized and generate revenue in search-related areas.

4. Are leading indicators a source of hope? The current revenue performance is clearly not outstanding, and the outlook can be described as poor, but the leading indicators reflecting the subsequent revenue growth trend are relatively optimistic. The growth rate of newly signed enterprise cloud contracts has surged to 30%, with a more realistic growth rate under constant exchange rates at 23%, also accelerating by 4 percentage points quarter-on-quarter. This indicates that there may be incremental demand still in the contract stage, which has not yet reflected in revenue.

Similarly, the balance of existing contracts awaiting fulfillment (i.e., deferred revenue from payments received but not recognized as income + amounts for contracts signed but not yet paid) has seen a year-on-year growth rate increase of 2 percentage points to 22%, also indicating that there may be more demand that has not yet reached the revenue recognition stage.

5. Is the cycle of slowing revenue, increased investment, and accelerated profit coming to an end? If the revenue perspective is merely lacking highlights, it still needs to be verified whether and when the incremental demand for AI can arrive. The pressure on profits from the need for advanced Capex expenditures has already begun to show.

The largest marketing impact is reflected in the gross profit perspective, with this quarter's gross margin at 69.4%, down 1.8 percentage points year-on-year and down 0.2 percentage points quarter-on-quarter. This led to a gross profit increase of only 13% year-on-year, lagging behind revenue growth. Notably, the amortization and depreciation this quarter have doubled compared to the same period last year, increasing by over $3 billion.

Therefore, although the expense ratio has passively contracted by a total of 0.8 percentage points, Microsoft's operating profit margin still decreased by 1 percentage point year-on-year to 46.6%. This quarter, operating profit grew only 13.6% year-on-year, marking the first time since Q3 of FY23 that profit growth has lagged behind revenue, signaling the end of the company's profit margin expansion cycle and a shift towards profit margin contraction.

In this quarter, Microsoft's Capex expenditure has once again risen to $20 billion, a year-on-year increase of 79%. This means that only 70% of operating profit for a single quarter has been reinvested into fixed assets. With such a massive investment, subsequent profit margins are likely to remain under pressure.

6. Is the guidance for the next quarter overly conservative or genuinely poor? Regarding the guidance for Q2 of FY25, the continued slowdown in the growth rates of core Azure and Microsoft 365 businesses has been mentioned earlier. As for profits, the midpoint of the guidance for next quarter's operating profit margin is 44%, which, while continuing to decline quarter-on-quarter, is slightly up by 0.4 percentage points year-on-year. This seems to indicate that the pressure on profit decline may ease somewhat.

Dolphin Investment Research Perspective:

As mentioned earlier, overall, Microsoft's key indicators this quarter are either in line with or slightly exceed expectations, with no significant shortcomings. However, the issue is that based on the company's guidance, subsequent revenue and profit growth are expected to be around 10% to 20%. Currently, the company's LTM PE exceeding 30x clearly reflects that it is not merely about "meeting expectations."

As we mentioned last quarter, the reason the market is willing to give Microsoft a valuation premium comes from investors' imagination of substantial incremental revenue from AI in the future, and Microsoft's relatively highest visibility in the mid to downstream of the AI sector. However, the key Azure and Microsoft 365 businesses have still not demonstrated significant incremental revenue brought by AI, and subsequent guidance indicates that growth is expected to decline further.

However, in the current situation where we have not seen significant incremental revenue from AI, and it is still uncertain whether it can ultimately be realized, the quarterly capital expenditures of up to hundreds of billions are indeed necessary upfront expenses. Moreover, the past two quarters have primarily reflected a significant suppression of profit margins from the perspective of gross margin.

Therefore, if the high investment versus incremental revenue ROI does not show significant improvement in the next few quarters, Dolphin Investment Research must remind investors of the potential risks associated with the current valuation of over 30x.

The following is a detailed commentary on the financial report:

1. Changes in Financial Report Disclosure

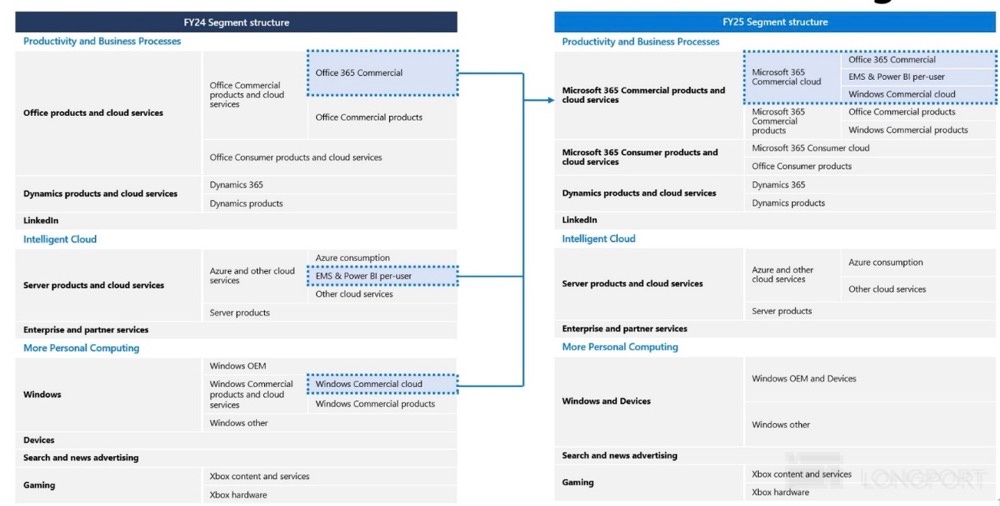

After the last quarter's financial report, Microsoft officially announced that it will make significant adjustments to the departmental structure of financial report disclosures starting in fiscal year 2025. The adjustment approach is to move all enterprise-facing Microsoft 365 service projects (in addition to the B2B Office 365, also including Windows 365 and Security 365) into the major revenue category of productivity and processes (PBP) for Office 365, thus unifying the Office 365 revenue into Microsoft 365 revenue.

Specifically, the new productivity and processes 365 revenue has added:

① The Microsoft EMS (Enterprise Mobility and Security, similar to enterprise network security protection) originally in the Intelligent Cloud (IC) business, plus Power BI, which is essentially a SaaS-type service. Note that these revenues are charged per user or seat, similar to Office 365 revenues.

② The enterprise-facing Windows cloud operating system (Windows commercial cloud). This business is sold as part of the Microsoft 365 service.

After this adjustment, moving SaaS-type services that should not have been in the cloud business—security and Power BI—has made Microsoft's PaaS business, namely Azure, clearer and more straightforward for industry comparisons.

All enterprise-facing SaaS-type businesses have been categorized into productivity and process services (PBP), making the contract liabilities (or annual pre-revenue business) clearer. These changes are better for understanding Microsoft's true SaaS and PaaS business revenues

In addition to the major changes in streamlining business types, there are also some minor adjustments, such as:

a. In the Productivity and Business Processes (PBP), besides the enterprise-oriented Microsoft 365 (note that Microsoft has a naming convention where all SaaS-type cloud products are called 365), there is also a small portion of traditional software products sold to enterprises (for example, some traditional Office suites and their locally deployed products).

b. In addition to the enterprise customers in Productivity and Business Processes, consumer-oriented products have also been separated out, mainly the Office suite and some cloud services sold to users (like One Drive).

This adjustment clarifies the classification of to B and to C in PBP.

The other main change is some minor adjustments in More Personal Computing (MPC):

a. After the revenue from the Windows cloud operating system was moved out, Windows and Devices were combined for reporting. It seems that the granularity has decreased, but it can be understood that whether selling Windows to OEM manufacturers like Lenovo or Microsoft directly selling Surface, they are essentially selling PCs, so combining them is not a big issue.

b. Another point of market interest is that the newly launched Copilot product's revenue has been moved from Office to More Personal Computing (MPC).

This adjustment seems interesting to Dolphin, as it essentially indicates that the official stamp has deemed Copilot as an unfeasible separately charged incremental service module within Office (SaaS-type business is generally unreliable), and has moved it to the consumer-oriented search business, treating it as a new form of search Q&A, attempting to increase the possibility of a turnaround in future search business (or in other words, future search business will include both advertising and Copilot's paid services).

For those interested, you can refer to the summary of the segmented adjustments:

Due to the aforementioned splitting of some businesses from the IC and MPC segments into PBP, we can see that the new PBP segment's revenue guidance is approximately $7 to $8 billion higher than before. Meanwhile, the IC segment's revenue has decreased by about $4 to $5 billion, and the MPC segment's revenue has decreased by about $2 to $3 billion compared to the original figures.

II. Is the "AI" moment just thunder without rain?

2.1 With AI support, is Azure's growth rate declining?

The growth rate of Azure's business, closely related to the spending on training and inference of large AI models, is arguably the most critical indicator reflecting the dynamics of AI development and demand, and has always been one of the market's main concerns.

Under the new standards, Azure's year-on-year and constant currency growth rates for this quarter are 33% and 34% respectively, both down 1 percentage point from the previous quarter. Although this aligns with the company's prior guidance and market expectations, it does not reflect the unexpectedly strong growth seen in Google's GCS. In detail, the revenue growth contribution from AI this quarter reached 12 percentage points, a slight increase of 1 percentage point from the previous quarter, but the growth of traditional demand slowed by 2 percentage points.

What further dampens market sentiment is Microsoft's guidance for Azure's growth rate next quarter, which is expected to slow by another 1-2 percentage points. Taken together, this seems to indicate that AI demand has not significantly boosted Azure's growth rate, but rather is continuing to slow. Dolphin Investment Research speculates that possible reasons include: ① A large amount of AI-related demand has yet to be recognized as revenue and remains in pending contract amounts; or the GPU supply bottleneck continues to limit Azure's growth; ② After the most severe phase of GPU supply shortages has passed, related computing power rental prices have significantly decreased, dragging down revenue growth; ③ Azure's leading advantage in AI has been diminished by AWS and GCS, possibly resulting in lost market share.

Overall, due to the lackluster performance of the core Azure segment, the overall revenue of the Intelligent Cloud segment under the new standards is $24.1 billion, which is nearly in line with market expectations, and does not constitute a beat. However, from the overall growth acceleration of the segment, it can be inferred that the growth of enterprise services should see a significant increase this quarter.

2.2 Slow growth of 365, no significant progress in Copilot promotion

The Microsoft 365 commercial business, which has the second highest closeness to AI and, after adjustments, also ranks among the top two in revenue size within the company, saw a revenue growth of 15% this quarter (16% growth at constant currency) which is flat compared to the previous quarter. For the next quarter, the guidance indicates a growth rate decline of 2 percentage points. Similar to Azure, this quarter's growth did not accelerate, and the outlook for the future is further declining.

It is reported that Office Copilot recently launched a new 2.0 feature update, but so far, it has not demonstrated a significant increase in demand driven by AI

From the perspective of volume and price:

1) The number of enterprise Microsoft 365 subscription customers increased by 8% year-on-year, slightly up from the previous quarter.

2)Correspondingly, the year-on-year growth rate of average revenue per user decreased slightly from 7.5% last quarter to 6.5% this quarter. It can be seen that the increase in average revenue per user driven by the adoption of higher-priced products like E5 continues, but the space and speed for price increases are narrowing.

In other major businesses within the productivity segment, the growth rates of personal 365 business, LinkedIn, and Dynamics 365 are generally flat compared to the previous quarter, or slightly declining. From an absolute growth perspective, the nearly 20% growth in Dynamics business is clearly the second-largest incremental revenue source after Azure.

Overall, as there are no significant changes in the growth rates of major businesses, the adjusted revenue for the productivity process segment this quarter is $28.3 billion, which is also basically in line with market expectations. It represents a year-on-year growth of 12%, slightly up by 0.3 percentage points from the previous quarter, with no particular highlights.

III. Advertising continues to grow strongly, is search still the main avenue for AI?

The adjusted revenue for the personal computing segment this quarter increased by 16.8% year-on-year, accelerating by 2.3 percentage points from the previous quarter, making it the most noticeable revenue acceleration among the three major segments. The actual revenue exceeded market expectations by nearly 5%, also the most significant beat among the three segments.

Specifically, this is mainly due to the significant acceleration in advertising revenue contributed by the integration of the Copilot pro business. After excluding customer acquisition costs, the growth rate of advertising revenue this quarter increased by 3 percentage points quarter-on-quarter, reaching 18%. Both in terms of absolute growth and marginal trends, this is quite impressive. It can be seen that currently, AI functions are still primarily successfully applied and monetized in search-like areas.

In other sub-segments: ① Windows OEM and device revenue increased by 2% year-on-year, still in a state of stagnation.

② After the acquisition of Blizzard, game business revenue increased by 61% year-on-year, but after excluding the impact of consolidation, the actual growth rate is 4%, also hovering at a low level

IV. Are the improvements in revenue leading indicators a glimmer of hope?

The company's overall revenue this quarter is $65.6 billion, slightly above market expectations, with a year-on-year growth rate of 16%, which is a slight acceleration of 0.8 percentage points compared to the previous quarter. As mentioned above, this is mainly attributed to the acceleration of MPC and its advertising business.

Excluding the impact of the consolidation of Activision Blizzard, Microsoft's actual comparable revenue growth rate is approximately 13%, which also shows an acceleration compared to the previous quarter. However, overall it still has not broken through the 12%-14% range seen over the past five quarters, and there are no signs of substantial acceleration in growth.

In summary, apart from the notable driving effect of AI in the search business, the core Azure and Microsoft 365 businesses have not shown signs of benefiting from the acceleration of AI growth, and the subsequent guidance even indicates a further slowdown.

Although the current revenue performance is not impressive and the outlook is poor, the leading indicators reflecting the trend of future revenue growth are relatively optimistic. The growth rate of newly signed enterprise contracts has significantly increased to 30%. Although the more realistic growth rate at constant exchange rates is 23%, it has also accelerated by 4 percentage points quarter-on-quarter. This indicates that there may still be incremental demand that is in the contract stage and has not yet reflected in revenue.

Similarly, the balance of existing contracts to be fulfilled (i.e., deferred revenue from payments received but not yet recognized + amounts for contracts signed but not yet paid) this quarter is 259 billion, with a year-on-year growth rate accelerating by 2 percentage points to 22%, which also indicates that there may be more demand that has not yet reached the revenue recognition stage.**

V. The "cost" of declining profit margins due to AI explosion needs to be paid in advance

If the revenue perspective is merely lacking highlights, it still needs to be verified whether and when the incremental demand from AI can arrive. From the profit perspective, the upfront investments that need to be made are already showing pressure on profits.

1)From the gross profit perspective, Microsoft's gross margin this quarter is 69.4%, a year-on-year decrease of 1.8 percentage points and a quarter-on-quarter decline of 0.2 percentage points. This results in gross profit increasing by only 13% year-on-year, lagging behind the revenue growth rate.

2)From the expense perspective, Microsoft's marketing, research and development, and management expenses this quarter have increased by about 10% to 14% year-on-year, which is lower than the growth rate of revenue or gross profit. Therefore, the combined expense ratio has passively contracted by 0.8 percentage points, indicating that the company's internal cost control and efficiency improvements have helped offset some of the profit margin decline caused by high capital expenditures.

3)However, overall, due to the significant decline in gross margin caused by high capital expenditures, Microsoft's operating profit margin has still decreased by 1 percentage point year-on-year to 46.6% this quarter. This has resulted in the company's operating profit growing only 13.6% year-on-year, marking the first time since Q3 of FY23 that profit growth has lagged behind revenue growth, signaling the end of the company's profit margin expansion cycle. With high investments related to AI, it has slipped back into a profit margin contraction cycle.

4)The decline in profit margins is evident from this quarter's capital expenditures, which have risen again to $20 billion, a year-on-year increase of 79%. This means that nearly 70% of the operating profit for one quarter has been reinvested into fixed assets. Additionally, the amortization and depreciation this quarter have doubled compared to the same period last year, increasing by over $3 billion. Free cash flow has also seen a year-on-year negative growth of 7% due to the drag from high capital expenditures. The massive investment in AI infrastructure has begun to fully reveal its pressure on profits.

Dolphin Investment Research on Microsoft's Past Studies:

Financial Report Commentary

July 31, 2024, Conference Call Summary: Microsoft: No Miracle from Strong Efforts, Is the AI Dream Stalled?

July 31, 2024, Conference Call Summary: Microsoft: How to Grasp the Rhythm of AI Investment

April 26, 2024 Financial Report Review: Microsoft: Azure Carries Everything, Definitely the "Anchor" of US Stocks

April 26, 2024 Conference Call Minutes: Microsoft: How Much to Invest in AI?

October 25, 2023 Conference Call: Microsoft: AI Features Progress Steadily, Driving Demand Recovery

October 25, 2023 Financial Report Review: “AI” Microsoft is Here, Is the Internet Entering the Microsoft Era Again?

July 26, 2023 Conference Call: Microsoft: All in AI

July 26, 2023 Financial Report Review: The Vision of AI is Beautiful, but Microsoft's Reality is Still Lean

April 26, 2023 Conference Call: What Will be the Impact of AI on Microsoft's Performance?

April 26, 2023 Financial Report Review: “Giant” Microsoft Comes Out of the Low Point, Can It Soar Again with ChatGPT?

January 25, 2023 Conference Call: Slowdown is Inevitable (Microsoft Conference Call Minutes)

January 25, 2023 Financial Report Review: Strong Azure Can't Save Microsoft in the Cycle

In-Depth Research

July 5, 2023: Can AI "Recreate" Microsoft? Not So Easy

May 30, 2022 "Microsoft is flawless, killing the price is more perfect"

February 15, 2022 "Microsoft: Don't focus on poor expectations, having orders and reserves is the key"

November 22, 2021 "Alibaba, Tencent are declining before they get old, why is Microsoft getting stronger?"

Risk disclosure and statement of this article: Dolphin Investment Research Disclaimer and General Disclosure

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.