Quit the "one-size-fits-all" approach, Alibaba "turns the tide"

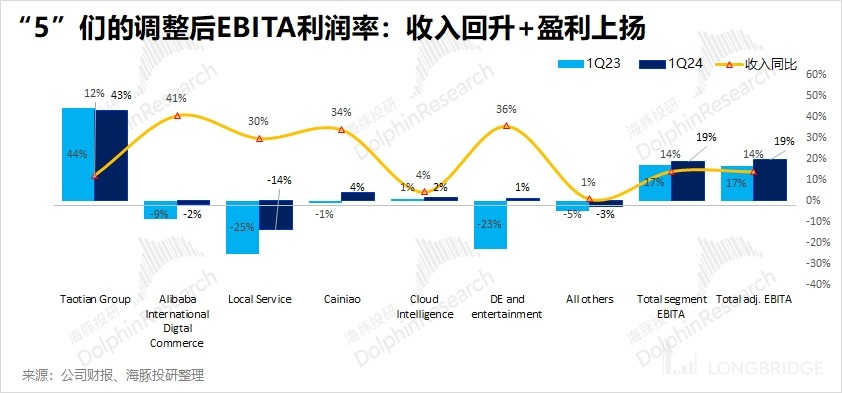

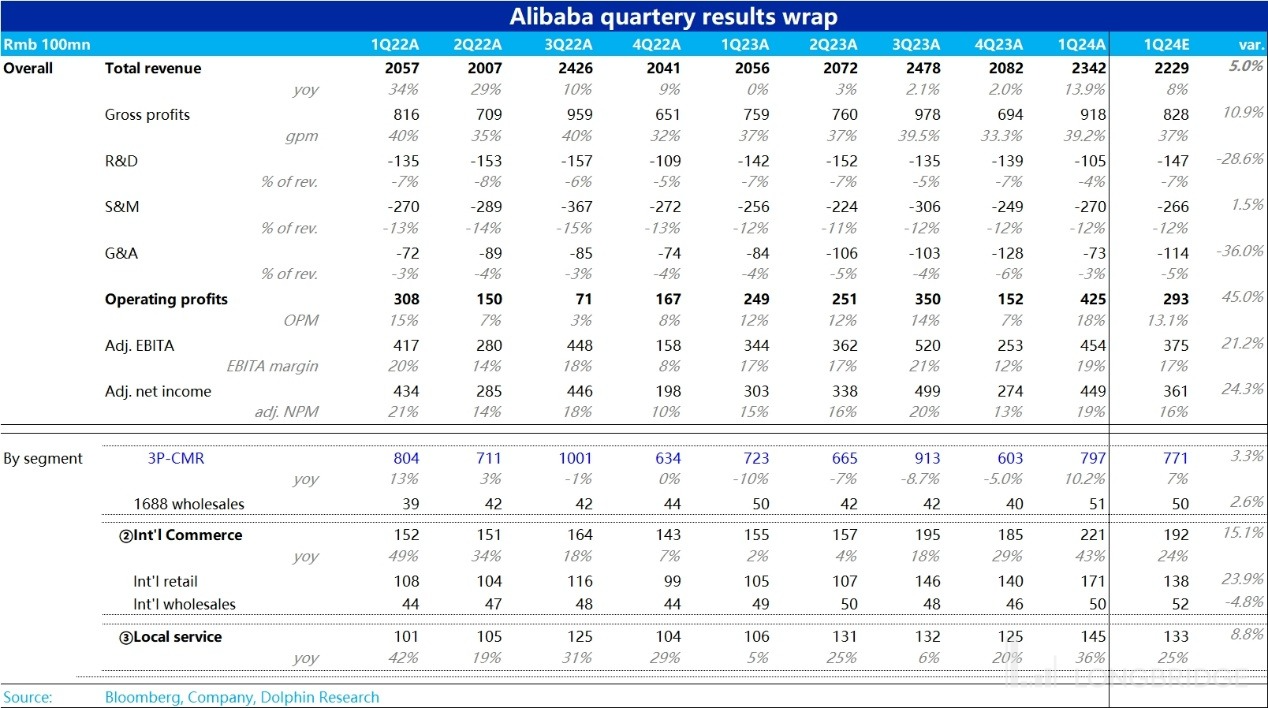

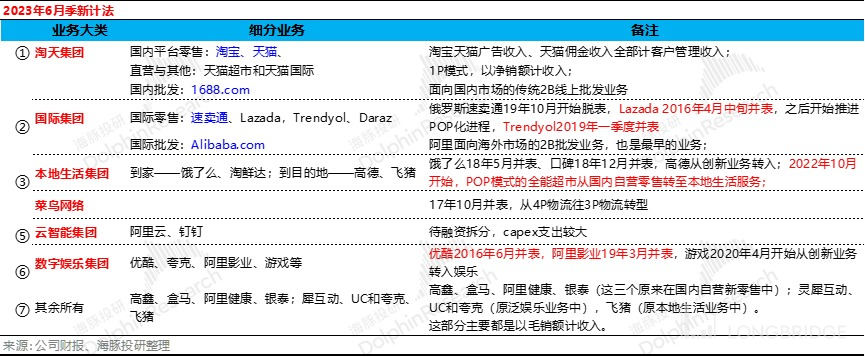

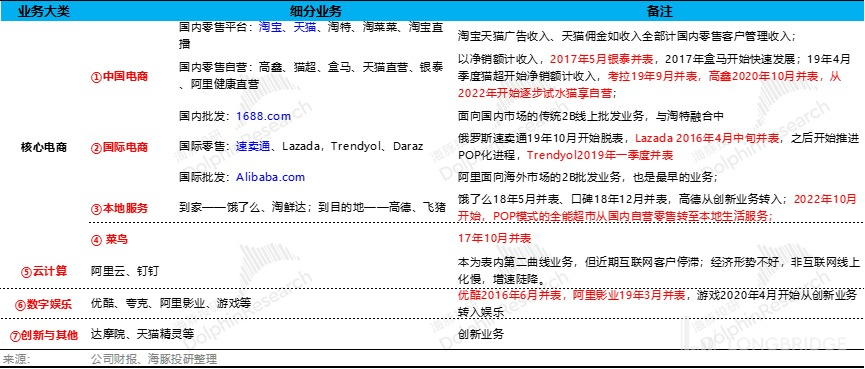

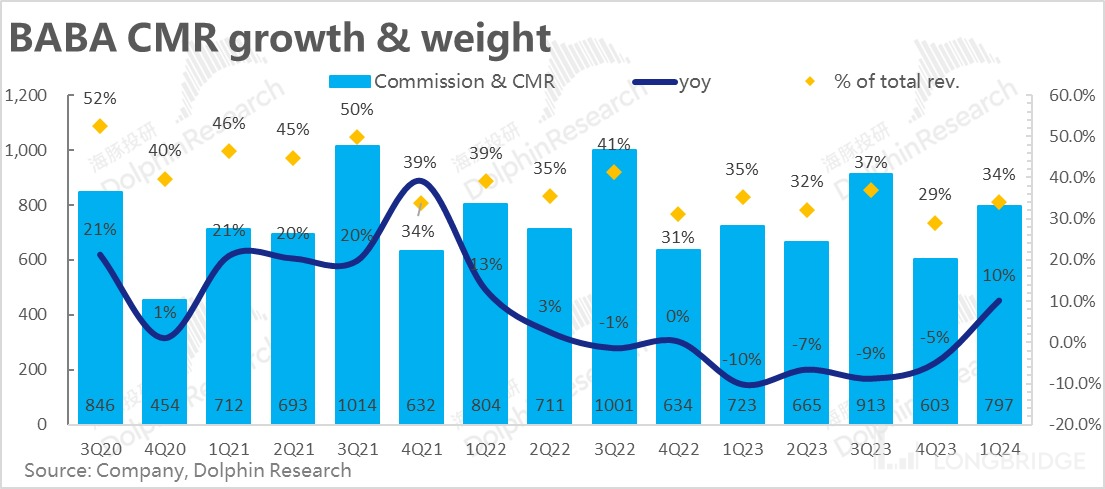

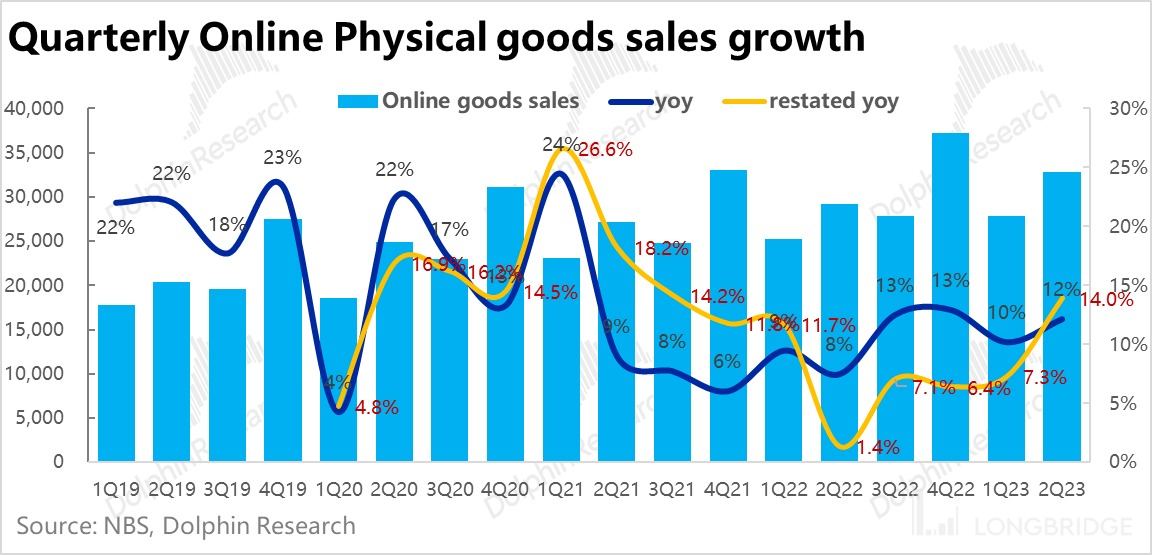

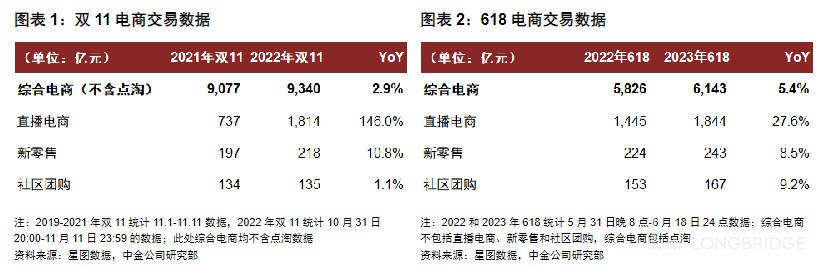

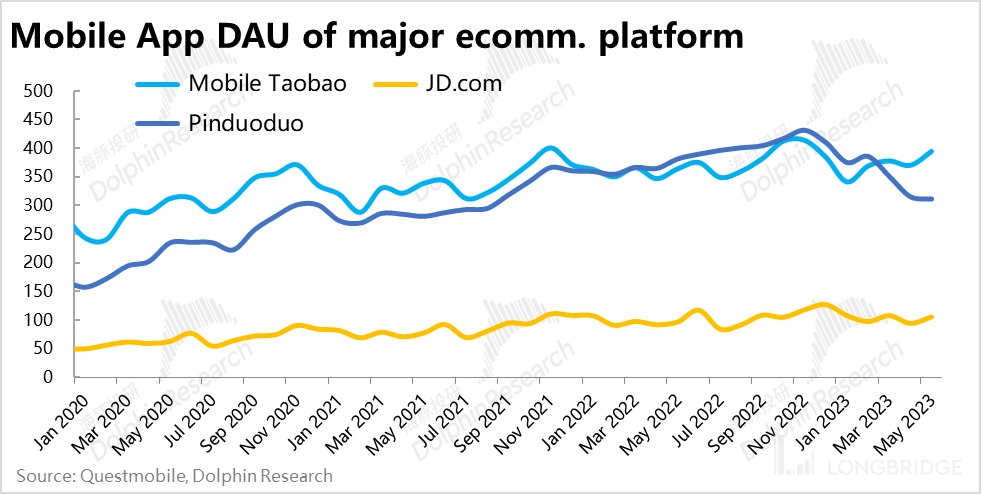

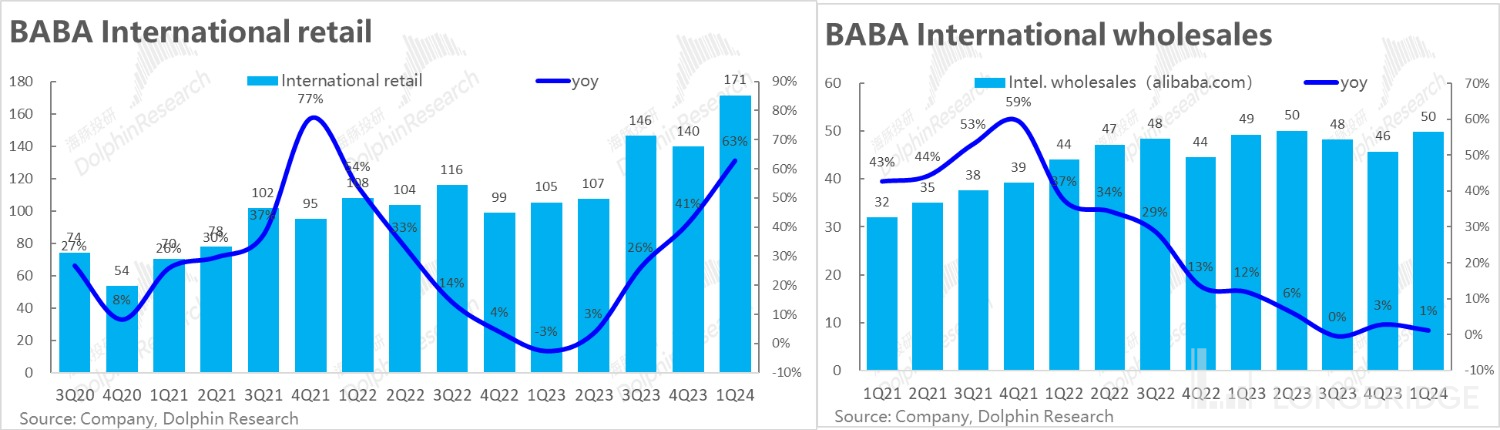

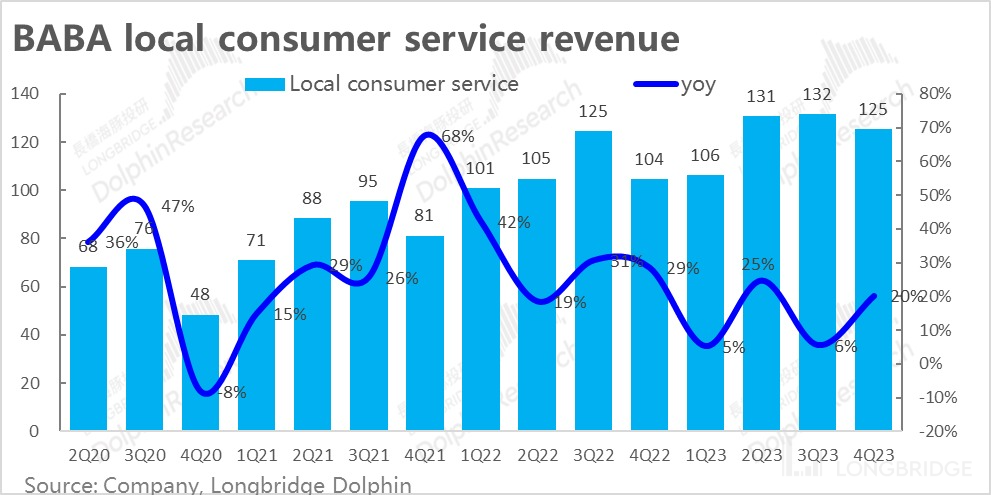

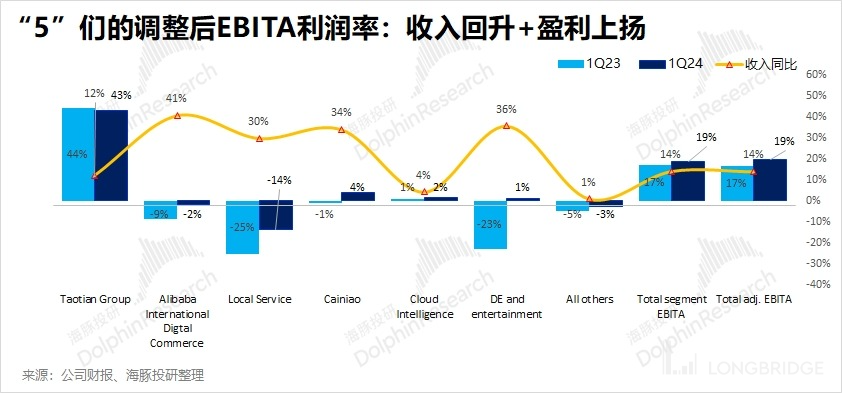

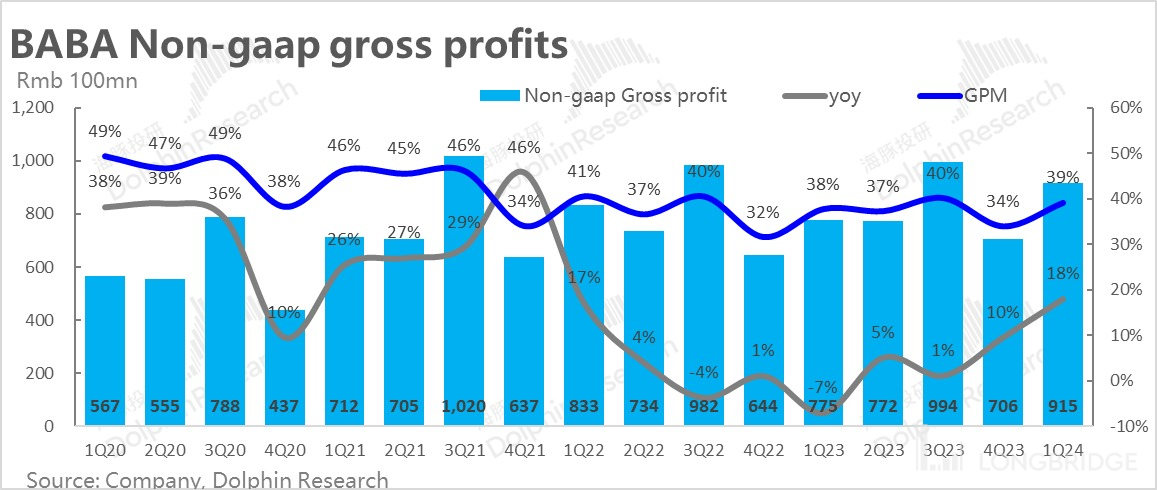

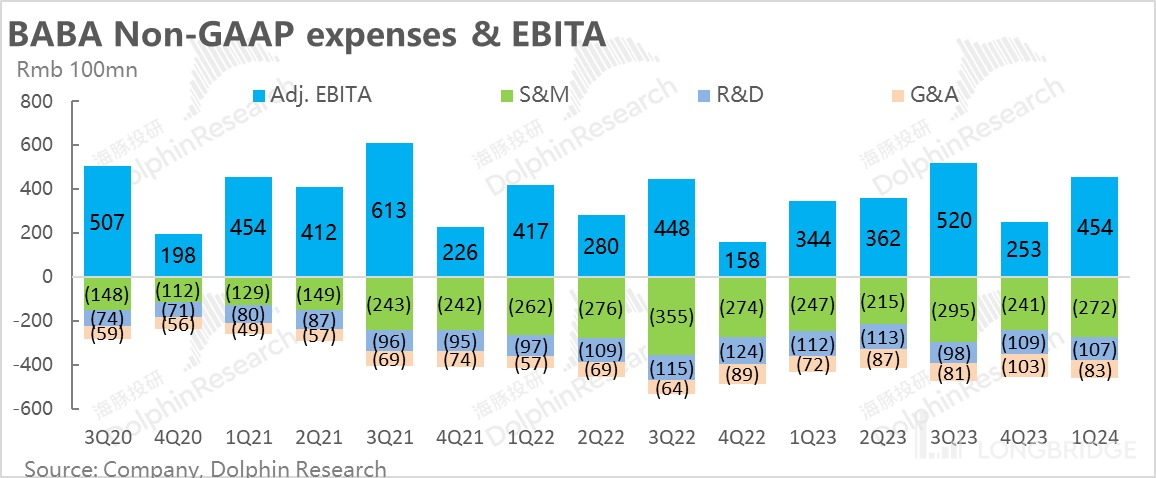

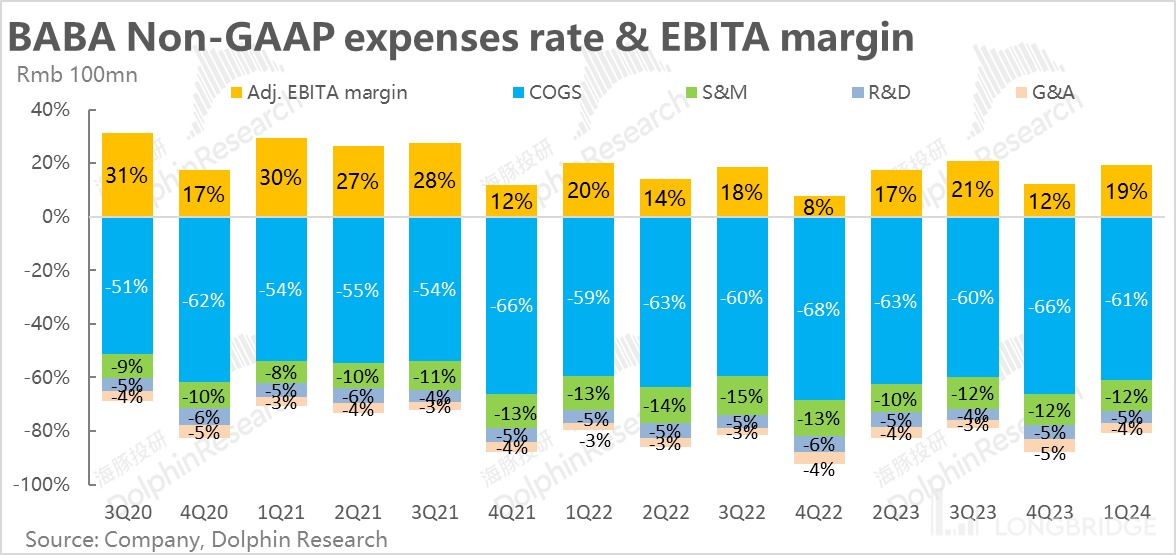

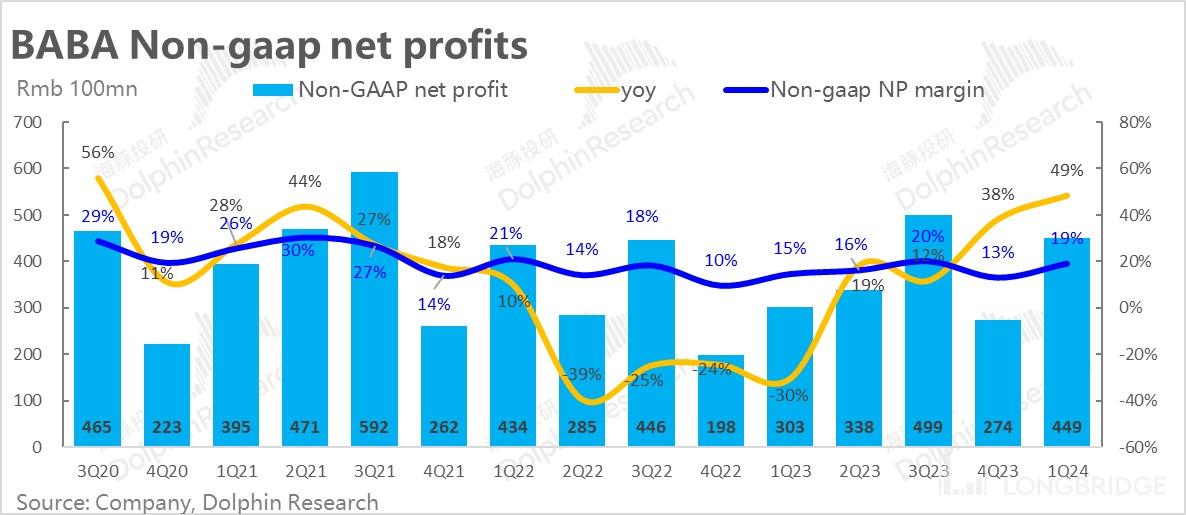

Since Jack Ma set Ali to "return to Taobao, return to users, return to the Internet", does Ali have a chance to "turn around"? From this quarter, Ali, who has been suffering for the past two years, seems to have finally come to a light. Ali this time again big financial report caliber, resulting in the trend is not so clear, but the key trend is still relatively obvious: Tao Tian looks good, actually mainly the base and expectations are low, and other businesses after independent accounting, because itself is not Tao Tian as serious competition pattern, but income elasticity performance is relatively large. According to the six major groups to give you a stroke of the key points: * * 1) Tao Tian is not bad? The market is too pessimistic * * 1) Tao Tian: as a soul support, Tao Tian customer management revenue year-on-year market was originally expected to be 4-5%, then adjusted to 7-8%, the actual 10%, reached 79.7 billion; The corresponding adjusted profit increased by 9%, slightly lower than the income, all properly exceeded expectations. However, judging from the expected difference, there is still fierce competition behind this group of numbers: CMR growth is 10%, and GMV growth is estimated to be around 5% (due to more returns, GMV and no income in the same period last year). And if there is no increased competition, the return of CMR growth rate should correspond to a higher profit growth rate, while the profit growth rate is actually only 9%, which is also confirmed by the higher overall sales expense growth rate (10% year-on-year) after the removal of equity incentives. But in any case, * * this number basically shows the inflection point, implying that Tao Tian stayed out of the bottom * *, after all, the most critical daily growth rate turned positive, behind CMR growth may not be able to achieve 10%, but based on the 618 unit price and order volume at the same time turned positive, to achieve positive growth should be no problem. * * 2. don't eat big pot rice, energy came up! * * If Tao Tian, the big "1" pillar, has only improved at the bottom, but has not yet reversed, then the remaining "5" seem to have energy after not eating from the same big pot: * * 1) The brightest: Jiang Fan's international business. * * Retail sales exploded 60% year-on-year, and the overall order growth rate was 25% year-on-year. AliExpress Choice, a full-custody model pushed by Jiang Fan after his arrival, helped a lot. The improvement in operation efficiency and the increase in liquidity rate were also a major reason. In addition, many international businesses were denominated in local currencies, and the devaluation of RMB also boosted the business growth rate. The most important thing is that while the revenue is growing, the international business is still reducing losses: the equity incentive factor and the operating profit including amortization (Adjusted EBITA) lost only 0.42 billion, with a loss rate of only 2%, compared with 9% in the same period last year. **2) The most underachiever: Pan-entertainment. The next biggest marginal change is pan-entertainment. Not only did Ali Pictures and barley net repair obviously, but Youku also "returned to its soul". Therefore, in addition to the year-on-year increase in revenue, the profit margin actually turned to 1%, which is unprecedented! **3) Pretty good: rookie and local life. * * Due to the rapid progress of pan-entertainment, the two actually performed well and only ranked third. A. Cainiao is mainly dependent on international business, followed by Tao Tianzhong's proprietary business, with a direct growth rate of 21%; International business orders grew by 25%, and Cainiao achieved 34%, which only shows that Cainiao has done a good job in expanding external customers. B. The year-on-year growth rate of local life has achieved 30%. Of course, this is partly due to the low base last year, but the year-on-year revenue and profit margin repair performance is not bad. * * 4) The bottom is hovering like light: * * Aliyun, compared with the negative growth of 3% in the previous quarter, the positive growth of 4% in this quarter is not bad, slightly better than the market expectation, but obviously it is still not back on track. At present, Aliyun has introduced strategic "shareholders" to open up the upward space of long-term business, which may be more important than the current business development. **5) All the rest: each has its own merits and is generally average. **Other businesses, whether it's Gaoxin, Box Horse, or Ali Health or Yintai, are mostly offline self-employed, with an unusually high increase in the epidemic last year and a significant decline in the second quarter of this year. Moreover, the above five groups, in addition to revenue performance, the most important thing is to reduce costs and increase efficiency, the story of profit repair continues, especially the pan-entertainment big stride profit repair. The vast majority of Ali's small animals, who can't eat a big pot of rice, currently show higher income and profit elasticity than the soul pillar-the Tao Tian business.! ! * * Dolphin Jun's overall view: * * As the first performance report of the 1+6 + N strategy landing to the financial caliber, I finally regained some confidence for myself. And Ali from the current valuation, even 100 yuan/share of Ali is only the valuation of Tao Tian Group + Group net cash. However, under the undervaluation, Ali can do a lot more. 1) Aliyun will distribute shares to Ali shareholders before listing. As a basically fully controlled asset, Aliyun's valuation is basically set at US $600-80 billion. 2) Ant's valuation Dolphin Jun is basically estimated at US $90 billion, and the corresponding shareholding of Ali should be US $more than 30 billion. When the IPO moves forward, these two businesses correspond to Ali's upward elasticity of about 35%. Especially when these businesses are re-listed one by one, and then superimposed Aliyun out of the table, Amoy is likely to operate to improve the repurchase to give back to shareholders, Ali is currently a clear upward opportunity is greater, while the downward risk is less opportunity period. Of course, after the value of asset spin-off and repurchase re-issued at this stage, Ali's long-term real out of a long-term upward assets, or to see in the core hinterland Tao Tian Group can reverse the war, no longer lose, and the Dolphin Jun is still conservative, can only say while walking. After all, Ali has gone too long and too far on the wrong road. Although he is fortunate to turn back, it takes determination, time, and even more effort to turn back. * * The following is a detailed analysis: * * * * 1. Ali has adjusted the financial report again! * * After dismantling 1+6 + N last quarter, Ali began to adjust the financial report caliber again from this quarter, and this adjustment was especially large. The overall thinking was aligned with the split idea of 1+6 + N: 1) Tao Tian Group: Taobao, Tmall, Tmall Supermarket + Import Direct Marketing; Domestic wholesale; 2) International Group: it basically corresponds to the previous international retail businesses such as AliExpress, Lazada and Ali International Station 3) Local Life Group: Hungry Noodles and Gaud 4) Cainiao Group: The same as before, except that the current income calculation method regards other businesses in Ali Group as customers, and the income generated is included in Cainiao Company's income; 5) Intelligent Cloud Group: Aliyun + DingTalk; the current income calculation method includes Aliyun's other businesses in Ali Group. 6) Pan-Entertainment Group: Youku and Ali Pictures; 7) All the rest: Gao Xin, Hema, Ali Health and Yintai (these three were originally in the domestic self-operated new retail); Lingxi Interactive, UC and Quark (in the original pan-entertainment business), Fliggy (in the original life business). This part is mainly based on gross sales.! Dolphin King will put another previous calculation method to facilitate comparison before and after:! * * 2. Taobao Tmall (at least) saw the dawn before dawn * * First of all, the core * * domestic retail customer management revenue (CMR) was 79.7 billion yuan, a year-on-year growth rate of slightly more than 10%, after the previous four consecutive quarters of year-on-year decline, finally turned positive. Although the market has fully expected this CMR growth rate to turn positive year-on-year due to the impact of the epidemic in the second quarter of last year due to a very low base, the actual performance is still slightly above expectations compared to the market's generally expected growth rate of 7%-8%. * *! However, with reference to the second quarter, the overall growth rate of domestic physical retail sales reached 14%. According to third-party data, the year-on-year growth rate of shelf e-commerce during the 618 period was only slightly more than 5%, still significantly lower than the growth rate of live e-commerce by about 28%. It can be inferred that the growth rate of Ali GMV during the quarter is still only single digits, in other words, **Taobao Tmall is still underperforming the market, share continues to lose. * *! ! and the positive from a very low base this quarter is not sustainable, so the market is also widely expected that subsequent CMR growth is likely to decline again. So in a nutshell, **Taobao Tmall's performance on the growth side of the season was mainly slightly better than expected from a low base, and the probability that the inflection point of the actual competitive landscape and growth pivot of Taobao has not yet officially arrived. * * However, judging from the front-end traffic and the number of users, according to Quest Mobile Taobao App, the number of daily users has continued to grow since the beginning of 2023. Under the company's standard, the number of daily users of Tao Tian Group increased by 6.5 year on year in this quarter. It can be seen that with the strategic direction of user traffic first and the implementation of many measures such as "low price every day", "10 billion subsidy", "Taobao at night" and "shopping for short videos", * * Ali's user traffic and stickiness are indeed returning, clearly starting the first step to fight back against the erosion of Duoduo and chattering traffic. * * It is worth paying attention to the competition for user traffic among subsequent platforms.! * * 3. self-operated retail: all "burdensome" assets are stripped off, leaving only high-quality platform assets * * * after the adjustment of the company's structure and financial report, * * all offline retail businesses with heavy assets, such as box horse, yintai department store and gaoxin retail, which were originally acquired or cultivated under Ali's "new retail" strategy, have been kicked out of the self-operated retail sector under taotian group, only Tmall Supermarket, Tmall International and other online proprietary businesses are retained. **Due to a significant change in caliber, we are unable to go back and compare historical data for the time being. Looking at this season's data alone, **as the growth driver is mainly from consumer electronics, Dolphin Jun estimates that more standard electrified products may have been added to the proprietary category, which may also have some negative impact on Jingdong. * * International retail" explosive "growth after 4. Jiang Fan took over and operated independently **In addition to CMR's long-lost and slightly better-than-expected positive growth, the amazing growth in international retail business was another major highlight of Ali's earnings report this quarter. And the caliber adjustment of international business is not large, can still refer to the comparison of historical data. * * * * This quarter, overseas retail businesses including Lazada, Aliexpress and Trendyol have achieved an astonishing growth rate of over 60%, far exceeding the market's general expectation of 30%-40% growth. Although the international wholesale business has basically zero growth, after adding up, the international e-commerce sector still achieved 41% growth and 22.1 billion revenue. * * * * According to the company's disclosure, the overall single volume growth rate of the international e-commerce business this quarter was around 25%, significantly lower than the revenue growth. Combined with the performance of companies such as SEA and Amazon, which we cover at the same time, Dolphin Jun believes that overseas e-commerce companies have generally taken measures to raise the liquidity rate one after another due to the recent slowdown in industry growth and huge profit pressure. As a result, Ali's international e-commerce business is likely to follow suit to improve the level of realization, while not hurting its own competitive landscape. * *! * * It is also worth noting that Ali has recently launched a fully managed and mainly cost-effective AliExpress Choice business similar to Temu. Considering the strong growth momentum of Temu and the high probability of overseas preference for low-priced goods due to inflation, the subsequent growth of Choice business is also worth looking forward. * * * * 5. target listing, rookie recorded in the group's internal income * * * as the group's second priority to be listed independently of the business, rookie logistics's income caliber began to include the group's internal and external customers two parts. Specifically, Cainiao's revenue this season was nearly 23.2 billion yuan, an increase of about 34% year-on-year, which was significantly better than the 15% growth in the previous quarter. Although the rookie sector, which is responsible for cross-border transportation, will benefit from the growth of overseas retail sales within market expectations, the rookie also performed better than expected because the actual growth rate of international retail sales was much higher than expected. * * * * In addition to the strong performance of overseas cross-border transportation, with the official announcement of Cainiao's entry into to C's distribution business and the possibility of further increasing its stake in Shentong to "backdoor" into the express delivery market, there is also much room for subsequent domestic logistics revenue to grow. * * * * Under the low base of the 6., the in-store business has been repaired well * * * * In the second quarter of last year, due to special circumstances, it had a greater impact on the in-store and in-home businesses that rely more on offline performance. And since the second quarter in the overall normalization of travel, the backlog of domestic residents to go out to play demand rebounded significantly, so Ali local life group principal to achieve income 14.45 billion, up 30% year-on-year, but also slightly better than market expectations. * *! 7. demand repair, its own slimming, Ali Entertainment also ushered in its own spring? This quarter, also because of the repair of cinemas, concerts and other consumer scenes, and the backlog of popular, quality works and events released, even the previously most marginalized Ali Entertainment segment achieved 36% revenue growth this quarter. At the same time, after the reform, Ali clerks only retained Youku, barley net and Ali pictures, and other businesses with unclear prospects were also thrown out of the body. After slimming down, it has turned losses into profits, and the subsequent business development and profits will be more traceable. 8. Aliyun is still in the pit and the rookie plate is similar, although Aliyun's internal business has not changed significantly, but in order to independently account for revenue, profit **, this quarter Aliyun in the revenue caliber also recognized revenue from within the group. Specifically, Alibaba Cloud achieved revenue 25.1 billion this quarter, still growing at a year-on-year rate of only 4%, better than the previous quarter's-3% growth, but the growth repair was the worst of all subsets. It also further highlights the need for Aliyun to introduce external shareholders to strengthen the business of government and enterprises. * * * * The biggest highlight of the 9.: all "younger brother" businesses have reduced losses or twisted profits * * In fact, the repair of the revenue growth of Ali's sub-sectors (except Ali Yun) is not the biggest two points of this Ali financial report. * * The real thesis changer is the overall loss reduction or profit reduction of all businesses except Tao Tian. Specifically: 1) Tao Tian Group's adjusted operating profit before amortization (EBITA) for the quarter actually increased by only 9% year-on-year, but was lower than the 10% growth in revenue, which shows that Taobao Tmall's profit margin is indeed slightly affected by subsidies and the competitive landscape. **As we'll see later, marketing spending did increase quite a bit this season. **2) But in addition to the days, regardless of international e-commerce, rookie logistics, local life, Ali cloud and Ali entertainment all showed a significant improvement in operating margins. Even businesses that were not selected by any sub-group and thus "abandoned" into the "All Others" classification, as well as "unallocated" costs at the group level, were also reduced. * * Due to time constraints, Dolphin Jun will not recover the specific profit situation of each sub-sector disclosed in the financial report.! **Why does Dolphin Jun think that the loss reduction of other" little brother "businesses is a key benefit? Because in the previous market valuation of Ali, only the value of the profitable business was considered for a long time, while other businesses have been refused to be valued. Dolphin Jun believes that the reason is that for long-term loss-making business, the market is willing not to make punitive valuation of losses, directly according to the profit valuation of Tao Tian has been "benevolent and righteous". **** It is somewhat unreasonable in the current market environment to have the market ignore the losses and not deduct the profits of Tao Tian, but also to have the market give additional incremental valuation to the loss-making business. **** And as other sub-groups gradually have their own stable earnings, the market will be given a reasonable incentive and a clear reference benchmark to give valuations to other sectors. Thus, even in the case of the competitive landscape of the business may not be significantly improved, but also can bring some upward valuation flexibility. **** Where does the overall loss reduction and profit increase of the 10. come from? Then what is the source of the overall loss reduction? First of all, After each sub-group operates independently and pays for its own profits and losses, the management and employees of each sub-group will certainly be better motivated to "survive" and have the right to start business more flexibly and independently. This is the fundamental reason for the overall improvement in operating efficiency and profits. * * and * * from the perspective of financial data, the gross profit margin under Ali's non-gaap caliber reached 39% this quarter, only a slight increase of 1pct over the same period last year. It can be seen that the increase in profits mainly comes from the control fee and the elimination of non-quality assets. * *! In terms of expenses, **the expenses under the Gaap caliber were significantly underestimated as the company significantly lowered its valuation of Ant Group, resulting in a one-time reversal of approximately $6.8 billion in equity incentives previously issued to employees. * * Therefore, we mainly look at the data under the non-gaap caliber, which shows that 1) * * * Sales and market expenses still increased by 10% year-on-year, reaching 27.2 billion, even exceeding the expected 26.6 billion under the market GAAP caliber. It can be seen that under various subsidies and drainage measures, the company's marketing investment is indeed growing, thus dragging down the profits of the Group. **2) After widespread layoffs, research and development costs decreased by about 4.5 percent year-on-year, which may be due to layoff subsidies, and management expenses also increased by about 14.5 percent in the quarter. However, if it is indeed the impact of layoffs, the subsequent management costs will probably decline rapidly.! ! As a result, the company's overall non-gaap net profit margin for the quarter improved by about 4pct compared to the same period last year, and the improvement of 3pct compared to the previous quarter was not very significant. **(Mainly because the profit margin of the highest proportion of the Tao Tian sector is declining, resulting in the improvement of other sectors is not significant at the group's overall level.) * ! dolphin jun's past related articles, please refer to: * * earnings season * * * may 18, 2023 earnings review * * * * * "has been grinding bottom not light? Ali really wants to fight this time!" * * * * * Call on May 18, 2023 * * * * * "After drawing up the organizational structure, Ali will have to work for another three years (minutes of the call) * * Call on February 24, 2023" minutes of Ali's call: "there are always people who make subsidies, but no one has posted changes" "Comments on the financial report on February 24, 2023" Ali "squat" has come, is "take-off" still far away? " * Interpretation of Financial Results on November 18, 2022 * * " Ali: Losses Are Only Paper Tigers, "Competition Dead End" Is Kill "

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

-

- November 18, 2022 financial report call * * "Ali:" actively preparing for the end of the epidemic " * * * August 5, 2022 financial report interpretation * * " saving food and clothing, Ali "giving up his life and running for money" * * * August 5, 2022 financial report call * * * Ali without user growth: staring at wallet share, seeking Quality and Efficiency (Minutes of Telephone Meeting) May 26, 2022 Telephone Meeting Recovery Needs Sustained Operation and Users Hope May 26, 2022 Financial Report Review After a 70% Fall, Ali Finally Has Dawn? " February 25, 2022 Telephone Conference" 6,000-word Minutes: Ali Underestimates, Buyback and Split Will Do Apart from Hard Striving "February 24, 2022 Financial Report Review" Ali Still in Trouble? Don't pick on such cabbage prices "November 18, 2021 financial report review" Ali's mobile internet era is over? "on November 18, 2021, the phone call" behind the deep fall, Ali struggled to explain the grand plan (summary) "on August 4, 2021, the phone call" after listening to Ali's meeting, maybe e-commerce really needs to adjust for some time "on August 3, 2021, the financial report review" Ali: firepower is still the same, the results "lose color" "* * depth:** January 19, 2023 ants ashore, Zhang Yong on the cloud, how far is Ali from revaluation? " **** January 18, 2023 " e-commerce final battle, Taobao fight too trembles? * * * * * * January 18, 2023 "* * the trend of attack and defense is reversed," Ali, Ctrip, Didi "will counterattack * * * September 30, 2022 * * * " fight more & only products: your poor days are good days " * * * September 22, 2022 * * * " Ali, meituan, fight more, all resigned? There is still a great fortune April 27, 2022 Ali vs Duoduo: After shopping, only coexistence? " April 13, 2022 " To Cycle "Decay", How Much Value Do Ali Tencent Have Left? " September 22, 2021" Kill Crazy Ali, Meituan and Pinduoduo, Is there a real barrier to e-commerce traffic after the scuffle? "April 16, 2021" 2021, "Total War" of Internet E-commerce "" Risk Disclosure and Statement in this article: Dolphin Investment Research Disclaimer and General Disclosure

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.