Small Tencent SEA: Backlash Surges After Survival with One Arm

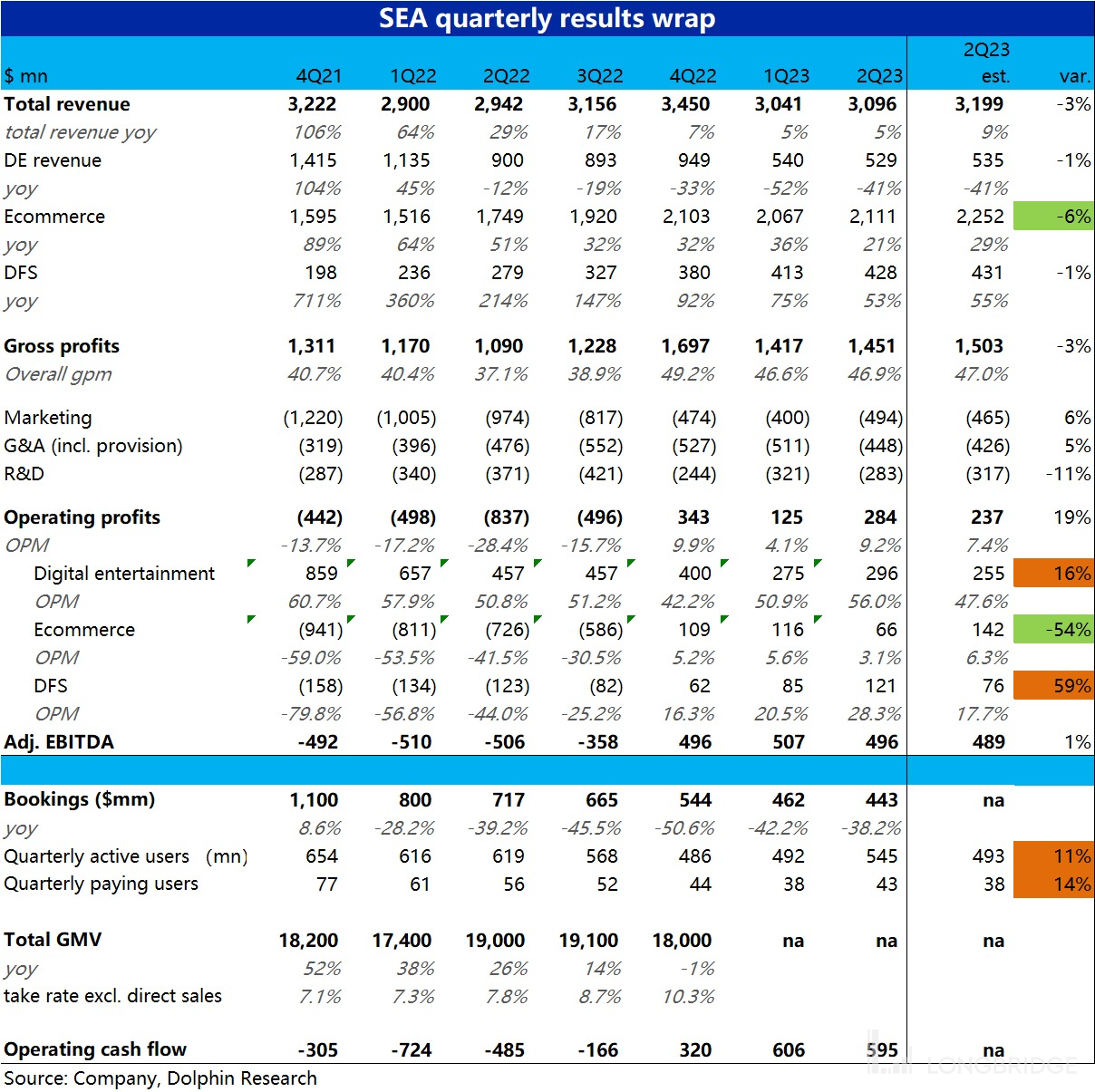

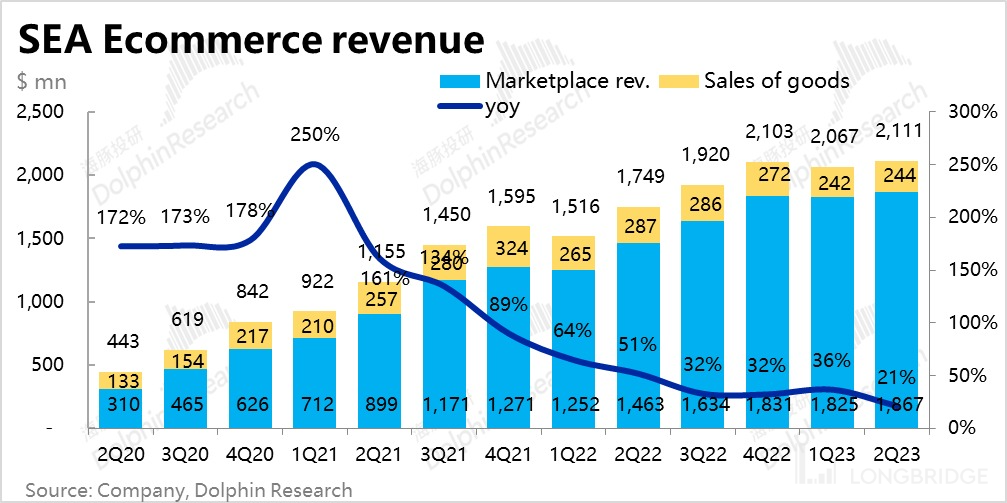

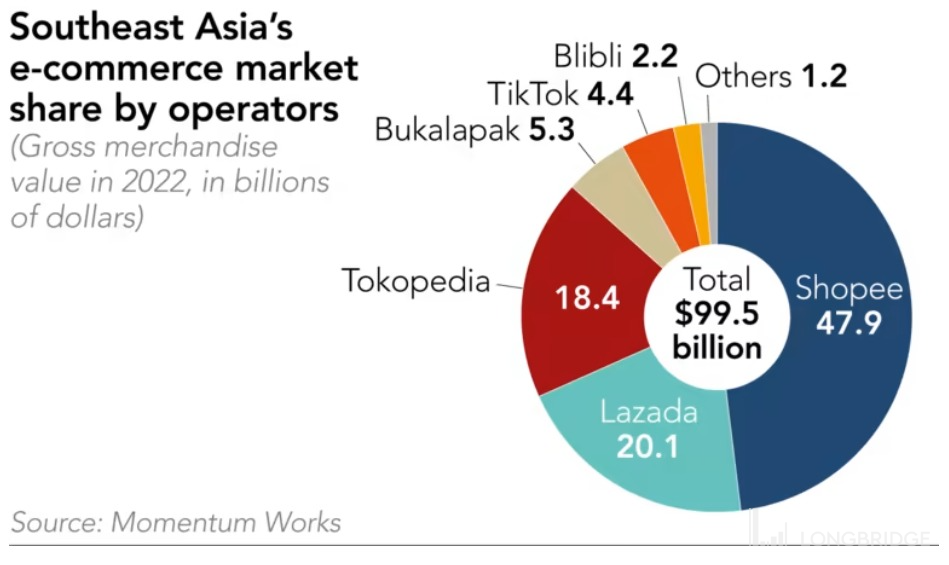

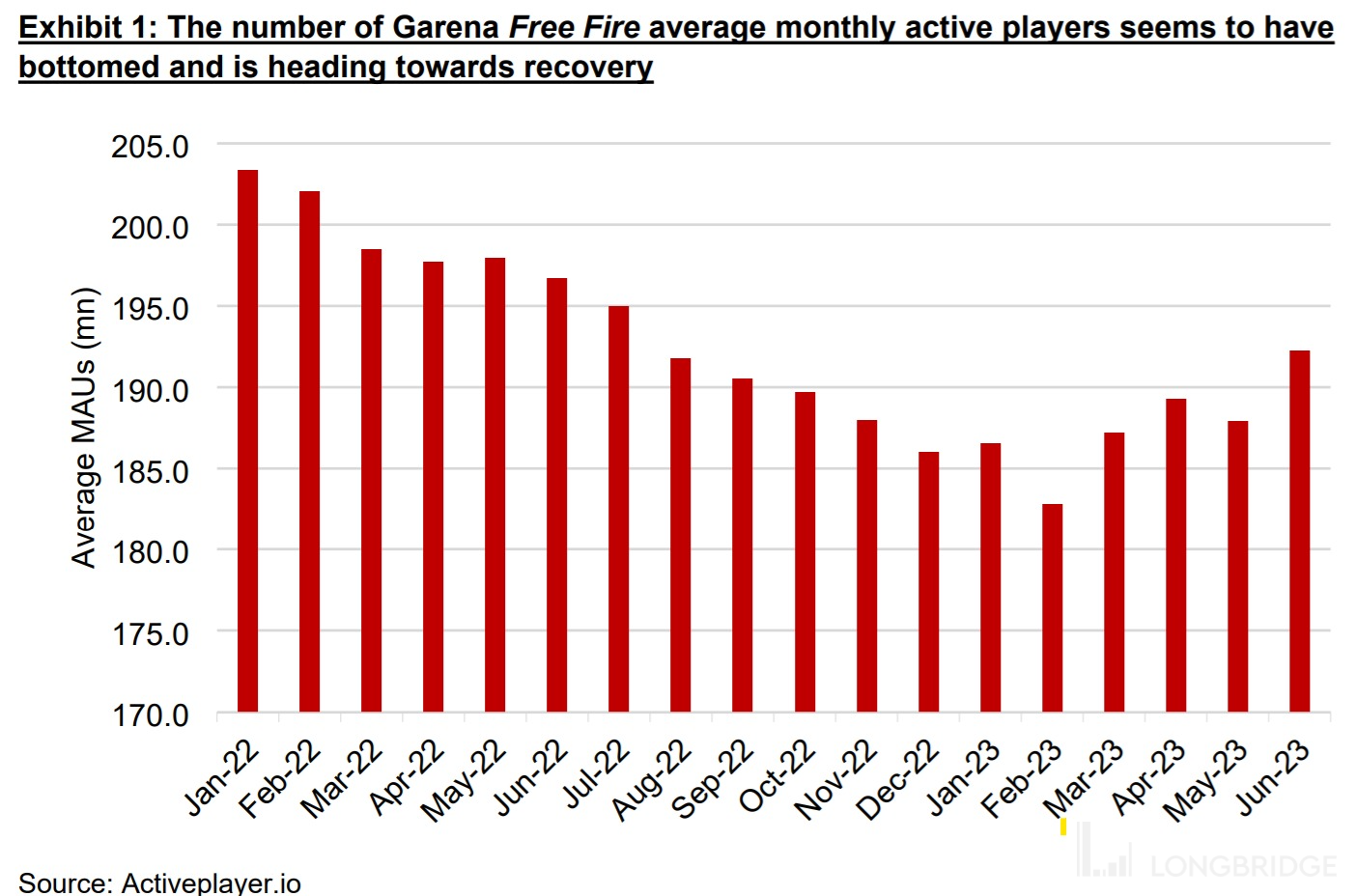

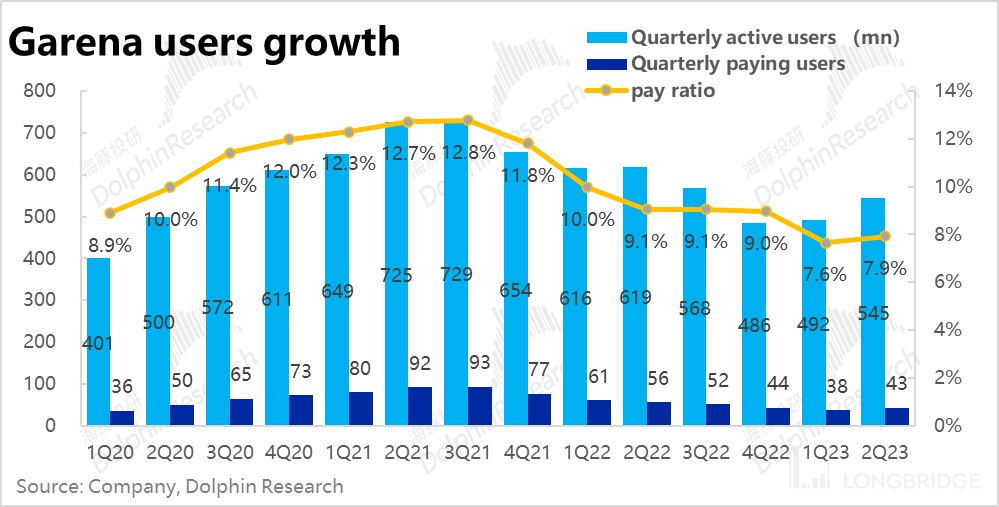

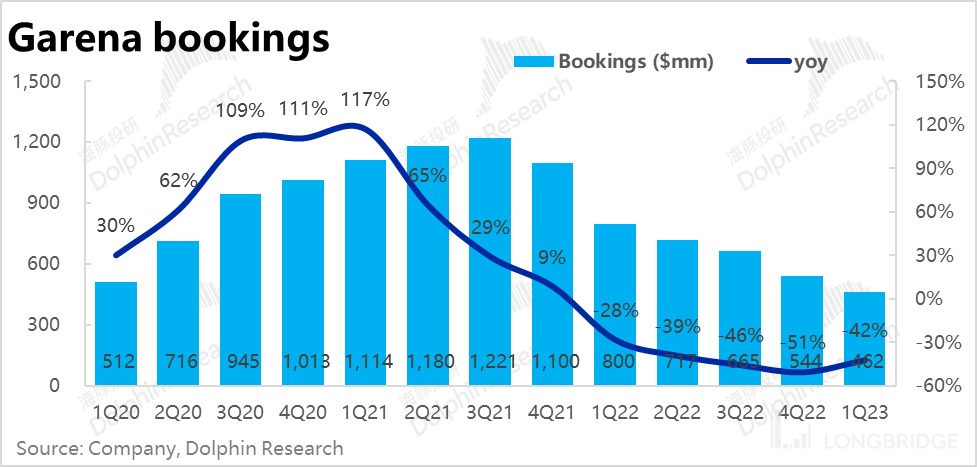

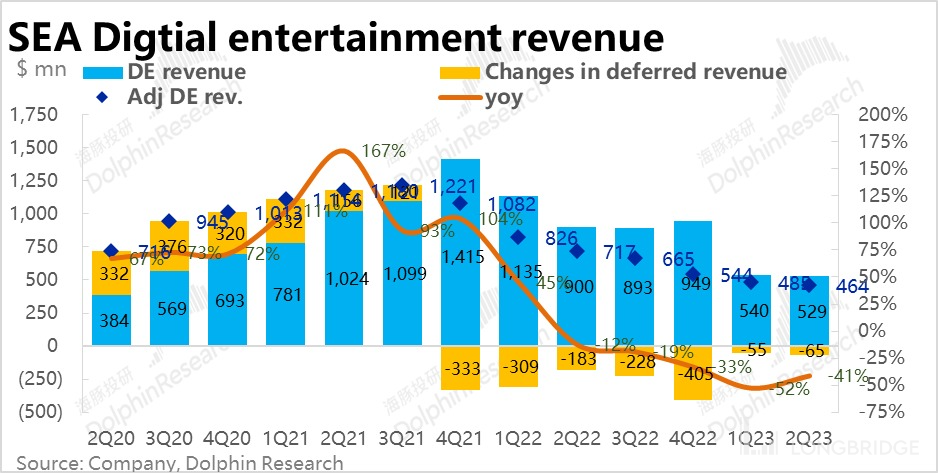

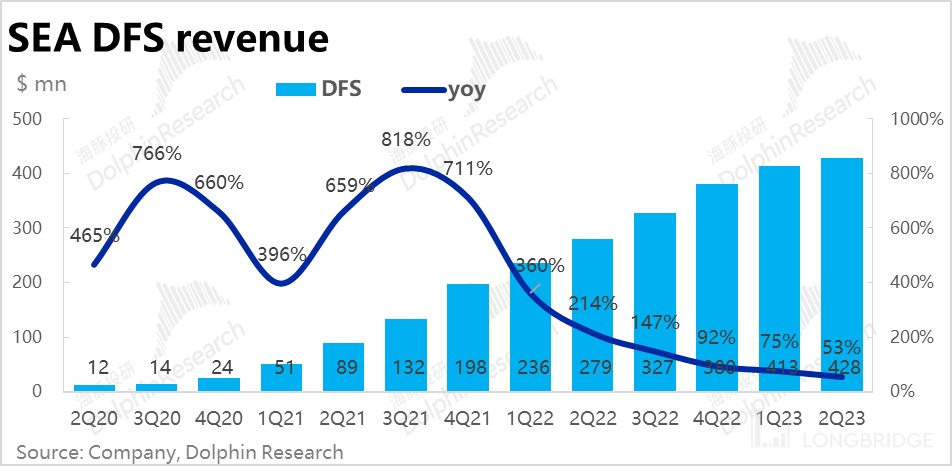

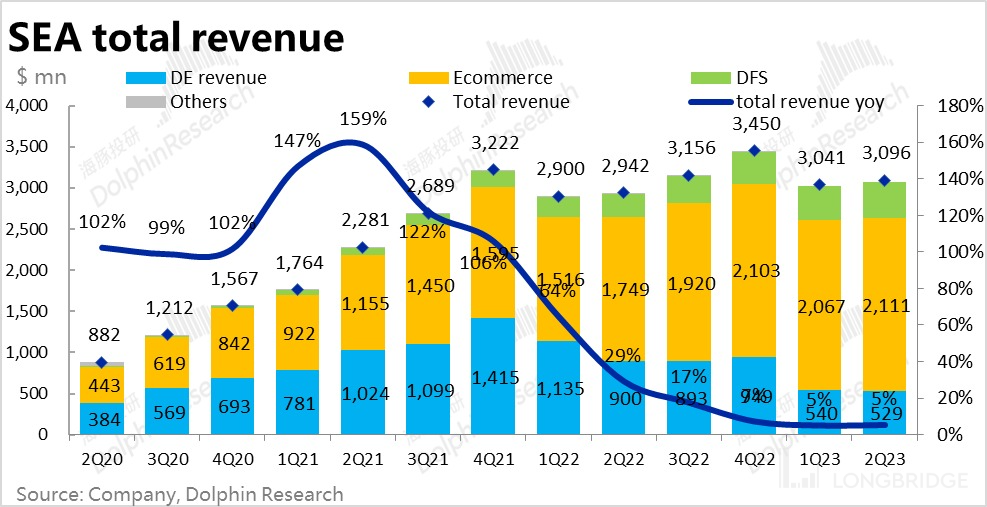

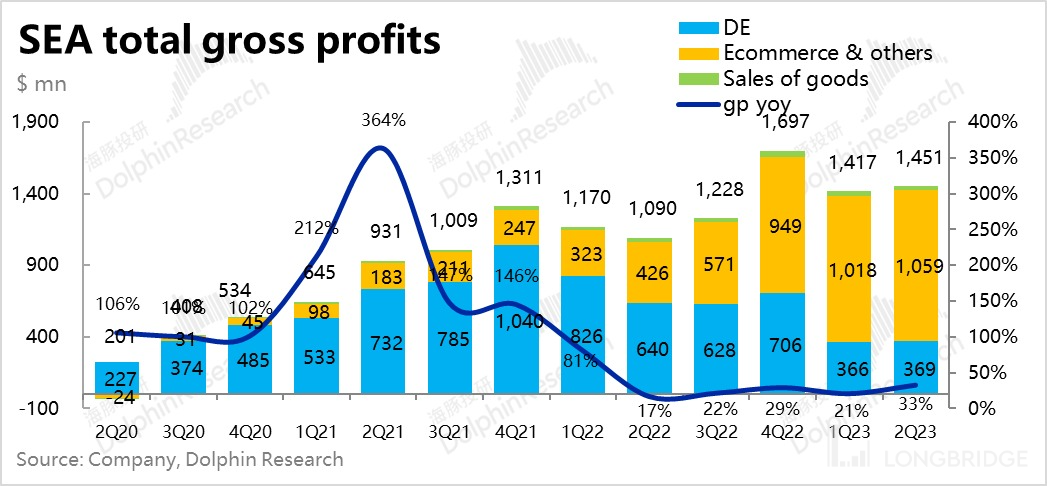

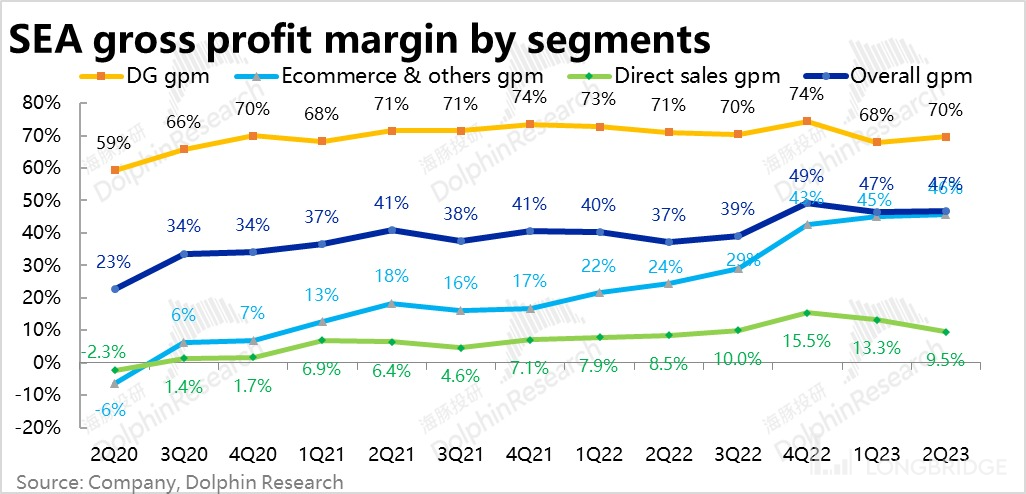

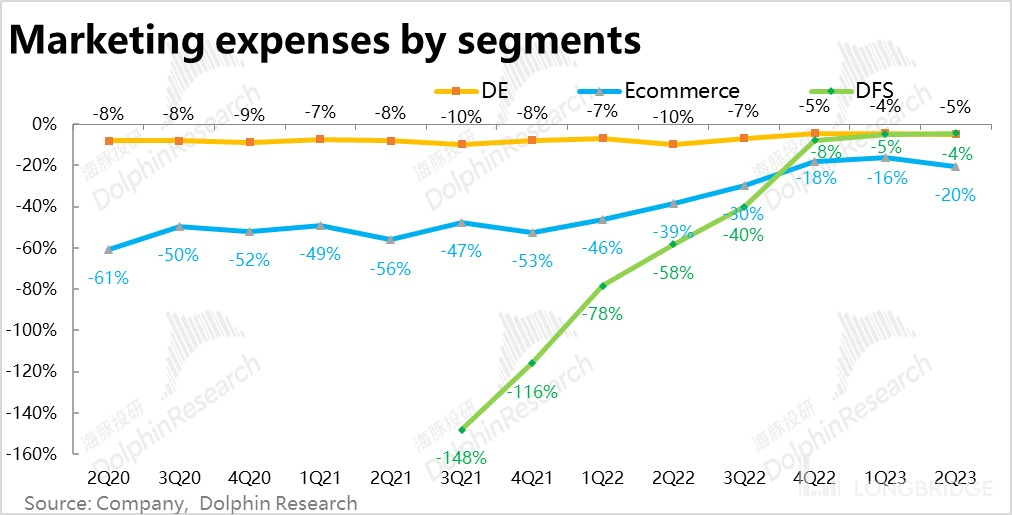

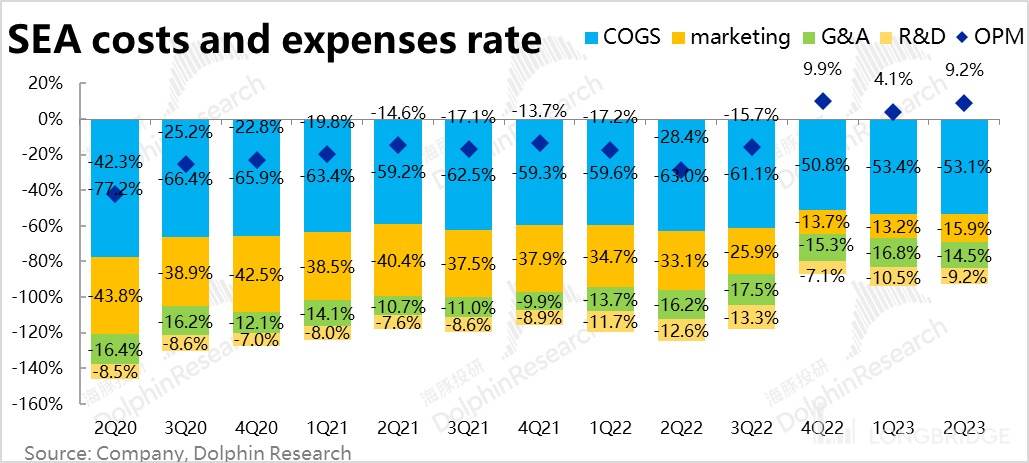

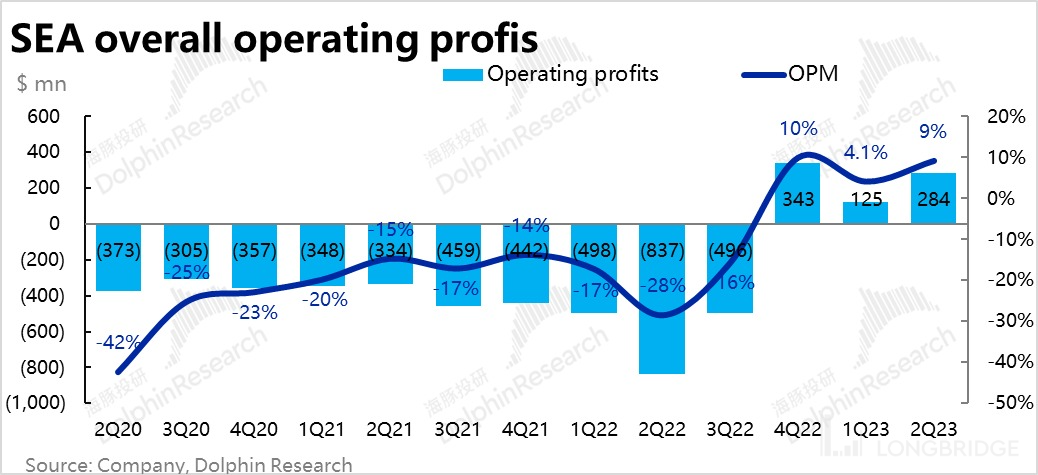

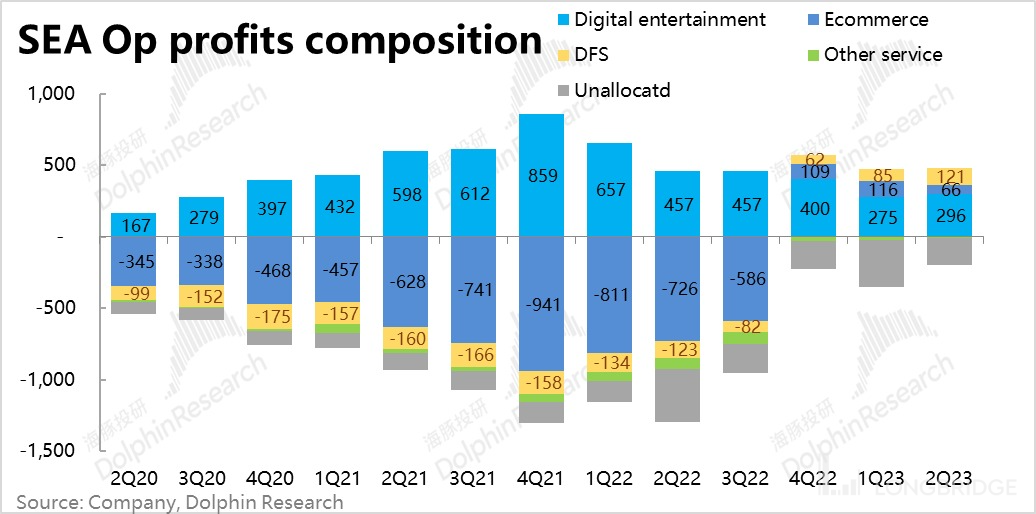

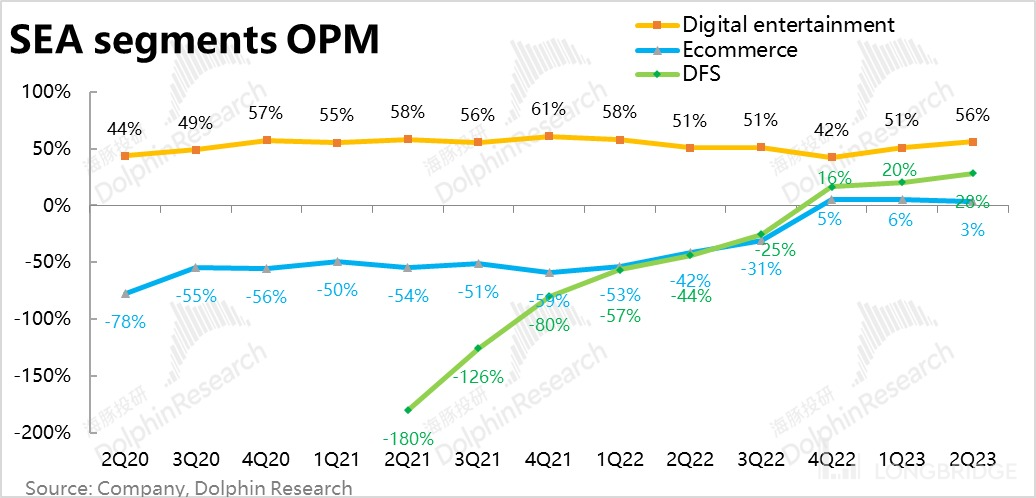

On the evening of August 15, before the U.S. stock market, SEA Donghai Group announced its financial report for the second quarter of 2023. Due to the unexpected but reasonable decline in revenue and profit of the e-commerce sector, the company's stock price fell sharply. The core points are as follows: * * 1. Revenue miss is unforgivable: * * Look at the overall performance first, * * Confirm that the total revenue is 3.096 billion yuan, which is lower than the market expectation of about 3.2 billion yuan. The year-on-year growth rate is also maintained at 5%, and there is no sign of improvement expected by the market. * * Although this quarter's * * operating profit was 0.28 billion US dollars, it was still significantly higher than the previous quarter * *. **Operating margins are back at 9%, close to last year's Q4 level. **But Dolphin Jun has also stressed many times that the market's emphasis on beat or miss of revenue is much higher than profit. The fact that revenue fell short of expectations was largely unforgivable, which was the main cause of the sharp fall in SEA's share price. * * 2. Shopee's backlash to quench thirst has come: * * and the biggest "thunder point" is that the company's * * most critical, highest valuation of the e-commerce sector Shopee this quarter in Topline and bottom-line both collapsed * *. This quarter **Shopee achieved revenue of $2.1 billion, significantly below market expectations of 2.25 billion revenue. * * The core platform revenue was 1.87 billion, and the year-on-year growth rate also dropped sharply to 28% from 46% in the previous quarter. * * At the same time, the company also said that the total order volume increased by 10% month on month. If the unit price of customers is basically unchanged, GMV still decreased by about 1%-2% year on year. Dolphin Jun believes that Shopee's e-commerce sector has been increasing its liquidity rate and reducing user subsidies, while helping the company quickly turn a profit, but it has also seriously devoured Shopee's competitiveness and growth potential. * * Although the management has realized the problem and increased investment to rebalance growth and profits, * * but it coincides with TikTok Shop's rapid expansion in the Southeast Asian market. After clarifying the business structure, Ali's investment in Lazada business is also increasing. As a result, Shopee, even if it increased its investment again, failed to return growth, resulting in a double loss of revenue and profit. More crucially, it has also severely damaged the market's expectations of Shopee's forward competitive landscape and market share. * * * * 3. Garena has a marginal improvement trend: * * From the high-frequency data already released, Dolphin Jun found that the number of monthly live users of Garena's most important game_Free Fire_has been continuously rising since March 23. Official data also show that the number of active users increased by 53 million and the number of paid users increased by about 5 million. The pay ratio also rebounded to 7.9 from 7.6 in the previous quarter, and Garena's gamers are picking up in size and activity. * * Therefore, although * * re-active players are not willing to pay, * * * Garena's confirmed running water this season is still falling * * to 0.46 billion yuan month on month. But **user recovery is a prerequisite for subsequent inflows and revenue recovery. Final Game segment revenue for the season was 0.53 billion, down only about $11 million from the previous quarter, and was not far from the 0.535 billion expected by the market. **** 4. SeaMoney finance pursues quality rather than growth: After the sector has experienced leapfrog growth in the past 3-4 quarters, growth momentum has shown signs of slowing this quarter * *. * * This quarter's revenue was about 0.43 billion yuan, up only about US $15 million from the previous quarter. **At the same time, the company disclosed a pending loan balance of $2 billion million, unchanged from the previous quarter and also largely stopped growing. However, **credit impairments were 0.153 billion this quarter, down from last quarter's 0.177 billion, indicating a steady improvement in the quality of the lending business, matching the rapidly improving operating profit of the segment. **** 6. Marketing expenses increased again: **Corresponding to the company's desire to re-boost the growth of the e-commerce sector and its goal of attracting players back to Garena's games, the company's marketing expenses began to expand this quarter. Among them, the marketing expense rate of the * * e-commerce sector increased significantly to 20% from 16% in the previous quarter, confirming the growth of the company's promotion or subsidy to consumers in Shopee. The marketing rate for the * * game sector also increased slightly from 4% to 5% month on month. In the end, * * total marketing expenses for the quarter were $0.49 billion, higher than the expected 0.47 billion. **As for administrative and research and development costs, the trend of contraction continued, with their expense rates falling by 2.3pct and 1.3pct, respectively. * * 7. E-commerce profits nearly halved, and the losses did not return to growth: * * By sector, * * The operating profit of the e-commerce sector declined significantly month-on-month, only 66 million yuan this quarter, close to halved, and also lower than the 0.14 billion expected by the market. The re-increase in investment has significantly dragged down the profits of the sector. Profits in the gaming sector, on the other hand, were steadily repaired to $0.296 billion for the quarter, up slightly from the previous quarter and slightly above the expected 0.26 billion. **Profits in the financial sector, on the other hand, improved significantly, with operating profit of 0.12 billion for the quarter, far exceeding the expected 0.076 billion, and an increase of more than 40% from the previous quarter, which shows that the main goal of the financial sector at present is indeed to improve quality, rather than to pursue scale too quickly. * *! Long Bridge Dolphin Jun view: Overall, we can see that the most critical issue in this earnings report is the simultaneous decline in revenue and profits in the e-commerce sector. In fact, since the fourth quarter of the year, when the company turned losses into profits by greatly increasing the e-commerce realization rate, Dolphin Jun has already stressed that Shopee, as a platform with the same extreme cost performance as its main competitive advantage, will greatly increase the draw for merchants and reduce subsidies to users, which is bound to seriously affect the company's attractiveness and competitive advantage. While management has noted the negative impact of the strategy and has tried to rebalance growth and profit priorities. But the landscape of the Southeast Asian e-commerce market is not yet solid, and the size of the companies behind Lazada and TikTok is absolutely not to be taken lightly. Therefore, Dolphin Jun believes that Shopee may subsequently fall into a domestic e-commerce-like internal volume pattern (of course, the degree of probability will be lighter), in a certain period of time will fall into the dilemma of revenue and profits at the same time are difficult to significantly upward. Competing the hard but critical internal skills of execution and operational efficiency may become the key to follow-up. But fortunately, the company's game sector has shown signs of an inflection point, and the profits of the financial business are also steadily increasing. As long as the game sector is no longer thunderous, the company has enough cash flow and profit space to re-enter the competition in the e-commerce industry. Without being dragged down by other sectors. * * The following is a detailed interpretation of the financial report: * * * * 1. Shopee: After the crazy cash-out, the inevitable backlash has come * * Since the second half of 2022, SEA has continuously increased the liquidity rate and reduced user subsidies to its * * Shopee e-commerce sector under great pressure. Although it has helped the company quickly turn losses into profits, it has also seriously backfired Shopee's competitiveness and growth potential. **** Shopee achieved revenue of $2.1 billion for the quarter **, **significantly below market expectations for 2.25 billion revenue * *. Under competitive pressure, Shopee's actual growth was worse than expected. The core platform revenue was 1.87 billion, with year-on-year growth falling sharply to 28% from 46% in the previous quarter. Although the company also did not disclose GMV data, it said that * * the total order volume increased by 10% month on month. If the unit price of customers is basically unchanged, GMV still decreased by about 1%-2% year on year. * *! In fact, after management saw that the company's overall earnings had turned positive and Shopee's growth had declined rapidly, **has previously indicated that it would take a more balanced view of the relationship between profits, inputs and growth. The Shopee sector operating profit fell significantly month-on-month, also confirmed the company's increased investment. **But the problem is that this year, Tiktok Shop has significantly increased its focus on the Southeast Asian market, and Ali is increasing its investment in Lazada after clarifying its business structure. The fact that Ali's international business grew by more than 60% in the second quarter, and that Tiktok Shop has become a Top3 player in several countries in Southeast Asia, also validates the acceleration of Shopee's competitors. As a result, **the company's previously aggressive liquidity gains and a marked increase in competition have caused Shopee's growth to slide even as it re-invests. Instead, it led to a double loss in revenue and profits. * *! 2. Garena game but hope of an inflection point? **This quarter, the" pillar "of the Shopee sector was significantly worse than expected, and the almost" almost rotten "Garena game sector showed a marginal improvement trend. * * First of all, according to third-party high-frequency data, the number of monthly live users of Garena's most important game_Free Fire_has been rising continuously since March 23.! and official data this season also show that the number of active users increased by 53 million and the number of paid users increased by about 5 million. The pay-to-pay ratio also rebounded to 7.9 percent from 7.6 percent in the previous quarter, showing that Garena's gamers are picking up in size and activity. * *! However, although players are returning, * * re-active players are not willing to pay much * *, with the average single-paid user spending $10.3 this season, down significantly from $12.3 last quarter. ! Although the user scale has rebounded, * * Garena's confirmed running water this quarter is still falling month on month * *, with 0.46 billion yuan this quarter significantly lower than 0.54 billion yuan last quarter. **But in any case the user recovery is a prerequisite for subsequent inflows and revenue recovery. **In terms of year-on-year growth, the loss is down 42% this quarter, which has narrowed from last quarter, also indicating that the inflection point in the gaming sector may be coming.! Reflected in the financial data, as the flow of water continues to decline, the revenue of the game sector this quarter was 0.53 billion, a decrease of only about 11 million US dollars from the previous quarter, and the 0.535 billion gap with the market expectation is not big. Although the game sector is still at the bottom of the performance in absolute terms, signs of marginal improvement have emerged. * *! 3. SeaMoney Digital Finance continues to grow After the SeaMoney shift in business focus to lending, the sector's revenue has grown by leaps and bounds in the past 3-4 quarters, but **growth momentum has shown signs of slowing this quarter * *. * * This quarter's revenue was about 0.43 billion yuan, up only about US $15 million from the previous quarter. **In terms of operating data, the company disclosed that the outstanding loan balance at the end of the quarter was $2 billion, which was the same as the previous quarter, and there was no significant increase. However, operating profit in this sector is improving rapidly **, with credit impairments 0.153 billion this quarter, down from last quarter's 0.177 billion, also indicating a steady improvement in the quality of the lending business (although size growth has largely stagnated). * *! 4. e-commerce sector dragged down total revenue less than expected As the largest e-commerce sector accounted for significantly lower revenue than expected, other sectors were unable to compensate for the excellent performance. * * SEA's final confirmed total revenue for the quarter was 3.096 billion yuan, which was lower than the market expectation of about 3.2 billion yuan. Year-on-year growth is also remaining at a low of 5%, with no signs of improvement. * *! and the company's 0.428 billion gross profit for the quarter was also lower than expected due to lower-than-expected revenue 0.431 billion. Actual gross margin was 46.9 per cent, also slightly below expectations of 47 per cent. Specifically, **mainly the gross margin of proprietary sales revenue fell sharply from 13.3 percent to 9.5 percent month-on-month, while the gross margin of other sectors was flat or up month-on-month. It can be seen that the company should have increased the discount on the selling price. * *! ! Significant growth in 5. marketing promotion and restraint in other expenses Corresponding to the company's desire to re-boost growth in the e-commerce sector and its goal of attracting players back to Garena's games, we saw the company's marketing expenses begin to expand this quarter. Among them, the marketing expense rate of * * e-commerce sector increased significantly to 20% from 16% in the previous quarter, confirming that the company has indeed increased its promotion or subsidies to consumers. **Marketing rates for the gaming segment also increased slightly from 4% to 5% QoQ. Therefore, the total expenditure on marketing expenses for the quarter was $0.49 billion, which was higher than the expected 0.47 billion, showing that the investment was stronger than expected. * *! while administrative and research and development costs continued the trend of contraction, with management fees falling by 2.3pct, and the reduction in credit impairment mentioned above was also one of the drivers of the decline in management costs. R & D rates also fell by 1.3pct.! On the whole, although the revenue and gross profit were lower than expected, the company's expense investment did not turn around in an all-round way, and the total expenditure remained stable month on month. Therefore, SEA realized an operating profit of US $0.28 billion in this quarter, which was still significantly higher than that in the previous quarter. Operating margin returned to 9%, close to last year's Q4's all-time high.! * * 6. profit is actually not bad, all because the game drag * * sub-sector, you can clearly see that * * e-commerce sector operating profit fell significantly month-on-month, this quarter is only 66 million yuan, close to halving, but also lower than the market expected 0.14 billion. It can be seen that the re-increase in investment has obviously dragged down the profits of the sector, but it has not been able to exchange for the acceleration of growth. * *! while * * profits in the gaming sector were steadily repaired * * to $0.296 billion for the quarter, up slightly from the previous quarter and slightly above the expected 0.26 billion. As for the * * financial sector profits are significantly improved, the quarter's operating profit of 0.12 billion, far exceeding the expected 0.076 billion, the ring improvement is also more than 40%, it can be seen that the current main goal of the financial sector is indeed to improve quality, rather than too fast the pursuit of scale. * *! * * Dolphin Investment Research SEA (Donghai Group) Past Research: * * May 17, 2023 Telephone Conference "SEA: Don't Tangle with Short-term Profits, Look More at Long-term Profits" May 17, 2023 Financial Report Review "Little Tencent SEA: Again Dragged into the Abyss by Bad Games?" March 8, 2023 Telephone Conference "SEA: No More Toss, 23 Years Still Profit First" March 8, 2023 Financial Report Review "All for Survival! Small Tencent SEA Breaking Arm to Survive" On November 16, 2022, the telephone conference "SEA: Tighten your belt, survival is the primary goal (3Q22 minutes)" On November 16, 2022, the financial report commented "The game sucks, Shopee Jedi to survive, SEA can return to the light?" August 17, 2022 Telephone Conference "SEA: Regardless of Scale, Everything Takes Efficiency First (Minutes of Telephone Conference)" August 17, 2022 Financial Report Review "Growth Without Sudden Losses, What Rescue Valuation Does Sea Take" May 17, 2022 Telephone Conference "Game Business Should Be Diversified, E-commerce Business to Profit (SEA Call Minutes)" Financial Report Review on May 17, 2022 "SEA: Game" Old ", E-commerce to Support the Field Alone" * * Risk Disclosure and Statement of this Article: * * Dolphin Investment Research Disclaimer and General Disclosure

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.