Crude oil, U.S. Treasury bonds, and the U.S. dollar are all suppressing emerging markets

美債利率持續上升,推動美元走強,導致新興市場股市承壓。2025 年以來,市場從"特朗普交易"轉向"二次通脹"交易,黃金和原油價格反彈。美國服務業數據回暖,12 月服務業 PMI 創 33 個月新高,非農就業新增 25.6 萬人,超出預期,顯示經濟韌性。

美債利率,太強

進入 2025 年以來,市場似乎從如火如荼的 “特朗普交易”,又重新切回 “二次通脹” 交易,有以下幾個跡象:

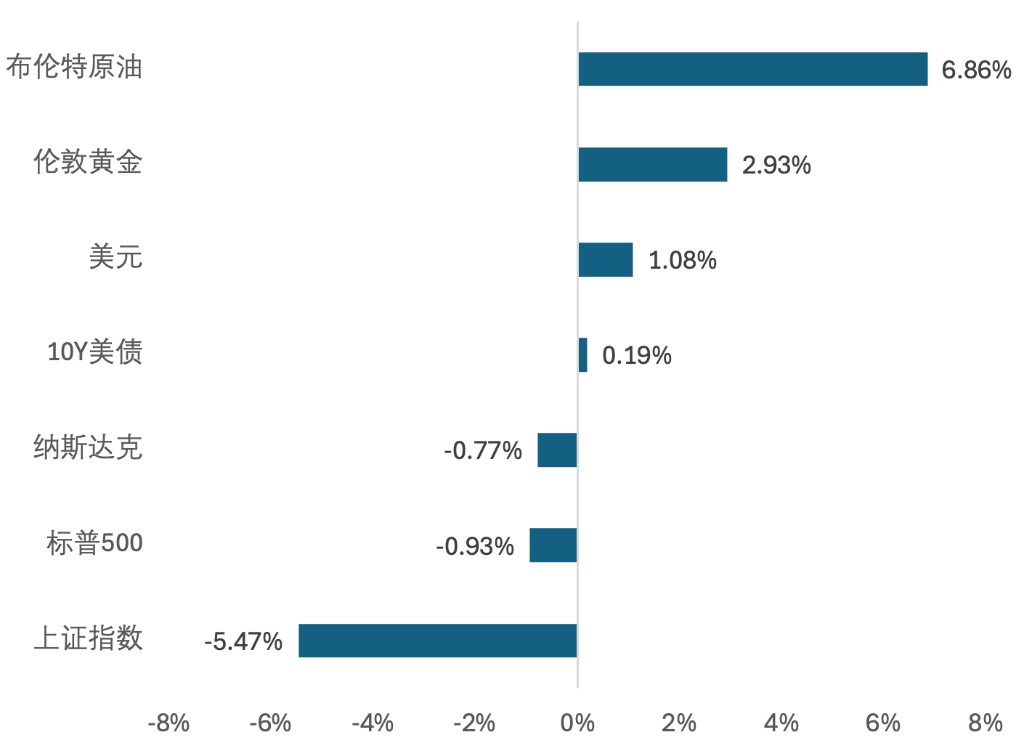

1)美元與美債收益率仍在上漲,但此前較弱的黃金、原油價格也開始反彈;

2)美股開始因美債利率走強而現如調整,部分新興市場股市則跌幅更甚。

圖:2025 年至今,各類資產漲跌幅(注:10Y 美債為收益率上行幅度)

要理解這一邏輯切換,就要明白美債是當前的 “風暴之眼”。

為何美債利率一路強勢?

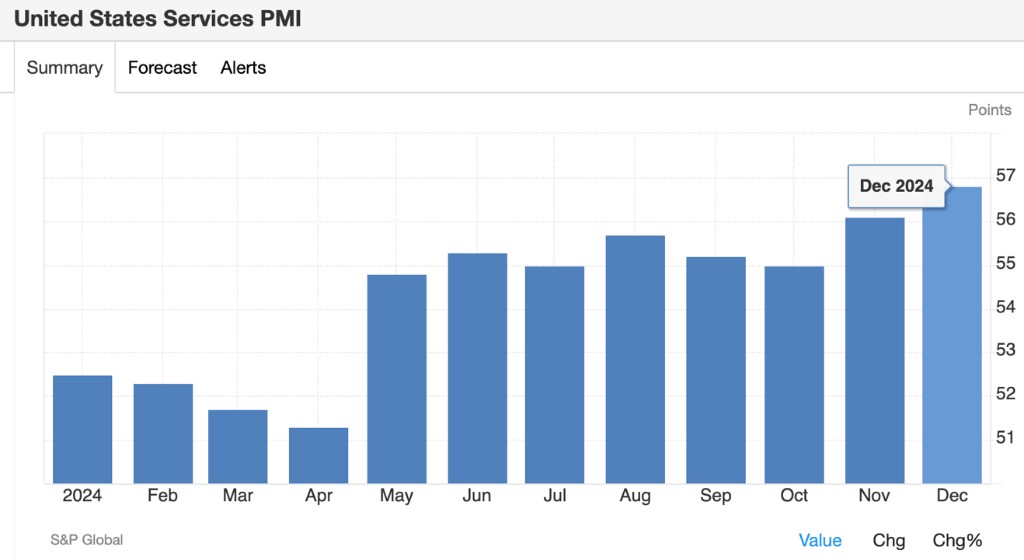

美國服務業數據全面回暖

美債利率繼續上行,首先是經濟數據驅動。

上週公佈的一系列美國經濟數據,均在向市場傳達服務業韌性的信號。

一方面,1 月 6 日率先公佈的標普全球美國 12 月服務業 PMI 終值錄得 56.8,雖小於初值 58.5,但仍創下 2022 年 3 月以來的 33 個月新高。

從分項看,就業分項指數終值升至 51.4,創 2024 年 7 月以來的終值新高,結束萎縮趨勢;新商業分項指數終值也創下 2022 年 3 月以來的終值新高。

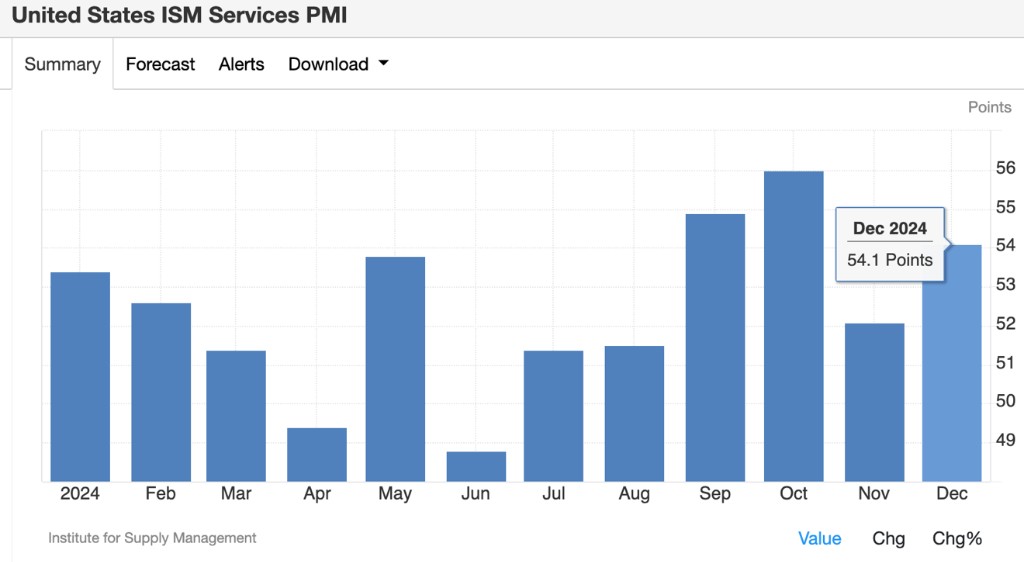

另方面,1 月 7 日公佈的美國供應鏈管理局(ISM)口徑下的 12 月服務業 PMI 錄得 54.1,超過市場預期值 53.5 及前值 52.1。

值得一提的是,價格端來看,Markit 服務業 PMI 與 ISM 服務業 PMI 分項中的價格指數在 12 月表現都出現上升,尤其 ISM 服務業 PMI 分項中衡量原材料和服務業支付價格的指標大幅上升 6.2 個點,飆升至 64.4,創下 2023 年初以來的最高水平,這意味着服務業面臨巨大成本壓力。

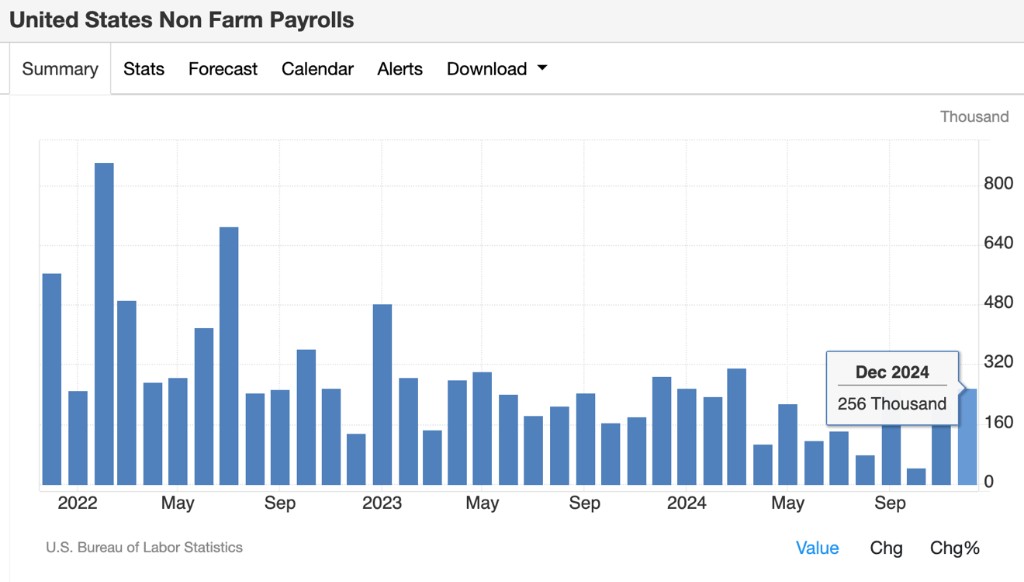

進一步夯實美國經濟強勢邏輯的,是週五的非農就業報告。

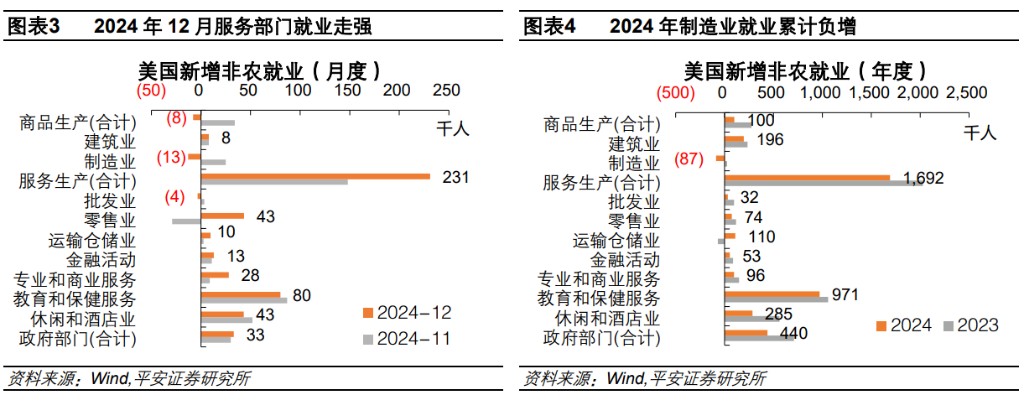

12 月,美國非農新增就業錄得 25.6 萬人,創九個月最大增幅,遠遠超出預期的 16.5 萬人,且高於媒體調查多數經濟學家預期。

從行業來看,製造業就業明顯弱於服務業,商品生產部門環比小幅負增、全年第三次負增長,而服務生產部分就業大幅增長 23.1 萬人,錄得全年最佳。

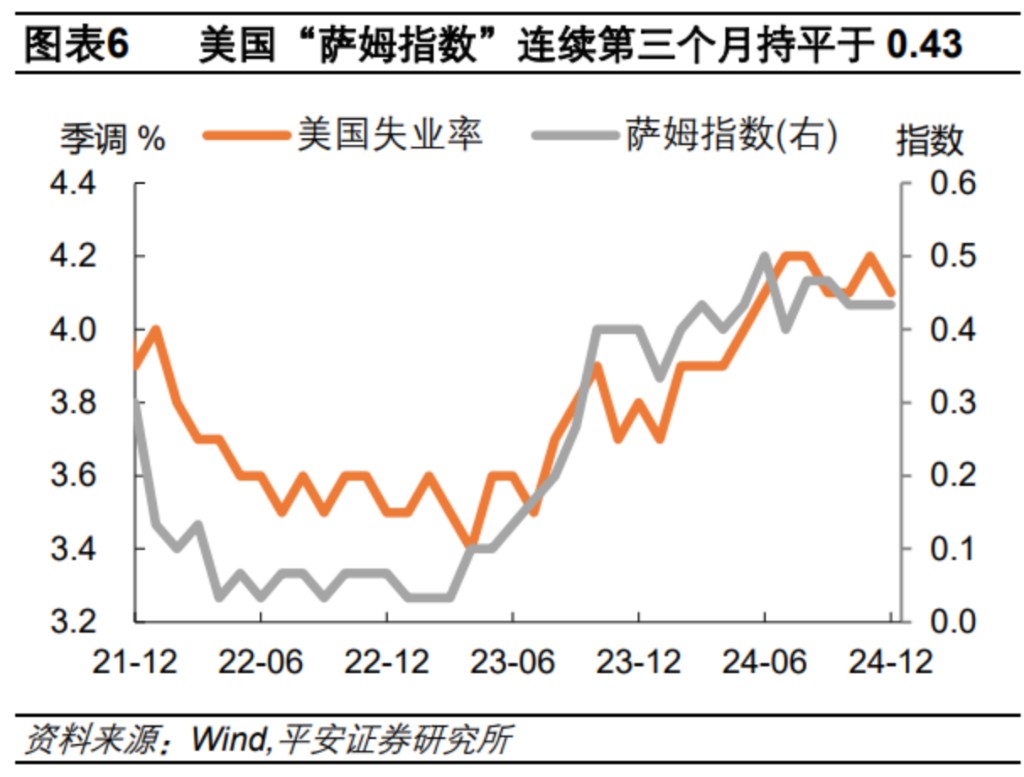

此外,12 月美國勞動力人口環比增長 24.3 萬人,失業人數環比下降 23.5 萬人,因此失業率下降至 4.1%,“薩姆指標” 則連續第三個月持平於 0.43,保持在警戒線下方。

毫無疑問,這是一份非常強勁的就業報告。

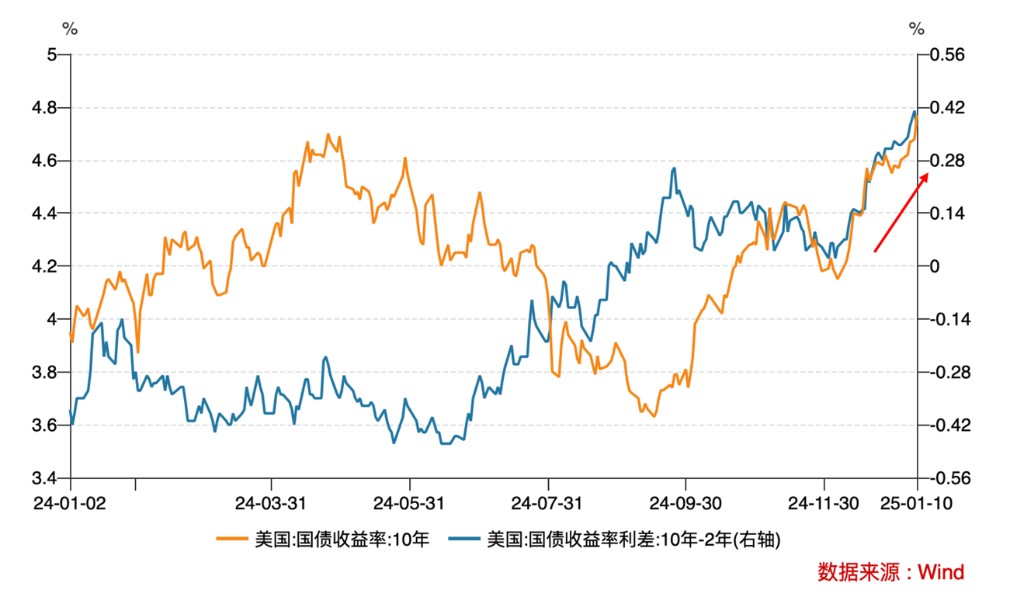

服務業增長強勁,推高了美國中性利率,也抬升了美債期限溢價。

12 月至今,10 年期美債利率上升了 59 個基點,而美債 10Y-2Y 利差擴大了 32 個基點。

另一方面,美國與歐洲、英國等的基本面差異也作用於匯率上,助力美元指數走強。

從美聯儲到市場,都在確認 “二次通脹”

1 月 9 日,美聯儲 12 月 FOMC 會議紀要公佈。

紀要中顯示,“幾乎所有” 美聯儲官員都認為通脹的上行風險有所增加。

此外,紀要多次提到了移民和貿易政策的變化可能對美國經濟產生的影響,並提示未來的降息步伐確實可能會放緩。

而市場方面,則定價得更加極致。

最新公佈的密歇根大學通脹預期數據顯示,美國 5-10 年期通脹預期上漲至 3.3%,與 2022 年 6 月齊平,創 2008 年以來新高,大幅高於預期的 3.0%,12 月前值為 3.0%。1 年通脹預期初值 3.3%,大幅高於預期的 2.8%,12 月前值為 2.8%。