Reviewing the ups and downs experienced by the U.S. stock market over the past decade [Fu Peng Says 12]

本文回顾了过去十年美股的走势与波动,强调了 2012 年以来的重要节点和市场变化。2015、2016 年美国及全球格局的转变,低利率和居民部门出清推动了市场发展。疫情成为催化剂,2018 至 2019 年间市场波动加剧,直至疫情前才稳定。文章还提到未来将以英伟达为例进行具体复盘。

“ 交易桌前看天下,付鹏说来评财经 ”

《付鹏说·第五季》重磅来袭!立即订阅

—

本期内容

>>本文仅限作者观点,点击上方视频收看!

交易桌前看天下,付鹏说来评财经。

本期付鹏说接上一期的内容继续聊美股近 10 年的复盘,一起回顾一下过去十年美股的走势和波动率的情况。

早在 2012 年,我就开始与中国机构的朋友们进行记录性的沟通交流,期间经历了很多重要的节点,这些都成为了我们共同的回忆。同时,我也一直在社交媒体上持续分享相关内容,所以很多回忆的节点在过往的历史中都是可以追溯的。

从 2015、2016 年开始,美国以及全球的世界格局都在发生巨大的转变,而美国的这种变化并非一蹴而就。随着从上到下的整体变革,以及 2008 年金融危机后美国居民部门的有效出清,其潜力逐渐在市场中显现。

2020 年疫情的爆发,成为了一场重大共振性的催化剂。而在这之前,市场是相对比较温和缓慢的。在 2015 年、2016 年时,美国的低利率以及居民部门出清后的债务和杠杆,已经在推动早期的市场出清。当然,在技术的这条线上,在之前【美股大师课】上已经和大家具体讲过产业周期和技术迭代下的美股分析方法,之后也会以英伟达为例具体复盘。

我们看到,在 2015、2016 年,市场经历了特朗普上台以及中国的冲击,之后市场平稳延续至 2018 年。在此期间,单纯从利率角度看,美国从耶伦任期末期开始小幅加息。这一阶段,从经济、利率、出清到技术早期,都已初具雏形。

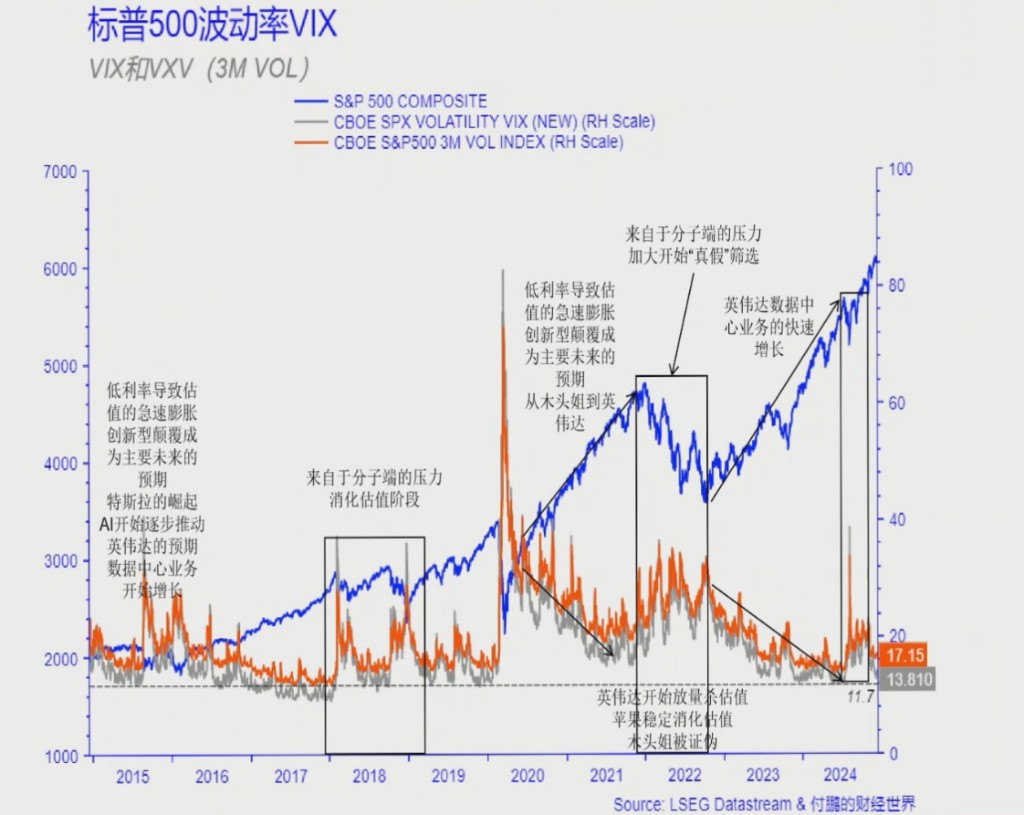

然而我们从下图上能看到:市场在 2018 年至 2019 年时波动率较高,美股呈现扩散性形态,直至疫情前才真正稳定下来。大家可能会认为这是疫情带来的冲击,因此可以忽略。但实际上,在 2018 年至 2019 年这将近两年的时间里,美股一直停滞不前,从 2019 年后市场才开始逐渐推动发展。

当时我们曾讨论过这个问题,我认为美股可能看似创新高后又大幅下跌,你以为要崩盘了,它却又慢慢创新高。但它是否会就此结束?并没有,它又开始下跌,呈现出扩散性状态,市场波动率随之放大。

当时,鲍威尔先是加息,随后又开始降息,这一阶段正好对应美国降息时期——那时美国经济的韧性尚未充分展现。无论是技术推动,还是特朗普上台后政治右翼化带来的变化,包括关税、贸易战等,都还未直接产生结果,所以经济韧性表现不强。那么,利率抬升的可持续性就会比较差。

但美国经济的基础其实已经奠定,包括技术早期发展、政治的积极变化,以及 2008 年金融危机至 2014、2015 年对美国相关运营部门的出清——基础是有的,只是韧性还未显现。

疫情后,虽然很多人从微观角度认为美国经济是靠财政政策推动,但有时因既是果,果既是因。若自身基础不牢,即使吃再多补药或亢奋药也无济于事;而若底子修复过来了,遇特殊事件时,潜能便可能被激发。

疫情爆发后,爆发式的低利率状态从 2020 年延续至 2021 年,大约有一年半时间。这期间,技术从早期走向裂变。其实我认为:到 2020、2021 年,技术裂变已初现端倪,英伟达的例子可加以佐证。低利率环境对技术裂变起促进作用,同时在财政补偿和利率影响下,居民部门和政策韧性再次被激发出来了。从那时起,美股真正意义上的长牛趋势才开始展开——这就是疫情后的重要性。

到了 2021 年底,波动率上升,美股下跌。这一期间,我多了很多炒币的粉丝,币圈很多朋友从这时开始关注我。在 2021 年底,我们讨论木头姐和比特币时,我曾表示:木头姐采用的是二级市场中的一级投资策略。而比特币到底是什么,至今我们仍未完全理解其本质,但从我的观察来看,它与利率存在一定关联。

如果说疫情之后,美国逐步进入常态化阶段,那么利率抬升在裂变节点中势必引发一波杀估值现象——这种状态可能会推动某种转化,即技术从早期的估值状态向价值状态切换,后续我们可以深入探讨这一点。

当时,英伟达、比特币、木头姐都经历了一波暴跌,比特币更是跌至 2 万多美元。然而,在利率抬升、杀估值结束后,市场进入价值阶段,波动率持续下降,木头姐表现低迷,而英伟达和比特币却重新创下新高,大幅上涨,市场整体波动率也随之下降。这种上涨与之前的上涨有着本质区别,完成了一次重要的转换。

综合过去十年来看,从早期解决问题,到从底层居民部门、中间内政外交以及技术维度这三个方向着手,可视为全要素的准备阶段。在第一阶段,美国的经济韧性不足;随着疫情爆发,促使韧性开始展现;经历杀估值后,最终展现出韧性和价值——这一系列路径符合完整的逻辑和路径。

风险提示及免责条款

市场有风险,投资需谨慎。本文不构成个人投资建议,也未考虑到个别用户特殊的投资目标、财务状况或需要。用户应考虑本文中的任何意见、观点或结论是否符合其特定状况。据此投资,责任自负。