CPI continues to rebound, but core CPI has decreased. The market is very happy, but perhaps a bit too early to celebrate

In December, the U.S. CPI rose by 2.9% year-on-year, and the core CPI rose by 3.2% year-on-year, both lower than expected. Market expectations for a rate cut by the Federal Reserve have increased, with the probability of a rate cut in June rising to over 70%, leading to a decline in U.S. Treasury yields and an increase in U.S. stock futures. However, analyzing the breakdown and trends of the CPI data indicates that the market's optimism may be premature

U.S. inflation accelerated in December but met expectations, while core CPI declined, and the market anticipates that the Federal Reserve will continue its rate-cutting pace.

Specifically, the December CPI rose 2.9% year-on-year, matching the expected value of 2.9% and up from the previous value of 2.7%, marking the highest level since July 2024; at the same time, the December core CPI rose 3.2% year-on-year, below the expected 3.3% and the previous value of 3.3%.

Theoretically, core CPI is more indicative of future inflation, so the market reacted positively to this data: the market increased its bets on a rate cut in June.

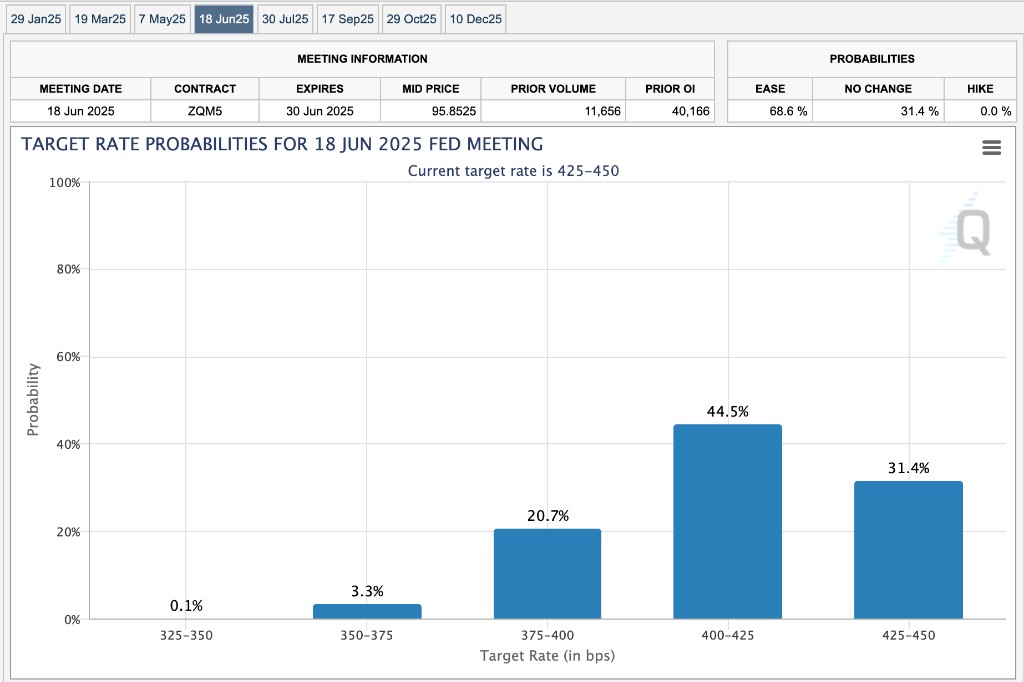

Chart: The probability of a rate cut in June 2025 has risen to over 70%

As a result, U.S. Treasury yields fell, and U.S. stock futures jumped before the market opened: Nasdaq 100 futures surged 2%, and the S&P 500 rose 1.55%.

However, a closer look at the breakdown and trends of the CPI data reveals that the market may be a bit too optimistic