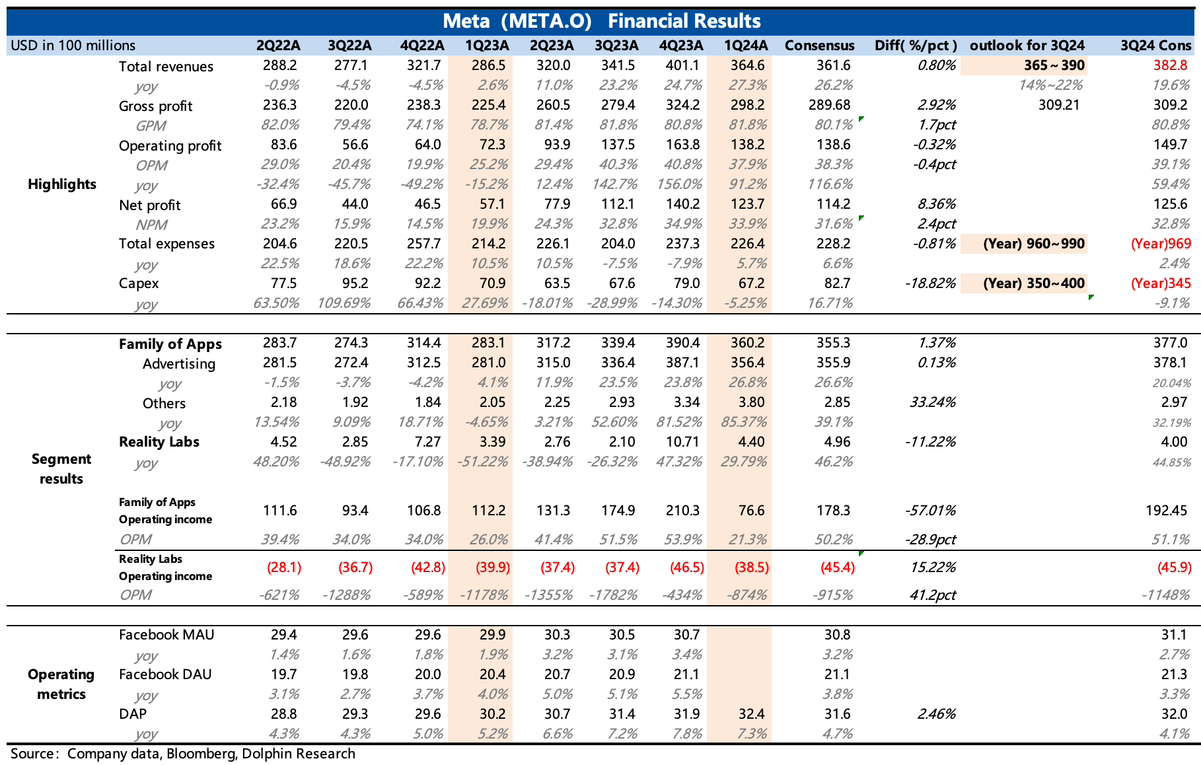

$Meta Platforms(META.US)first take:一季报最大的问题就是 Q2 收入指引(中位数)略低于预期的同时,公司还上调了 2024 全年总支出(从 940-990 亿上调至 960-990 亿)和资本开支(从 300-370 亿上调至 350-400 亿)的指引区间,类似两头压缩利润预期的局面,让人不得不联想到两年前的梦魇。这种” 预期差 “下,直接影响到市场对公司短期内盈利改善趋势的判断,因此在估值并不算低的情况下,股价难免巨震,截至目前,盘后已经下跌 16%。

虽然很难避免全年 eps 和估值的双调整,但结合预期调整后的估值,海豚君认为短期可能存在过度反应。当下和 2022 年下半年开始的至暗时刻相比实际上区别很大,一方面管理层允诺增加的 Opex 和 Capex 都主要用于 AI,而 AI 驱动公司业务增长的逻辑已经能够论证,2025 年也有可能进一步推动收入增长而非继续下调预期。另一方面,上一次最伤逻辑的竞争恶化问题,至少对于目前的 Meta 来说也并不存在。

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.