Morgan Stanley discusses recent "asset allocation": shifting from government bonds to commodities, stocks still lack cost-effectiveness.

本輪美國股債拋售浪潮至 10 月下旬,但在過去兩週強勁反彈。摩根大通認為,這一走勢本質上是技術性的,是由動量策略和空頭回補推動的結果。摩根大通 Marko Kolanovic 分析師團隊在上週公佈的報告中表示,股票的風險回報仍然不具吸引力,由於明年的經濟前景仍不明朗,對股市保留防禦立場: 限制性貨幣政策可能會持續一段時間,股票估值較高,鑑於流動性緩衝減弱、一系列高利率,消費者可能開始緊縮開支,消費貸款產品、貸款標準收緊以及拖欠率上升。

本輪美國股債拋售浪潮至 10 月下旬,但在過去兩週強勁反彈。摩根大通認為,這一走勢本質上是技術性的,是由動量策略和空頭回補推動的結果。

摩根大通 Marko Kolanovic 分析師團隊在上週公佈的報告中表示,股票的風險回報仍然不具吸引力,由於明年的經濟前景仍不明朗,對股市保留防禦立場:

限制性貨幣政策可能會持續一段時間,股票估值較高,鑑於流動性緩衝減弱、一系列高利率,消費者可能開始緊縮開支,消費貸款產品、貸款標準收緊以及拖欠率上升。

這可能會在未來幾個季度對需求造成持續衝擊,削弱企業的定價能力和利潤率,明年每股收益(EPS)增長 12% 的共識預期可能無法達到。

與此同時,考慮到過去一個月油價大幅下跌,地緣政治風險仍然較高,摩根大通對能源更加樂觀。它削減了對國債的配置,將資金轉向大宗商品尤其能源上面。

從國債轉向商品,聚焦能源

摩根大通提出將資金配出從國債轉向商品,主要基於一下幾點考慮:

地緣政治風險仍然較高。

當前俄烏衝突帶來的不確定性依然很大,地緣政治緊張局勢也較難在短期內明朗。這增加了市場的波動性和風險溢價。商品特別是能源類商品的配置可以起到對沖作用。

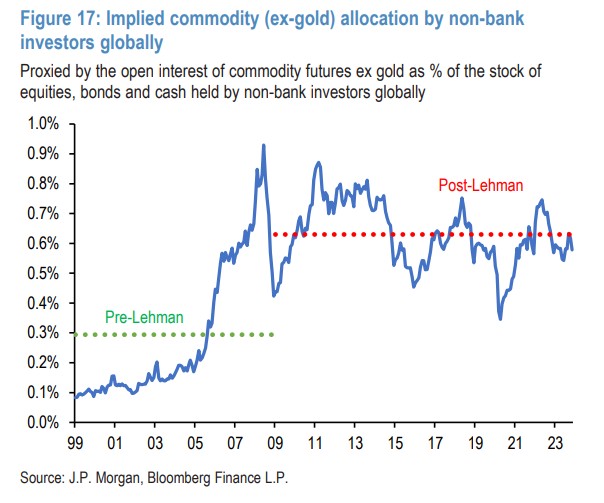

能源領域的持倉較為清淡。

數據顯示,由於過去一年的回調,投資者對商品(除黃金外)特別是能源類商品的持倉已經較為清淡。這意味着目前的減持並不充分,還有進一步增加配置的空間。

國債持倉偏重,需獲利了結。

摩根大通認為,當前國債供給急劇增加,而投資者又持有較重倉位,這意味着國債市場將面臨回調壓力,因此有必要通過獲利了結來減持頭寸。

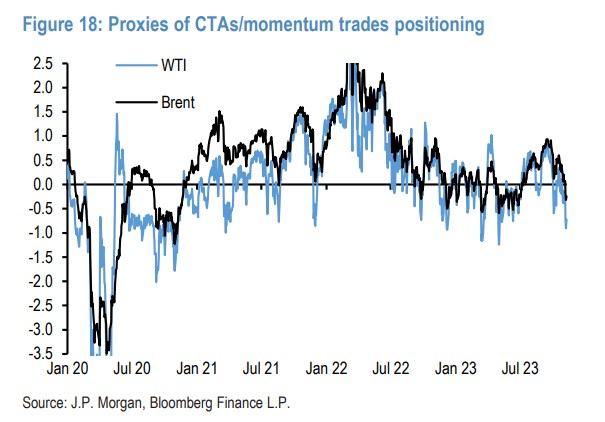

該機構指出,動量交易者的國債空頭倉位基本已平倉。商品交易顧問(CTA)和其他動量型投資者此前極端做空的政府債券頭寸已經基本平倉,這也為轉向商品提供了技術上支持。

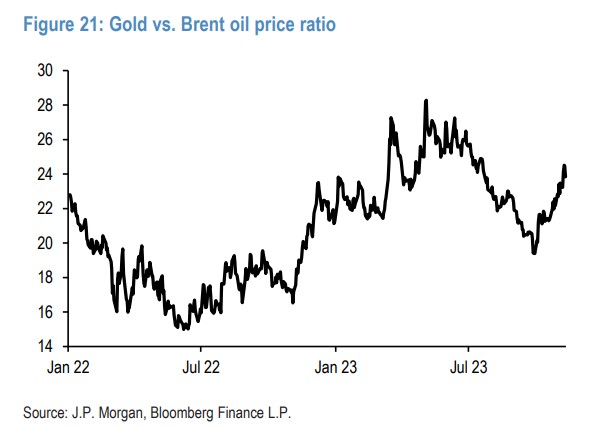

黃金與原油的價比看高。

從黃金與原油的價比上看,原油相對黃金而言仍然較為便宜,支持將資金轉移到原油的配置。

股票依然性價比不高

在股市方面,摩根大通保留防禦立場,而這取決於其對美國明年經濟衰退的預期。

摩根大通指出,近幾個月美國勞動力市場顯示出超乎想象的彈性,而且第三季度 GDP 增長 “異常強勁”,這表明美國經濟衰退的時間可能會從明年年初推遲到年底。

三季度的企業財報也支持了這一觀點。摩根大通在報告中寫道:

在美國和歐洲,大約有 75% 至 85% 的公司已經公佈了第三季度的業績。

在不考慮能源部門的情況下,美國和歐洲 (企業) 的 EPS 分別增長 9% 和 4%。超出預期的盈利表現推動標普 500 指數三季度綜合 EPS 預期值大幅提升。在各個行業中,非必需品、金融和通信服務部門的盈利增長都達到兩位數。

雖然三季度財報表現較為積極,但分析師對未來 12 個月的 EPS 預測主要是下調的。

經濟的韌性為美聯儲的緊縮政策帶來更多不確定性。華爾街見聞此前文章提及,為了進一步瞭解美國的經濟狀況,美聯儲已經開始了實地調研,通過企業管理人員和消費者反饋的坊間數據,更直觀的瞭解經濟形勢。

而且,美聯儲最新的會議記要顯示,聯儲決策者再次集體認為適合一段時間保持高利率,重申將謹慎行事,並沒有流露結束加息週期的意願。

美債漲勢正在削弱

過去幾周,美債市場得到一定的緩解,10 年期美債收益率下降超過 40 個基點。但是 30 年期美債拍賣情況不佳,這表明,美債仍面臨需求結構變化、供應過剩的窘境。

即使發行定息債券量沒有預期的那麼多,但今年淨髮行美債規模仍將從大約 4500 億美元仍驟增至 1.3 萬億美元。

美聯儲的預期也轉為更鴿派,中期預計將進行 20 多個基點的降息。此外,實質貨幣 (real money) 投資者的(美債)持倉整體仍比較長。

這意味着過去幾周美債收益率可能沒有太多上漲的空間,摩根大通尤其不看好 7 年期美債。同時,由於供給增加和需求結構變化,遠期溢價進一步走高的壓力將持續存在,預計收益率曲線進一步陡峭,因此,摩根大通更看好 10 年期與 30 年期之間的基差看漲倉位。

新興市場:股市更樂觀

美國勞動力市場數據疲軟、工資數據通縮傾向減輕,新興市場經濟放緩但沒有崩潰,對新興市場部分資產形成了支撐。

摩根大通仍維持對新興市場股票的看漲,預計其有望受益於增長前景的改善、低倉位和相對便宜的估值。

摩根大通表示:

一些新興市場央行採取了風險管理的策略,實施的寬鬆政策較少,甚至有出乎意料的升息,主要是因為高油價和匯率貶值引發對通脹的擔憂。隨着其中一些風險逐漸減輕,央行有更多的靈活性,投資者對它們對風險的警惕感到安心。

由於美債收益率前景不太樂觀,且新興市場央行的寬鬆政策相對較少,摩根大通對於新興市場債市持謹慎態度。

歐元區:中期債市相對樂觀

歐元區方面,上週經濟數據延續弱勢基調,通脹放緩的速度和採購經理人指數(PMI)數據低於預期,三季度 GDP 數據顯示歐元區經濟適度收縮。

即使如此,摩根大通仍認為歐洲將避免衰退,經濟增長將恢復至 1% 的水平。

摩根大通對歐元區債券保持中期看漲觀點,持有德國 5 年期國債,但同時也持有歐元利率互換曲線上的 10 年期和 30 年期部分的陡峭部分,這意味着摩根大通預計長期利率較短期利率有所上升。

而對於股市,摩根大通維持謹慎態度,股市的風險回報仍然不具吸引力,不建議追高最近的反彈。