Amidst the sharp increase in difficulty in stock selection in the US stock market, Goldman Sachs has put forward two "wealth codes"

美股選股難度增加,高盛提出兩個 “致富密碼”。高盛策略師認為,美債收益率上升、股市估值高企以及美國政府赤字擔憂將影響美國股市的漲幅。高盛預計,美股基準指數不太可能繼續上漲,並重申對標普 500 指數年底 5200 點的目標預測。高盛經濟學家預測美國今年實際 GDP 增長率約為 3%。高盛建議投資者在平緩市場環境中採取多元化分散投資策略。高盛股票分析師給出的兩項個股建議為 “強力買入”。

如果華爾街大行高盛對後市的預期準確的話,短期內選股將變得更加困難。高盛知名策略師奧本海默 (Peter Oppenheimer) 認為,10 年期美債收益率步入上行趨勢、股票市場估值高企以及美國政府高額赤字可持續性的擔憂加劇共同作用之下,將收緊美國股市的整體漲幅。

高盛 5 月份發佈的一份研報顯示,隨着美聯儲降息預期從年初的一度 150 個基點降息預期大幅下降至僅降息 25 個基點,高盛策略團隊預計從現在到今年年底,美股基準指數——標普 500 指數不太可能繼續上漲。高盛重申該機構對標普 500 指數年底 5200 點的目標預測,同時指出 “從現在到今年年底,回報率大致持平”,除非美聯儲比市場目前預期更加積極地下調利率。

高盛經濟學家預計,美國今年的實際 GDP 增長率將在 3% 左右;高盛股票策略團隊則預計,2024 年標普 500 指數的盈利增長率將達到 8%,同時強調,目前美國股市估值已經處於歷史高位。

“在我們看來,如果美債收益率上升得越快,對美股的負面影響就越大,” 高盛策略師奧本海默表示,並補充道:“考慮到股市的估值,這將是一個減速帶。”

不過,儘管美股有可能轉為橫向波動或者趨於向下調整,但仍有前進的道路。奧本海默指出:“多元化分散投資是投資者們在平緩的市場環境中擁有的機會。”

多元化分散投資是一種更謹慎的投資組合管理策略,並且在基準指數面臨上行壓力之際 “自下而上” 的分散化選股邏輯更加適合投資者們。奧本海默在高盛的股票分析團隊的同事們正以 “自下而上” 的選股邏輯選擇他們認為有穩定上漲潛力的股票。

TipRanks 數據庫中顯示出高盛股票分析師們最近給出的兩項個股建議,看起來華爾街大行們與高盛的觀點是一致的——分析師一致將這兩隻熱門個股評級為 “強力買入”。

爵士製藥 (JAZZ.US)

對於生物科技公司來説,讓一種藥物獲得監管正式批准並上市就像是找到了聖盃——而總部位於愛爾蘭的爵士製藥公司在神經科學和腫瘤學領域都有大量此類獲批產品。這些商業化的藥物確保了爵士製藥的強勁基本面,即使它也保持着廣泛的新藥研究項目的相關高額支出,同時該公司還能保持季度利潤基本穩定。

從投資者的角度來看,這家生物科技公司提供了幾乎 “兩全其美” 的生物科技局面,既有穩定的營收規模和銷售額記錄,又有前景頗高的臨牀試驗候選藥物潛力。

在該公司現有和已批准的藥物中,有三種藥物被該公司評級為今年第一季度的 “關鍵增長動力”。這三款藥物的總營收同比增長了 12%;其中兩個來自爵士製藥的神經科學產品組合,第三個來自腫瘤學領域。從增長最低到最高,三個主要的營收來源分別是 Epidiolex(一種用於治療癲癇發作的大麻二酚),產品淨銷售額同比增長 5%;Xywav 是一種用於治療白天過度嗜睡的藥物,產品淨銷售額增長 14%;以及治療急性淋巴細胞白血病的腫瘤學藥物 Rylaze,其產品淨銷售額增長約 20%。

轉向研發管道,該公司的候選藥物之一 zanidatamab 是多個臨牀試驗研究的主題。這些研究將 zanidatamab 作為一種單一療法和聯合療法,計劃用於治療多種癌症。在這些研究中,其中的一項研究是 zanidatamab 治療 HER2 陽性膽道癌的試驗。該公司於 6 月 1 日發佈了 zanidatamab 治療先前治療的、不可切除的、局部晚期或轉移性 HER2 陽性膽道癌的 2b 期臨牀試驗的陽性數據;數據顯示,zanidatamab“表現出持續和持久的抗腫瘤反應”。

就在該數據發佈的前幾天,爵士製藥宣佈 FDA 已經批准了 zanidatamab 在先前治療過的、不可切除的、局部晚期或轉移性 HER2 陽性膽道癌症適應症的 BLA(生物製品許可申請) 優先審查。PDUFA 審查日期則定於 2024 年 11 月 29 日。

此外,爵士製藥於 6 月初在聯合專業睡眠協會第 38 屆年會上發表演講。這些演講強調了 Xywav 的安全性和有效性,Xywav 是該公司批准的對抗白天過度嗜睡的重磅藥物。

對高盛分析師 Andrea Tan 來説,這家公司的部分吸引力在於研發管道的高質量。她在談到該股時寫道:“雖然關於睡眠業務 (以及 Epidiolex,在某種程度上) 的前景一直存在爭議,但我們對支持長期業績增長前景的新興管道持樂觀態度……在研發和早期研發管道方面的持續投資以及業務發展 (如果爵士製藥要槓桿率達到 5 倍的基於 2024 年 EBITDA,則其資產負債表增量容量將要達到約 80 億美元) 將成為增長的來源。” 由於爵士製藥的股指相對於標普 500 指數的 5 年平均水平有更高的折讓,我們認為 J 該股目前的水平具有吸引力。”

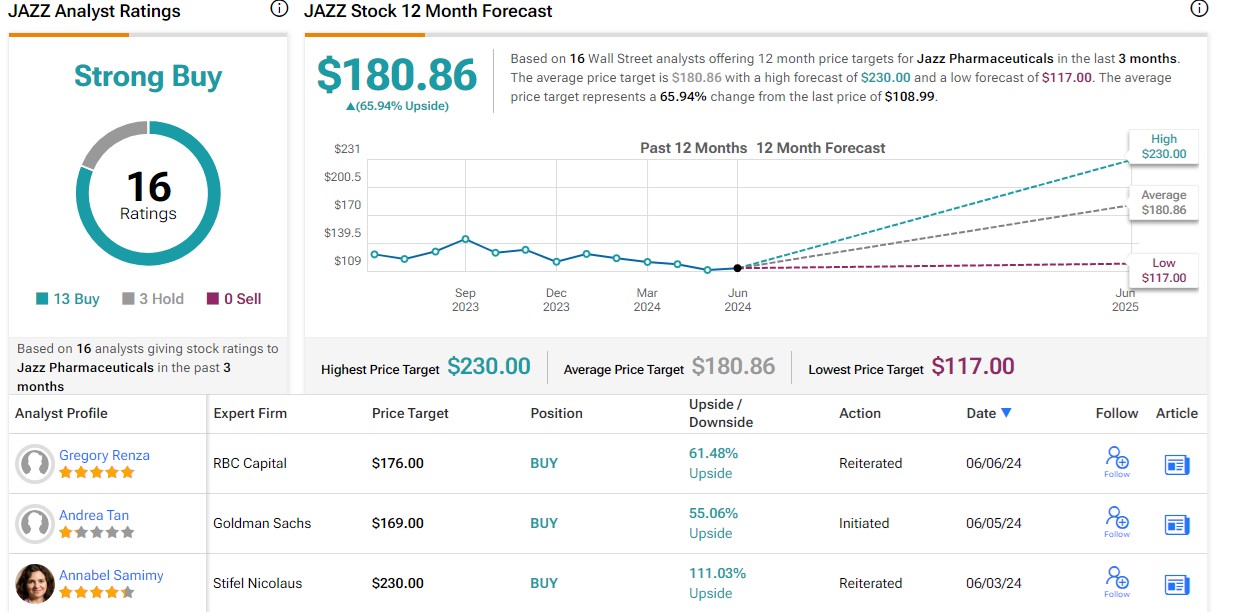

高盛分析師 Andrea Tan 給出 “買入” 評級和高達 169 美元的目標價,這意味着該股一年內將有高達 55% 的強勁上漲潛力。

華爾街分析師們對於爵士製藥的 “強烈買入” 一致評級是基於 16 篇評論,其中包括 13 篇 “買入” 評級研報,3 篇 “持有”,該股 180.86 美元的平均目標價甚至比高盛的觀點更為樂觀,這表明該股在週一收盤價 108.99 美元的基礎上還有 66% 的潛在上漲空間。

極氪 (ZK.US)

高盛支持的股票榜單上的下一隻重要股票是中國汽車巨頭吉利 (Geely) 部分擁有的電動汽車品牌極氪。極氪是一個豪華電動汽車品牌,專注於將歐洲汽車風格和性能與最新的先進生產和製造工藝相結合。該公司的車型包括 Zeekr 001,一款五座掀背跨界車和 Zeekr X,一款豪華城市 SUV。此外,該公司還推出了一款 6 座 MPV Zeekr 009,並正在研發一款高檔豪華轎車。該公司的汽車定位於純電池電動汽車,同時具備高端軟件和硬件應用程序,以增強駕駛體驗。

今年 5 月,極氪正式登陸美股,並且公佈了一份強勁的季度業績報告。本月初,Zeekr 宣佈了 2024 年 5 月的交付數據,並顯示出強勁的同比增長。今年一季度,極氪共交付 33059 台,同比增長 117%,實現營收 147.37 億元,同比增長 71%;整車毛利率達 14%,同比提升 3.9 個百分點。

1-5 月,極氪共交付 67764 台,同比增長 112%,穩居 2024 年 20 萬以上中國純電品牌銷量冠軍。其中,5 月交付 18616 台,同比大增 115%,創單月交付歷史新高。

這家中國電動汽車製造商引起了高盛電動汽車行業分析師 Tina Hou 的注意。在談到新上市的股票時,她指出了極氪的一些明顯優勢,然後給出了她的長期展望前景:“我們相信,通過採用輕資產製造模式,利用其母公司 (吉利) 的工廠產能,極氪在競爭中處於更有利的地位,這有助於減輕沉重的前期資本支出負擔。吉利成熟的供應鏈也使極氪在成本上具有優勢,極氪的汽車貢獻利潤率更高,達到 18.2%(蔚來汽車和小鵬汽車的貢獻率分別為 16.2% 和 3.7%)。此外,極氪在 2023 年擁有 30 億元人民幣的淨現金和 23 億元人民幣的經營現金流。”

對 Tina Hou 來説,這是一隻現在值得買入的股票。該分析師給極氪的初步評級為 “買入”,目標價高達 34 美元,意味着一年內的潛在漲幅高達 44%。

整體來看,華爾街分析師們對這隻新上市美股的一致評級為 “強力買入”,基於 3 個 “買入” 評級的研究報告。截至週一美股收盤,該股收於 23.66 美元,34.67 美元的華爾街平均目標價意味着未來一年的潛在漲幅高達 46.5%。