The competition in the mainstream new energy market has reached a critical turning point

In August, the competition in the new energy vehicle market intensified, with BYD's sales exceeding 370,000 vehicles, continuing to lead the market. However, brands like Leapmotor and HiPhi made breakthroughs in BYD's strong areas, indicating a change in the market landscape. Although BYD remains far ahead in overall sales, other brands are starting to challenge its position in the mainstream household vehicle market below 200,000 RMB. In the mid-to-high-end market segment, sales of BYD's sub-brands still lag behind, while competitors such as ZEEKR and Nio are gradually emerging

autocarweekly (ID: autocarweekly), Author: Luo Ji, Cover image from: AI Generated

In August, the new energy vehicle market showed the dominance of BYD, but brands like Leapmotor and Galaxy began to break through.

• 🚗 BYD's sales in August exceeded 370,000 vehicles, continuing to lead the market.

• 🌟 Leapmotor, Galaxy, and other brands made breakthroughs in BYD's strong areas.

• 🎯 Several differentiated models helped some brands establish a foothold and challenge BYD.

In the just-passed August, the penetration rate of new energy vehicles in the domestic market exceeded 55%. At the same time, BYD's sales reached a new high, exceeding 370,000 vehicles in August. Whether it is the expansion of the new energy market or BYD's growth, it seems very stable, with no key turning points in the short term.

However, looking closely at the detailed sales data for August, signs of change have emerged in the new energy market, especially in the mainstream household vehicle market within 200,000 RMB. While everyone is predicting when BYD will break through the 400,000 mark, its dominance in the new energy field can also bring about different sparks.

What new secret weapons are hidden in the detailed data

At the enterprise level, whether in the overall market or the new energy market, BYD's sales volume is significantly ahead. The second-ranked Volkswagen brand, with the combined monthly sales of North and South Volkswagen last year totaling over 200,000 vehicles, has now dropped to around 150,000 vehicles. BYD's sales alone exceed the sum of North and South Volkswagen, and North and South Toyota.

In the camp of independent brands, it is basically necessary to combine five or six car companies such as Geely, Changan, Great Wall, and Chery to match the scale of BYD alone. Reminiscent of the slogans from previous years, today's BYD does indeed have the momentum of "Qin sweeping the six states, Tang battling the barbarians".

Looking at the macro numbers, it seems that other manufacturers have no chance to compete with BYD in its dominance in the new energy field. However, looking at the detailed data, everyone actually has quite a few secret weapons.

Firstly, in the mid-to-high-end market above 200,000 RMB, BYD's main brand has almost no models priced above 200,000 RMB, and its sub-brands such as Tang and Song Pro currently have limited sales, which combined are still not comparable to ZEEKR and Nio Of course, FANGCHENGBAO has adjusted its pricing positioning, and Tengshi will also launch the heavyweight Z9 series. The performance of the two brands in the high-end market may see a breakthrough, but in the short term, BYD is still struggling to rank among the top tier in the market above 200,000 yuan.

Looking at BYD's absolute dominance in the mainstream market.

In the low-price market below 100,000 yuan, the Seagull with a monthly sales volume of around 30,000 units still has Wuling Rongguo as a strong competitor. In the price range of 100,000 to 200,000 yuan, whether it's pure electric vehicles like Yuan PLUS, Yuan UP, and Dolphin, or PHEV models like Qin L and Song PLUS, they are basically unbeatable in the household car market (with the exception of Ai'an, which is mainly driven by ride-hailing demand).

PHEV models such as Geely's Yinhe L6, L7, and Shenlan S7, with monthly sales volumes of around five to six thousand units each, are performing well. At the same time, there are LEAPMOTOR C10 and C16 with pure electric and extended-range power, each with monthly sales that are also difficult to exceed 7,000 units. When these models are combined, they are roughly equivalent to the sales volume of just one Song PLUS model, while BYD has at least 5 models with stable monthly sales of over 20,000 units in the price range of 100,000 to 200,000 yuan.

If the automobile market becomes a battlefield, facing a Super Power like BYD, other car companies may not even have the courage to unite to resist. Fortunately, this is a marketplace, and companies in a weak position still have the possibility of breakthroughs. And in the just past August, this sign has already emerged.

LEAPMOTOR, Yinhe, Shenlan, August sales surge

The first breakthrough came from LEAPMOTOR.

With the bulk delivery of the C16, LEAPMOTOR's sales in August this year increased significantly month-on-month, breaking the 30,000 unit mark for the first time. Regardless of the market or LEAPMOTOR itself, this phenomenon is first seen as the third new force brand to break the 30,000 unit mark in sales after Li Auto and Aito, completely pulling away from Nio and XPeng.

For me, the true significance of LEAPMOTOR breaking the 30,000 unit mark in monthly sales is not about being the third new force. After all, the selling prices of almost all LEAPMOTOR products are below 200,000 yuan, making them incomparable to Aito and Li Auto, and the price difference with Nio and XPeng is also very large. Apart from being in the new force camp, LEAPMOTOR has no real comparability with "Nio-Xiaopeng-Li-Aito" and brands like ZEEKR and Xiaomi.

I am not trying to deny the significance of LEAPMOTOR breaking the 30,000 unit mark. On the contrary, from a different perspective, it can be seen that LEAPMOTOR's monthly sales of 30,000 units within 200,000 yuan may be more critical than breaking through above 200,000 yuan, because these more than 30,000 units of sales are all within BYD's strongest price range In other words, LEAPMOTOR has achieved a breakthrough under the almost all-round encirclement of BYD.

According to LEAPMOTOR's data, in August of this year, the delivery volume of C16 exceeded 8,000 units. Although it is still only a small fraction of the same-priced Song PLUS series, the differences between LEAPMOTOR C16 and C10 are essentially only in the length of the car and the layout of the seats. They are closely priced, with highly similar product styles and positioning. In fact, they can be seen as two versions of the same model. In this way, LEAPMOTOR has a popular model in the price range of 130,000 to 180,000 yuan, with a monthly sales volume of around 15,000 units.

Just as mentioned above, in the most stable 100,000 to 200,000 yuan household market where BYD is based, there were basically no competitors with monthly sales reaching five digits before. Of course, considering C10 and C16 as one car may be a bit far-fetched, but in the same month, there was another indisputable new hit model - the Geely Galaxy E5.

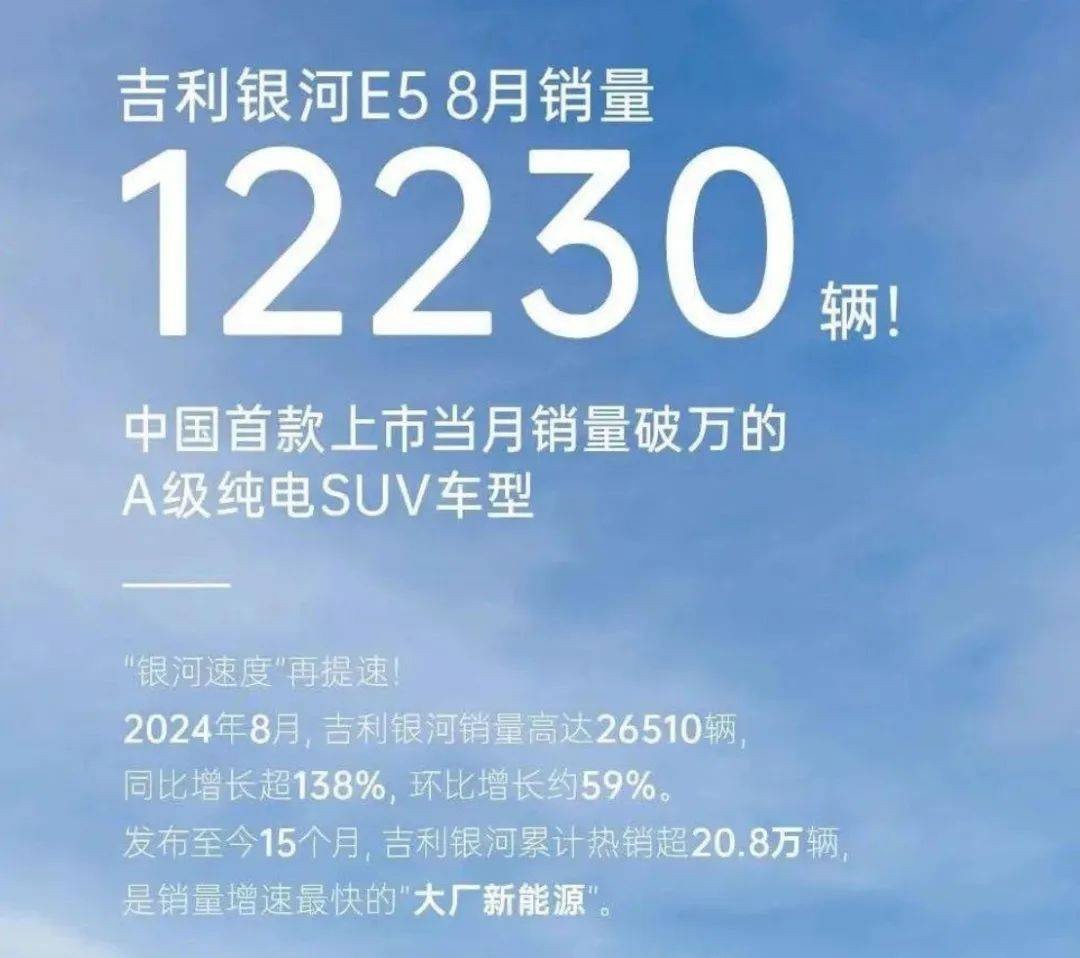

According to the manufacturer's data, the Galaxy E5, which was launched on August 3rd, achieved a sales volume of 12,000 units in its first month. The official slogan directly states: "The first A-class pure electric SUV model with sales exceeding ten thousand in the first month of listing", the prefix may be a bit long, but its significance is indeed significant.

For the Galaxy brand, the E5 has just been launched and has taken on half of the brand's monthly sales, allowing the Galaxy brand to soar from less than 15,000 units in July to 26,500 units directly on a month-on-month basis. Prior to this, the best monthly sales performance of Geely Galaxy was also hovering around 15,000 units.

For the market, as a compact pure electric SUV, the Galaxy E5, which focuses on the price range of 100,000 to 150,000 yuan, is the only pure electric SUV with monthly sales exceeding ten thousand in this price range, besides the slightly ambiguous body-shaped Aiways Y. The only pure electric SUVs with monthly sales exceeding ten thousand are the Yuan PLUS, Yuan UP, and Song PLUS EV. The rest, including the LEAPMOTOR C10 and C11 pure electric versions, have monthly sales of less than 5,000 units on average, creating a huge gap between them and BYD.

The emergence of the Galaxy E5 has bridged this seemingly insurmountable gap, with sales of 12,000 units in August already on par with the Song PLUS EV. Although there is still a multiple gap compared to the closest-priced Yuan PLUS, it has ultimately allowed other car companies to see the possibility of approaching, or even challenging, BYD in the mainstream price range In addition, Deep Blue, which has always been very similar to Galaxy in terms of sales volume, main selling price, also achieved a breakthrough in August. The monthly sales volume, which used to be less than 15,000 units, directly exceeded 20,000 units, mainly due to the renaming and listing of Deep Blue S07, which made up for the shortcomings in the product, and the achievements brought by price reduction and increased configuration.

Lastly, there is the XPeng MONA M03, which has not yet released data but has already shown the momentum of a hit product. This new car, which was just launched at the end of August, received 30,000 pre-orders in two days. XPeng has set a quarterly sales target of 41,000 to 45,000 units, equivalent to a monthly sales volume of nearly 15,000 units.

Whether this target can be achieved remains to be seen. But according to current market feedback, MONA M03 is likely to become a new pure electric sedan priced between 100,000 to 150,000 yuan with monthly sales exceeding 10,000 units. For comparison, BYD's Qin PLUS EV sold 17,000 units in July. If MONA M03 can reach around 15,000 units, it will basically be on par with BYD's best-selling sedan.

Do not simply benchmark based on price and configuration, it is better to establish a style and features.

The total sales volume of the four brands mentioned above, LEAPMOTOR, Galaxy, Deep Blue, and XPeng, in August will reach 100,000 units, which is only equivalent to the scale of one series of BYD Qin (Qin PLUS DM-i/EV, Qin L). Faced with the scale of over 300,000 units of the BYD brand, it seems insignificant, let alone posing a threat to BYD.

However, monthly sales volume is static. Looking at the dynamic trend, there are signs of a key turning point in the competitive situation of the mainstream new energy vehicle market.

The breakthrough of brands like LEAPMOTOR, Galaxy, Deep Blue, and XPeng came after the basic completion of the new launches or iterations of BYD's core models (Qin L, Song PLUS, Dolphin 06, Dolphin 07, Yuan UP, Song L DM-i, etc.). Currently, BYD is at an unprecedented peak in terms of both sales volume and product strength.

In other words, these brands have achieved breakthroughs under the eyes of BYD's strongest and most complete lineup to date. Although there is still an exponential gap in terms of sales volume, they have all secured their own "stronghold" based on their abilities. Once they establish a foothold, there is an opportunity for the "stronghold" to develop and grow.

Looking at the products, we will find that the breakthrough models achieved their success not by benchmarking against BYD based on low prices and configurations, but by each having their own style and characteristics.

On a price basis with sufficient sincerity, LEAPMOTOR C10, C16 follows the "dad car" route, MONA M03 follows the route of large space and intelligence, and Galaxy E5 is a global model that does not deliberately pursue large size. Their significant product positioning differentiation has also become the key to their breakthroughs Summary

From the perspective of national unity, Geely, Leapmotor, and BYD are not in opposition. The common goal of independent brands is to seize more market share from joint venture brands. However, from the perspective of the automotive industry, BYD's impact and threat to other independent manufacturers is no less than that of joint venture brands.

Recently, the confrontation between senior executives of automotive companies regarding internal competition has essentially exposed the contradictions at the industry level. For a long time in the future, how to combat BYD and how to achieve their own development will be a highly overlapping top priority.

As consumers, there is no need to overly involve personal positions and emotions. Regardless of how the future unfolds, as long as competition among automotive companies can bring about more cost-effective products, it will always be a good thing.

autocarweekly (ID: autocarweekly), Author: Luo Ji