Tencent Music: A small and beautiful entity hidden by the shadow of live streaming

After the Hong Kong stock market closed on November 14th, Tencent Music (TME) released its Q3 2023 earnings report. Despite the "shocking" decline in revenue (double-digit decrease), there were still some "small joys" (continuing improvement in gross profit margin, overall slightly exceeding expectations) amidst the anticipated impact of the live streaming adjustment.

Let's take a closer look at the key information:

Expected decline in revenue: Last quarter's revenue growth barely stayed positive due to a low base, but Q3 officially entered negative growth. However, with the market already anticipating the impact of the live streaming adjustment, the actual performance was slightly better than expected.

Continued increase in music subscription: Online music revenue grew slightly slower due to a high base, but still reached 32.7%. With the increase in average payment per user, the number of paying users and the payment rate have also reached 17%, approaching the penetration rate of long videos.

As the saying goes, the sustained high growth of music subscriptions, which is the essence of the business, can be attributed to Tencent Music's solid foundation. At least in the digital music market, its monopoly advantage has not been significantly affected by existing competitors. Of course, ByteDance, with its strong traffic, still needs to be closely watched. Recently, there haven't been many actions from ByteDance, which has given Tencent Music time for internal adjustments.

Less impact from live streaming than expected: Tencent Music is determined to adjust its live streaming business and has made its attitude clear since last quarter. Music subscription revenue will soon surpass social entertainment, completely transforming the previous business model of "music on the surface, relying on live streaming in reality." In Q3, revenue from live streaming and other social entertainment businesses decreased by 49% YoY, which may seem alarming, but the market had already anticipated this. Moreover, Q3 showed a trend of improvement month by month, indicating that the negative impact has reached its bottom.

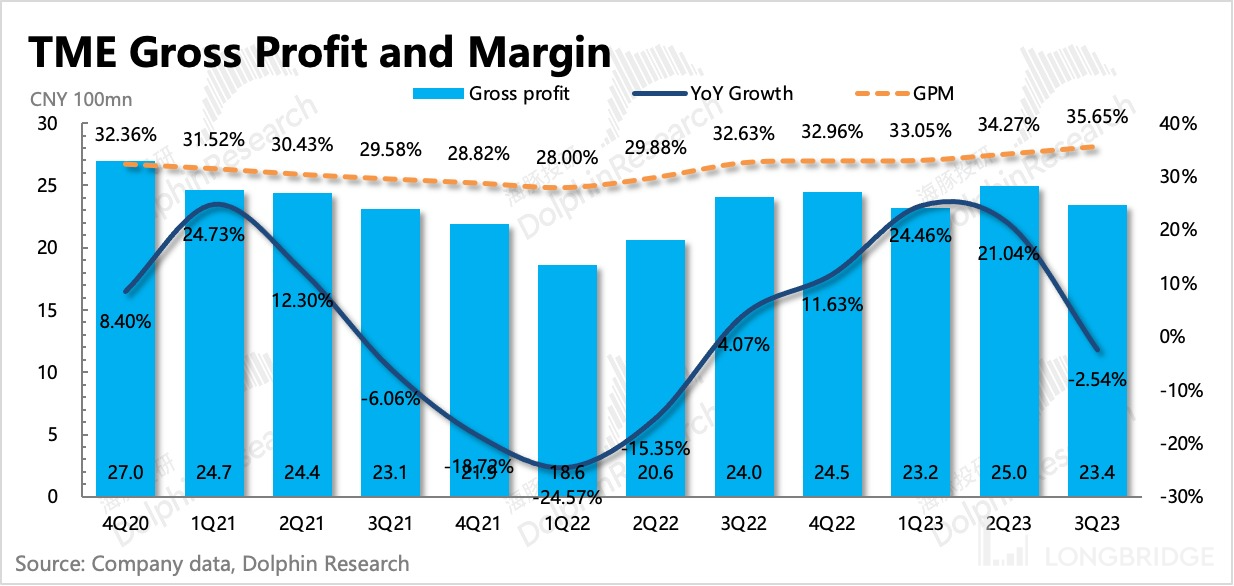

Continued improvement in gross profit margin: In the past, Tencent Music was believed to make money mainly from live streaming and karaoke businesses, as the subscription model alone was unable to cover the high copyright costs. However, since the exclusive copyright unbundling and the signing of new copyright cooperation agreements, the cost of high-quality copyrights, which were in high demand, naturally decreased. Additionally, unlike the concentrated music copyright market in Europe and the United States, Tencent Music, with its traffic advantage, also has relative bargaining power.

In this situation, with the growth of subscription and advertising revenue, the gross profit margin of online music is higher than that of live streaming, which has a more than 50% revenue sharing model. This has led to a continuous improvement in the group's gross profit margin. By Q3, Tencent Music's gross profit margin had exceeded 35%, approaching the medium to long-term target of 35-40%.

Share repurchase: The share repurchase plan announced earlier this year finally changed its stingy approach in Q3 and repurchased approximately 15.8 million American depositary shares for approximately $103 million during the market panic period, at an average price of $6.5 per share.

Detailed financial data in the earnings report:

Dolphin Research's Perspective

Although Tencent Music's third-quarter revenue continues to reflect the impact of live broadcast adjustments, the company has revealed that the negative impact has been slowing down month by month. Therefore, it can be expected that the absolute impact has already reached its lowest point. Of course, in terms of the relative impact on year-on-year growth rate, the numbers may still not look good in the first half of next year.

However, after gradually reducing its reliance on live broadcasts and focusing on music, Tencent Music still relies on the scale advantage of its music assets (having more bargaining power due to copyright dispersion) and the traffic support from Tencent's ecosystem. It has successfully approached its long-term target gross profit margin of 35% to 40%. Although it does not have live broadcasts as a business growth driver for now, it can still become a small and beautiful presence through optimizing its business model.

In terms of valuation, the improvement in profit margin can partially help alleviate the impact of declining revenue. However, there will also be some pressure on growth next year due to the high base. Therefore, based on this year's normal adj. net profit, a PE ratio of 12-15x is given, plus a net cash of 16.5 billion RMB (2.3 billion USD). The valuation range is between 12-14 billion RMB (slightly higher upper limit compared to the previous quarter). Currently, the market value is 12.8 billion RMB, and there is no particularly obvious undervaluation space for now.

Below is a detailed analysis:

1. Stable Traffic Pool Ecosystem

In the third quarter, Tencent Music's online music traffic pool remained relatively stable, with the number of monthly active users unchanged. The impact of live broadcast adjustments began in early June, so the impact on users mainly manifested in the third quarter, with the number of live broadcast users declining to 129 million, a decrease of 700,000 compared to the previous quarter.

2. Live Broadcast Revenue Halved

Although the live broadcast adjustment only started in early June, the direct decline of 20% in social entertainment revenue in the second quarter is already a clear indication of its influence. Therefore, for the third quarter, which has been negatively affected throughout the entire quarter, the year-on-year decline is naturally not good.

In the third quarter, social entertainment revenue was halved, directly decreasing by 49% to only 2 billion RMB. However, the company has also revealed in previous communications that the negative impact is improving month by month, according to the total revenue guidance from the previous quarter. Therefore, we expect that the decline in the fourth quarter will relatively converge.

Fortunately, such negative impact has been anticipated, and the current market is more willing to bet on the continuous improvement of the business model that encourages music payment.

Under the adjustment of the live broadcast business, the ARPPU (average revenue per paying user) of social entertainment continues to plummet, now only half of what it used to be, at 86.2 RMB per month. However, with the increase in payment points and the improvement of user stickiness, the number of paying users is increasing.

3. Is the value of music subscriptions unlimited?

Due to the pressure brought by the avalanche of social entertainment, companies are to some extent prompted to continue accelerating the growth potential of digital music payments through the paywall strategy.

However, at the same time, the growth performance of digital album sales in other online music revenues has lagged behind due to the high base pressure brought by Jay Chou's new album last year. Meanwhile, we expect that the advertising revenue in other online music revenues should not be bad.

Overall, online music revenue in the third quarter grew by 32.7%, reaching 4.55 billion yuan.

Taking a closer look, among them:

(1)Subscription revenue increased by 41% year-on-year, and with the increase in both quantity and price, it continues to accelerate expansion. Among them, the number of paid users (+21% YoY) and the average payment amount per user (+17% YoY) have increased more compared to the previous quarter.

According to the latest data from Sensor Tower in October, Tencent Music's subscription revenue seems to be continuing to accelerate.

(2)Other online music services, including digital copyright sales and advertising revenue, saw a year-on-year decline of 3.7%. Dolphin Research speculates that this is mainly due to the high base impact brought by the sale of digital albums (Jay Chou's new album) and the advertising business (the release of the epidemic and the increase in loading rates).

4. Improvement in gross profit margin, breaking the bias of the business model

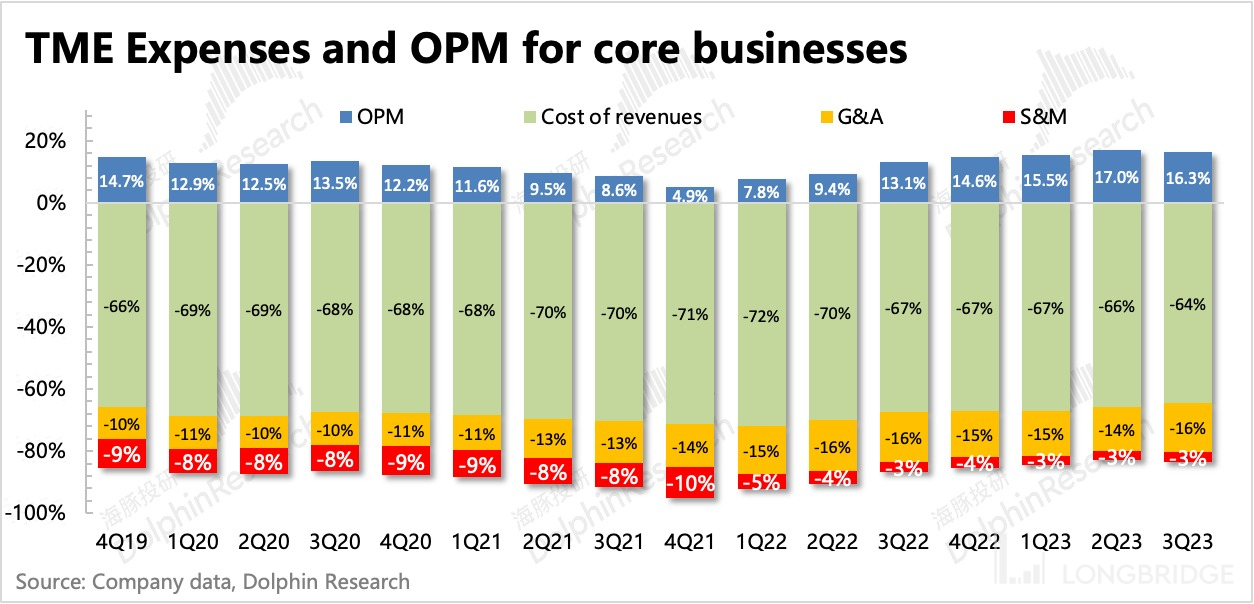

The adjustment of live broadcasting in the third quarter has brought a huge gap to the revenue side, and it still dragged down the overall revenue growth despite the increase in music payment increment. Although copyright costs are still being optimized, and extreme cost control continues (sales expenses decreased by 10% YoY, and management expenses decreased by 12% YoY), in the third quarter, without the low base dividend, the impact of live broadcasting on the profit side was finally exposed—the growth rate has rapidly declined compared to the previous quarter. However, despite a 10% decline in revenue, it is not easy to maintain a positive growth of 11% in operating profit. The gross profit margin has already crossed the threshold of 35% and is approaching the company's long-term target of 35-40%.

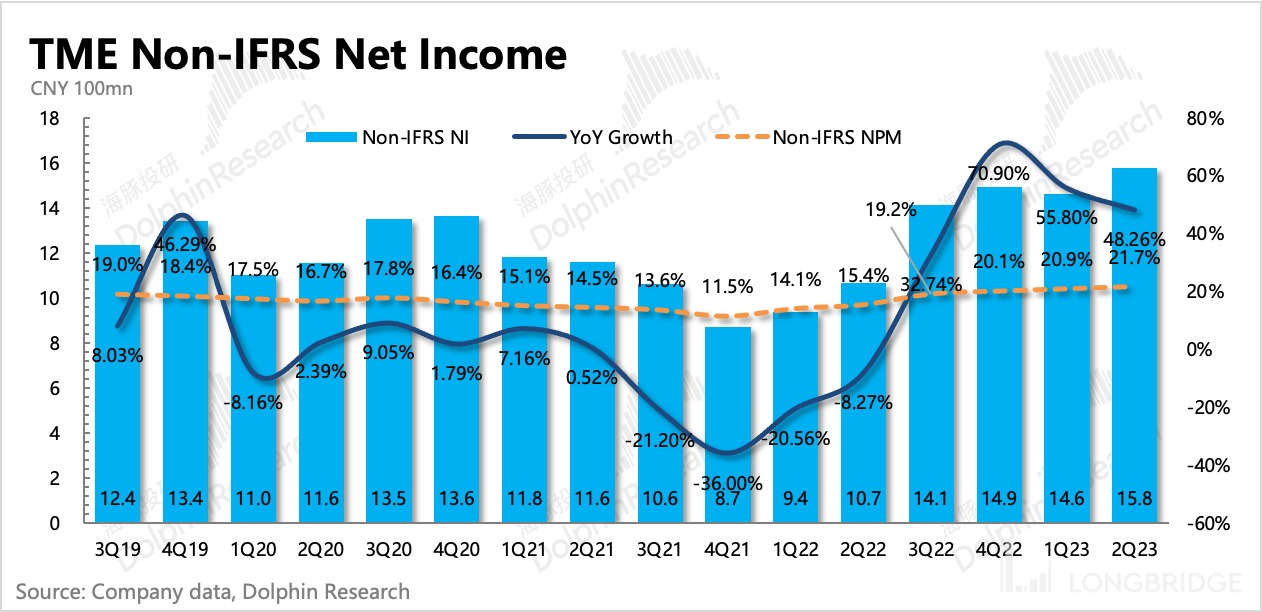

Excluding the impact of equity incentives and non-operating income, Tencent Music achieved a non-IFRS net profit of 1.503 billion in the third quarter, a year-on-year increase of 6.5%. The difference in growth rate compared to operating profit indicates the driving force of cost reduction and efficiency improvement (reduction in SBC).

In the past year, Dolphin Research has conducted several studies on Tencent Music:

- Earnings Season:

- August 15, 2023: Conference Call - "Stabilizing after Live Broadcasting Adjustments (2Q23 Conference Call Summary)"

- August 15, 2023: Earnings Review - "Business Adjustments, Continued Bottoming Out"

- March 22, 2023: Conference Call - "No Hard Damage in Performance Guidance, Just Overly Sufficient Expectations (4Q22 Conference Call Summary)"

- March 21, 2023: Earnings Review - "No More Growth, Can Cost Cutting Support the Music Dream?"

- November 16, 2022: Conference Call - "Tencent Music: Open Source and Streamline, Profitability Will Increase Next Year (3Q22 Conference Call Summary)"

- November 15, 2022: Earnings Review - "Tencent Music: 'Purifying' Users, Squeezing Out Profits, Focusing on Money"

Image 1 Image 2 Image 3 August 16, 2022 Phone Conference: Tencent Music: Enriching member privileges, continuing to promote incentive advertising (Phone Conference Summary)

{kind=link}

{kind=link}

{kind=link}

August 16, 2022 Earnings Report Review: Tencent Music: Easing performance decline, but early signs of recovery (Earnings Report Review)

May 17, 2022 Phone Conference: New live streaming regulations will be evident throughout the year, cost reduction and efficiency improvement are one of this year's top priorities (Tencent Music Phone Conference)

May 17, 2022 Earnings Report Review: Tencent Music: It's still early spring, with an abundance of resources (Earnings Report Review)

In-depth

April 12, 2023: Douyin and Tencent's alliance outside the venue, is there a solution to the deadlock in entertainment payment? (Invite code: invite-code=)》)

January 6, 2023: Pan-entertainment "New Year's Kickoff", whose rebound is more sustainable, Tencent or Bilibili? (Invite code: invite-code=)》)

Risk disclosure and statement for this article: Dolphin Research Disclaimer and General Disclosure

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.