Before the dawn of the battery battle, does CATL deliver the final blow?

On the evening of March 15, 2024, CATL announced its full-year performance for 2023. Dolphin Research broke down the performance of the fourth quarter, focusing on marginal changes.

1) Double decline in revenue MoM, below expectations: The shipment volume is basically in line, but the revenue is significantly below expectations. Behind this is the market underestimating the downward trend in the unit price of CATL's battery products. In the second half of the year, the price of power batteries per Wh has dropped to around 0.8 RMB.

However, with known profits, it can only be said that the market has not fully recognized the impact of raw material deflation on CATL. With profits stable and market share recovering, the decline in revenue is just due to deflation, which is not a major issue.

2) Gross profit margin exceeds, but not as exaggerated: Although the gross profit margin in the fourth quarter seems to greatly exceed market expectations, reaching close to 26%, due to the impairment of inventory in the fourth quarter, the actual gross profit margin, excluding impairment, increased by less than 2% compared to the third quarter. Therefore, while the gross profit margin in the fourth quarter is strong, it is not as strong as it appears at first glance.

3) Sharp increase in sales expenses, operating leverage release not as expected: Sales expenses in this quarter were 7.7 billion, a MoM increase of 120%, possibly due to the need for more sales and operation maintenance for energy storage, as well as higher operating expenses for overseas market expansion. The core operating profit margin (income minus operating expenses and impairment) remained flat QoQ in the context of the increase in gross profit margin, just not worse.

4) Sharp drop in overseas growth rate: In the second half of last year, CATL's overseas revenue growth rate can be described as a flash crash, with the YoY growth rate dropping from nearly 200% to 20%. Moreover, the growth is mainly due to contributions from energy storage, while the overseas expansion of power batteries is temporarily hindered.

5) Inventory hits bottom, turning point approaching? From a magnified analysis perspective, looking at the absolute decrease in inventory value at the end of the fourth quarter, as long as new energy vehicle sales continue to recover and lithium carbonate prices remain stable at 100,000 RMB/ton instead of dropping to 50,000, the inventory devaluation risk due to raw material deflation is basically coming to an end.

Dolphin Research's summary:

From the marginal incremental information of the fourth-quarter performance and the 2023 annual report, it can be seen that in terms of the financial statements from revenue to profit, the biggest positive - net profit has actually been released ahead of time.

In terms of the actual core operating profit considering financial leverage and the impact of asset impairment, although it remained flat compared to the third quarter, it is clear that it did not perform as well as the net profit release.

The real biggest positive of this performance is that due to the actual discount from asset impairment, and despite the poor revenue, CATL was able to achieve a greater deflation on the cost side in a situation of severe price deflation, ensuring the gross profit margin. This is still backed by the industry chain's strong pricing power.

So, in terms of this performance itself, Dolphin Research's judgment is quite accurate, but it is not reflected as well in the numerical performance.Dolphin Research is particularly optimistic about the "cyclical leader" capability demonstrated by Ningwang as a leader in a weak cycle behind its inventory and production capacity this time:

By 2024, when Ningwang's inventory pressure is alleviated and production capacity utilization is not high enough, Dolphin Research has every reason to believe that it can leverage its current gross margin control capabilities, economies of scale, and brand effects to increase production capacity utilization. This will further intensify the price war in the iron-lithium ordinary production capacity, delivering the "last straw" to some struggling second and third-tier players in the domestic battery industry, accelerating the clearance of production capacity.

Moreover, despite the short-term setback in Ningwang's overseas growth logic, the domestic clearance war of Ningwang, which has completed destocking, is seen by Dolphin Research as a tactical operation and a necessary choice for business development.

In this scenario, entering the new year, factors such as a significant MoM decline in electric vehicle sales, renegotiation of battery supply prices, and possible price reductions by Ningwang to clear the industry may temporarily pressure Ningwang's performance. However, with its strong Alpha capability, Dolphin Research believes that its valuation inflection point may come earlier:

Ningwang has cleared the risk of asset impairment and actively destocked. After shedding these burdens, Ningwang will start using its capabilities to leverage its abundant production capacity to initiate a market cleanup.

Ningwang's price reductions unsettle competitors, leading to subsequent production capacity clearance and a return to market concentration.

Incremental growth in overseas business, especially in Europe, as subsidies gradually decline and penetration rates approach challenging price bands, Ningwang, with its iron-lithium batteries and low-cost advantages, is poised to seize market share from Korean battery manufacturers (Korean battery manufacturers mainly produce NCM batteries, with large-scale supply of LFP batteries expected by 2025).

Despite performance not yet being cleared, Ningwang has a superlative cash generation capability: Ningwang itself has a strong operating cash collection capability - the attributable profit of 13 billion corresponds to operating cash inflows of 40 billion in the same period.

a. With domestic expansion coming to an end and overseas factory construction not progressing rapidly, capital expenditures have decreased - from 600 billion in 2022 to just over 300 billion; capital expenditure efficiency has improved, as the unit capital expenditure required for the same production capacity has significantly decreased due to process improvements.

With substantial cash generated from operations and continued reduction in capital expenditures, increasing dividends is evidently a leading example for A-share companies. Ningwang, leading by example, has chosen to distribute dividends as high as 22 billion yuan, far exceeding market expectations, with a dividend payout ratio of 51% in 2023, providing investors with a certain bottom line.

Therefore, compared to 2023, as a Beta stock that follows the trend of lithium carbonate prices, Dolphin Research believes that in 2024, attention should be paid to Ningwang's reversal opportunities.I. Turning Point Approaching?

Despite doubts about Ningwang's visibility in core competitive barriers and overseas operations, no one questions Ningwang's leading position as a global battery manufacturer. In other words, in Ningwang's pricing, the cyclical nature becomes more prominent, making industry cycles and operational turning points more critical. Therefore, in this earnings report, Dolphin Research first focuses on inventory and impairment issues.

a. Inventory Impairment Risk Confirmed

Let's first look at the long-standing concern in the market about inventory impairment risk: due to the high proportion of "finished goods" in Ningwang's inventory structure and the continuous decline in lithium prices, the market is worried about a high risk of impairment.

This concern has finally been confirmed. In the fourth quarter, asset impairment provision reached 3 billion, a significant increase to 7% of the original asset value. This means that even though Ningwang's procurement costs are low, the inventory of finished goods could not withstand the pressure as the price of lithium carbonate dropped to below 200,000. Consequently, substantial impairment was necessary.

b. Will there be further impairments after this? Yes, but the risk should be reduced

By the end of 2023, the inventory of battery systems remained at 70 GWh, the same as the end of 2022. However, the overall shipment volume in 2023 was 390 GWh, an increase of 100 GWh compared to 2022. Based on the 2023 shipment level, this inventory can only support production for two months without any new output.

Furthermore, with the increase in capacity utilization in the second half of the year, it is highly likely that the 70 GWh inventory, under the current shipment scale, has become a stable inventory, unless downstream vehicle sales collapse continuously. From the perspective of GWh volume, it is challenging for Ningwang's inventory to decline further.Is there a risk of further impairment of inventory for Ningwang?

Here Dolphin Research provides an observation perspective: with the same year-end inventory of 70Gwh, the inventory value in 2023 has dropped to only 45.4 billion RMB, a direct decrease of 40% compared to the same period last year; and based on the daily price of lithium carbonate, the price of lithium carbonate in 2023 has also decreased by 46% compared to 2022.

In other words, the reduction in the book value of Ningwang's inventory in 2023 is basically synchronized with the average price drop of lithium carbonate. This also indicates that Ningwang has made sufficient impairment. If the price of lithium carbonate does not further decline, the risk of impairment due to natural material price reduction becomes very small with a unit price of 100,000.

The remaining risk mainly lies in whether Ningwang will engage in a price war in the lithium iron battery market with its own non-high-end ordinary production capacity to accelerate market clearance. Dolphin Research believes that this risk cannot be ruled out, but even if it exists, with limited room for natural material price reduction, the impairment amount has also been greatly reduced.

c. In 2024, will Ningwang clean up the battlefield?

This is mainly because, although Ningwang's proactive destocking has come to an end, its capacity utilization rate is still only 70%. In a relatively low state, increasing the capacity utilization rate can offset a certain unit price decline. After Ningwang's proactive destocking, it can completely use the scale effect of increasing capacity utilization rate and lowering prices to accelerate the clearance of competitors' capacity and gain market share.

Combined with the industry information Dolphin Research has learned - in terms of Ningwang's competitive strategy in the domestic market, it does intend to maintain its high-end and gross profit margin through research and development and product strength, while using price reductions in ordinary lithium iron battery production capacity to accelerate capacity clearance and increase its market share. Moreover, Ningwang's battery market share has shown signs of recovery in January and February.

The hidden value behind the skyrocketing gross profit margin actually comes with a discount

Under the backdrop of price wars in downstream vehicles and upstream lithium mines, Ningwang's gross profit margin in the fourth quarter unexpectedly increased by three percentage points, reaching close to 26%, which significantly exceeded market expectations. This was originally the biggest highlight of this quarter's financial report, which could be used to prove Ningwang's product competitiveness in the price war.

However, due to the significant impairment of inventory this time, Dolphin Research has entered a US stock standard (impairment included in cost) gross profit margin. It can be seen that after taking into account the inventory impairment loss dominated by inventory, its gross profit margin in the fourth quarter did improve, but only by 1.7 percentage points compared to the third quarter, which is indeed an improvement, but not as high as it appears on the surface.

Analysis: Ningwang's Strong Profit Margin Control and Challenges in Revenue

Ningwang's ability to control profit margins is robust, with raw material deflation outpacing the decline in selling prices. The transmission of cost reductions from materials to complete vehicles may have a time lag. If Ningwang settles raw material costs weekly but has a slower settlement cycle for downstream complete vehicles, there will be a time advantage. However, this control ability itself reflects the bargaining power in the industrial chain.

Issue: Seemingly Poor Revenue, Is It Really a Problem?

After analyzing the two relatively positive points in the earnings report, let's now look at the "seemingly" problematic areas.

In the fourth quarter of 2023, quarterly revenue was 106.2 billion, a 10% year-on-year decline, lower than the market's expected 115.5 billion, significantly below expectations. Due to the decent performance of the gross profit margin and the situation of basically clear shipments, the revenue decline can mainly be attributed to deflation caused by the downward trend in battery materials such as lithium.

This lower-than-expected performance is essentially due to the market not fully pricing in the deflation of raw materials, which is a market expectation issue rather than a problem with Ningwang.

Looking at the marginal changes, Ningwang's battery sales volume in the fourth quarter was 120GWh, a 20% increase compared to the previous quarter, but total revenue remained almost flat, indicating a significant decrease in the unit price of Ningwang's batteries.

So, how significant is the price reduction of the core power batteries? Let's find some data from the second half of the year's financial report:

Looking at the split business in the second half of 2023, the year-on-year decline in revenue mainly came from the decline in revenue from power batteries, which decreased by 7% in the second half of 2023 compared to the previous year.

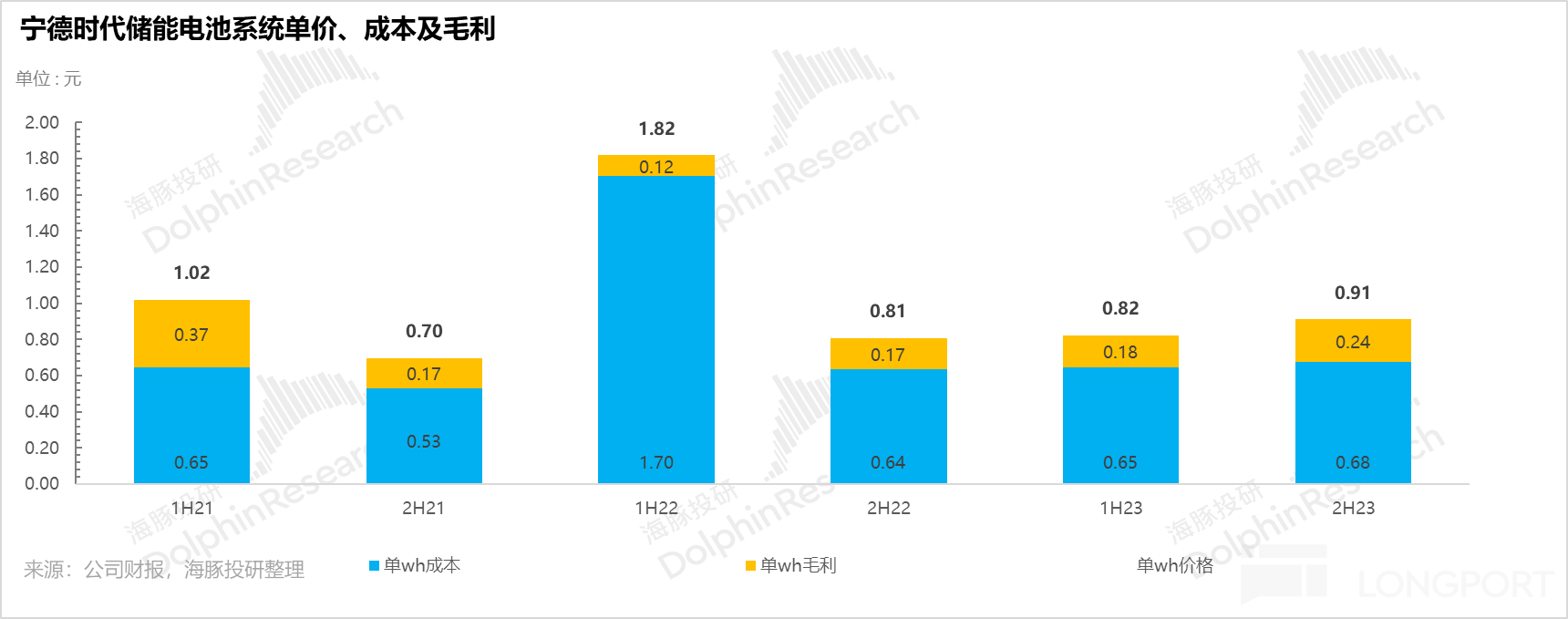

The reason for the decline in revenue from power batteries is mainly the decline in unit price, which dropped by 25% from 1 yuan/Wh to 0.79 yuan/Wh in the second half of 2023, a decrease of over 25%. Even with a 20% increase in shipments year-on-year, revenue from power batteries still saw a 7% year-on-year decline.

Currently, the comprehensive unit price of Ningwang at 0.8 yuan is still much higher than the spot market price of around 3.5 yuan and the unit price of iron-lithium batteries around 0.4 yuan, indicating that Ningwang indeed has room for price reduction.

Overseas Market: Facing Obstacles

In the second half of last year, the overseas market generated $65.3 billion in revenue, but the contribution rate dropped to 31%. If defining a global company as one where overseas revenue contributes 50%, Ningwang has not yet achieved this.

In the second half of the year, the YoY growth rate of overseas revenue slowed significantly from 195% in the first half to 19%. The slowdown is attributed to factors such as the deceleration in export capacity to overseas clients like Tesla, and hindered output exports due to trade protectionism, as well as the slow progress in overseas localization capacity building.

Currently, Tesla is facing pressure in short-term overseas market expansion due to its China-centric supply chain elements, which prevent models like Model 3 from enjoying the full $7,500 U.S. subsidy policy.

Despite encountering obstacles in overseas growth, the profitability of overseas operations is relatively stable as it is less competitive than the domestic market. The gross profit margin has rebounded to 29% in the second half, slightly lower than the peak of 30% during the high lithium prices period.

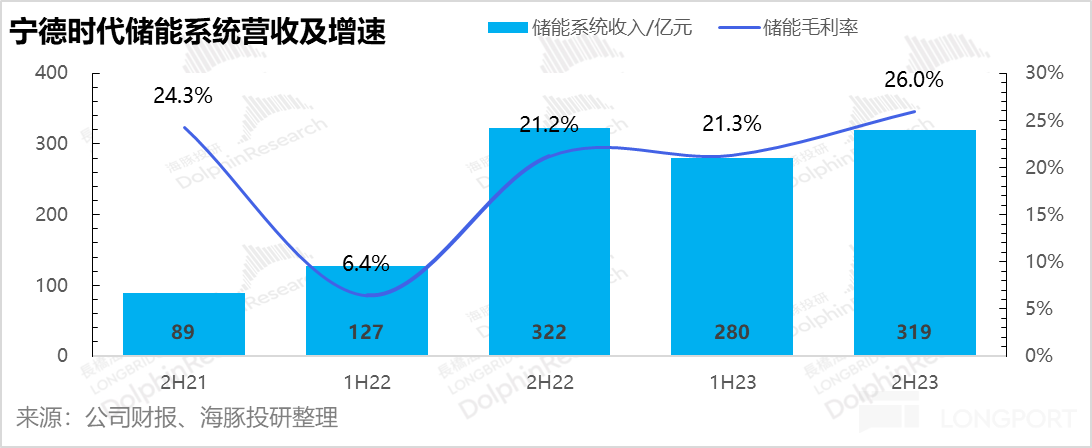

IV. Energy Storage Batteries: Gross Margin Recovery Driven by Price Increase

The second-largest high-growth business experienced a slight decline in revenue in the second half, reaching 31.9 billion, a 1% YoY decrease. However, the gross profit margin showed strong performance, increasing by five percentage points QoQ to 26% in the second half.

Since many energy storage projects are driven by projects, the time from signing to implementation is relatively long. The impact of raw material price changes on orders and performance realization has a longer cycle.

Combined with a significant increase in comprehensive service fees on the marketing end, and the continued rise in the unit price of energy storage shipments, it is estimated that the increase in the proportion of high-margin overseas energy storage business may have contributed to this improvement.

V. Profit Exceeds Market Expectations

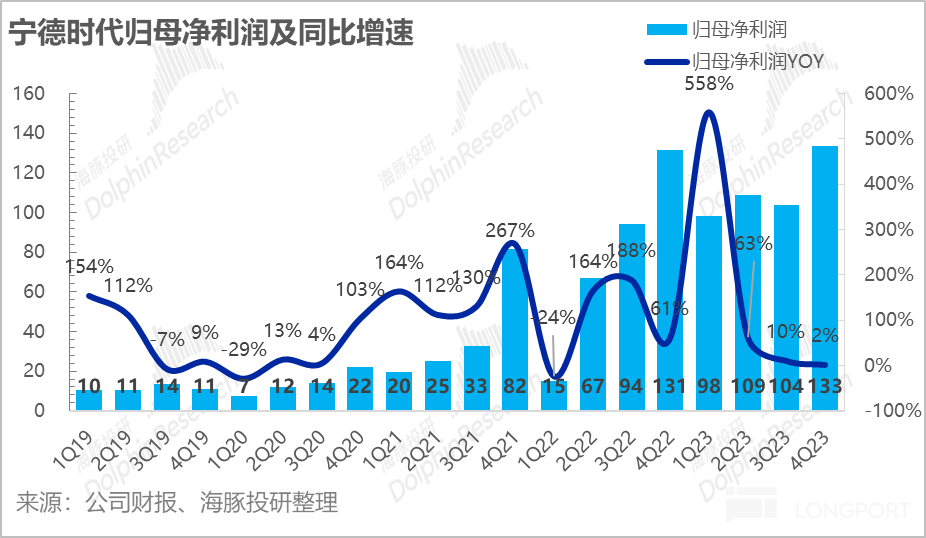

After reviewing core revenue and gross profit, let's look at the company's profit situation in the fourth quarter: the net profit attributable to shareholders in the fourth quarter was 13.3 billion yuan, with a profit margin of 12.6%, exceeding the market's expectation of 11.1%.

The reason why the net profit looks good is mainly due to the excessive cash on hand, the increase in cash management income, and the increase in investment income from joint ventures.

However, due to non-operating investment gains and losses in net profit, as well as interest income related to the company's financial leverage and strong cash and credit capabilities, Dolphin Research pays more attention to the core operating profit (revenue - taxes - three fees - asset & credit impairment) compared to its U.S. counterparts.

Image 1 Image 2 Image 3When looking at the core profit, it can be observed that although the net profit attributable to the mother in the fourth quarter is impressive, the core operating profit margin in the fourth quarter is basically the same as the previous quarter. Behind this, in addition to the high asset impairment mentioned earlier, another important reason is the sharp increase in sales expenses.

{kind=link}

{kind=link}

{kind=link}

VI. Expense Side: Sharp Increase in Sales Expenses

With the rapid expansion of the company's business scale, the corresponding expense scale is also showing a rapid expansion trend. Previously, due to the rapid growth in revenue, management, research and development, and sales expenses could be adequately diluted.

However, the performance on the revenue side this quarter was mediocre, coupled with a 120% MoM surge in sales expenses to 7.7 billion, mainly due to the significant increase in the largest project's after-sales comprehensive service fees, which grew by 74% YoY.

Overall, it seems to be related to the need for more sales and operation maintenance in energy storage, as well as higher operating expenses for overseas market expansion. Although administrative and research and development expenses both decreased this quarter compared to the previous one, the sharp increase in sales expenses has eliminated the leverage effect on the short-term operating side.

October 19, 2023, Earnings Report Review: "Ning Wang: Slowing Growth, When Will the Trillion-Dollar Era Return?"

October 20, 2023, Conference Call Summary: "Slowing Growth, Will Ning Wang Continue to Sacrifice Market Share to Maintain Gross Profit?"

July 25, 2023, Earnings Report Review: "Ning Wang: Stable but 'Mediocre' Changes"

July 25, 2023, Conference Call Summary: "CATL Summary: Expanding Overseas, Holding onto Gross Profit"

On April 21, 2023, Ning Wang: Perfect Reversal Expected? Rich Reserves are Key was published.

On April 21, 2023, CATL: Grasping Energy Storage and Overseas Markets, Keeping Gross Profit Stable (Summary) was released.

Financial Report Review on March 9, 2023: CATL: Car Manufacturers Cry, Batteries Smile, How Far Can This Profit Go?

Summary of the Phone Conference on March 9, 2023: CATL: "Current Gross Profit Margin is at a Reasonable Level" (Summary)

Financial Report Review on October 22, 2022: Ning Wang is Highly Regarded by Many, Next Year Will Be the True Test of Love

Summary of the Financial Report Phone Conference on October 22, 2022: Lithium Prices Will Decrease Next Year, Electric Vehicle Penetration Rate Will Exceed Expectations

Financial Report Review on August 24, 2022: CATL: Minor Setbacks are Just Interludes, Being Extraordinary is the Main Theme

Earnings Report Summary on August 24, 2022: "No Worse Performance in Power Battery Profit in the Second Half of the Year than in the Fourth Quarter"

Overview of the Power Battery Sector on May 20, 2022: "The Collapse of New Energy, Are We at a Crossroads in Investment?"

Earnings Report Review on April 30, 2022: "Performance Thunder Strikes as Expected, Is the Era of Ning Wang Coming to an End?"

Earnings Report Conference Call on April 30, 2022: "Ning Wang Unconcerned about Performance Thunder, Market Share and Customer Structure are the Key Observational Indicators"

Earnings Report Review on April 22, 2022: "Sentiment Affects Valuation, CATL Faces Dual Challenges of Profitability and Confidence"

Earnings Report Review on October 28, 2021: "Facing the Outstanding CATL, Should Valuation Still be Feared?"

Earnings Report Review on August 25, 2021: "CATL: Investment Beyond Distant Stories, Focusing on Current Performance"

In-depth Company Analysis on July 14, 2021: "CATL (Part 2): Is Faith Building a 'Rigid Bubble'?"

In-depth Company Analysis on July 7, 2021: "CATL (Part 1): Where Does the Confidence of Trillion-dollar Market Value Come From?"

For the risk disclosure and statement of this article: Dolphin Research Disclaimer and General Disclosure

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.