Costco: How does the retail "snail" forge an "indestructible body of gold"?

In the first part of our series on Costco research, we clearly identified two key points where Costco's greatest scarcity lies:

- The stable growth on the demand side almost ignores macroeconomic and technological cyclical changes. The reason behind this is that Costco actively adheres to low gross profit margins (i.e. markups) to benefit consumers, focuses on product quality and a more risk-resistant middle-class consumer group, and concentrates on categories such as fresh food and daily necessities that have "sustainable demand". Their business philosophy is not about seeking speed but stability, and aiming for long-term success.

However, if Costco only excels in steady but not outstanding growth, it is not enough to become a benchmark in the entire retail industry. 2) After actively reducing gross profit margins and self-imposed restrictions, how Costco achieves profits that are not inferior to its peers through excellent supply chain, store, cost, and expense control is the second key point of Costco's scarcity, which is the main topic of our discussion in this article.

The following is the content of the analysis:

1. Low Gross Profit, Low Expense Ratio, Not Low Profit Margin

Starting from the perspective of results, taking the 23rd fiscal year as an example, Costco has a gross profit margin of just over 10% (compared to peers, which is 10-20 percentage points lower), with an operating expense ratio of only 8.9% of revenue, while typical competitors have operating expense ratios of at least 19% or higher. With low expenses matching low gross profit, Costco's operating profit margin is slightly above 3%.

Among several typical companies in various retail formats, Dollar Tree in the soft discount model has the highest profit margin, close to 8% (reflecting that the profit margin of absolute low-priced goods may be higher compared to mass-market goods), and the comparable operating profit margins of most offline retail formats are mostly between 3% to 6%. Costco's profit margin is indeed relatively low compared to peers, at the lower end of the range, but not a significantly outlier.

Looking across time, as a mature business, the operating expense ratios of various players in different formats or markets in offline hypermarkets are relatively stable, with only small fluctuations around the central level determined by their different models and operating strategies. Between 2010 and 2023, except for the 20 years affected by the epidemic, Costco's operating expense ratio has remained stable in the range of 9% to 10% with minor fluctuations. This also seems to indicate that, in the absence of major changes in the business model, the operating expense ratios of offline hypermarkets do not show a trend of declining space.

Therefore, this leads to the main purpose of this article, which is to try to answer how Costco manages to achieve an operating profit margin that is not significantly different from its peers, despite having a gross profit far lower than its peers.How is it possible to achieve a cost rate that is less than half of competitors while delivering service quality and user attractiveness that exceed the norm?

2. The real "secret" behind the low cost rate is the extremely high store efficiency

From the results perspective, we can see that Costco's operating cost rate (as a percentage of revenue) is nearly 10 percentage points lower compared to other top offline supermarkets. So what are the specific reasons behind this significant difference in cost rates? Logically, from the perspectives of the denominator and numerator, a low cost rate may be due to an absolute efficiency advantage, meaning that the operating expenses per store can be lower; or it may be that the absolute expenses are not low, but are diluted by strong sales.

Since a considerable portion of operating expenses for offline supermarkets are relatively fixed, such as lease expenses for stores and equipment, depreciation, electricity, personnel wages, etc., once a store is opened and operating, these expenses are almost fixed regardless of the sales volume. Therefore, looking at it from a single store perspective can help us decipher the reasons behind Costco's "low operating cost rate".

In the above image, we compared the single store revenue and operating costs of Costco and BJ's Wholesale (a membership-based wholesaler in the North American market, similar to Costco). It can be seen that Costco's average single store operating expenses exceeded $25 million in the 23rd fiscal year, while BJ's single store operating expenses were around $8.4 million. Costco's single store operating expenses are 2.2 times that of BJ's, which is relatively high in absolute terms. Additionally, Costco and BJ's have similar store sizes (both over 10,000 square meters), and BJ's SKU count is higher than Costco's, indicating that BJ's lower single store operating expenses are not due to smaller store size or lower supply weight.

The real "secret" behind the lower cost rate compared to competitors is that Costco's average single store sales revenue is close to $290 million, which is 3.4 times that of BJ's. That is, with twice the investment in single store expenses, Costco achieves three times the sales of a single store. In other words, Costco is not being "stingy" or cutting corners on expense investment, but is actually taking on higher operating expenses compared to competitors for better service quality and user experience (which will be discussed in more detail later). The true winning factor is that high expenses and good service can lead to higher single store sales, thereby diluting the higher investment.

3. What are the real reasons behind the high store efficiency?

As seen above, one of Costco's key success factors is its significantly higher single store sales capability compared to competitors, or in other words, its sales per unit area. Comparing the single store operations of Costco, Sam's, and BJ's, all belonging to the membership-based discount wholesale supermarket category, we can see that Costco's single store sales are nearly 2 times that of Sam's and 3 times that of BJ's.After removing the impact of differences in store area, Costco's sales per square foot are still 1.8 times that of Sam's and 2.6 times that of BJ's. The key question we need to explore is - what are the reasons that lead to Costco's single-store sales and sales per square foot being several times higher than its peers?

Based on the research data on the average customer spending and shopping frequency of several typical supermarkets in the figure below, it can be seen that Costco's average annual shopping amount per user is about $3000, which is roughly similar to Walmart's $2800. However, in terms of single-store sales, Costco is about 3 times that of Walmart.

With little actual difference in per capita spending, there is a significant difference in single-store sales, which can only be reasonably explained by - Costco serves a significantly higher number of users per store than other peers, with data indicating approximately 2-3 times that of Walmart and Target.

As a cross-validation, by calculating the total number of paid members/total number of stores, it is indeed evident that Costco's average number of members served per store is approximately 3 times that of BJ's, which is consistent with the roughly 3 times difference in single-store sales between the two companies. Therefore, we can confidently infer that compared to Walmart and BJ's and other supermarkets with relatively high sales per square foot, Costco's revenue per individual user is actually similar (or Costco is not significantly better than its competitors in terms of average spending and shopping frequency), the main reason for the difference in sales per square foot or single-store sales is the gap in the number of consumers covered by each store.

How can we understand Costco's ability to have several times more single-store users than its peers? Dolphin Research believes there are several possible explanations:

① From the comparison between Walmart and Costco, we believe that the difference in store numbers or store density is likely the main reason for the approximately 2-3 times difference in the number of customers covered by each store. According to statistics, Walmart currently has over 4600 stores in the United States, with over 3500 large supercentersIn comparison, Costco has only about 600 stores across the United States. It can be seen that Walmart has 7.7 times the total number of stores as Costco in the U.S., and even 5.8 times more in terms of large stores alone.

So, how does store density affect the efficiency of individual stores? Let's create a scenario model under ideal assumptions. Assuming a market in city A has a total of 100 users, all users have the same spending power. With different store densities (at a ratio of 7:1 as mentioned above), and assuming that Walmart and Costco have the same service/product quality and attractiveness to consumers, Walmart and Costco each attract 50 consumers, resulting in equal total revenue. However, the number of consumers served by a single Costco store will be 7 times that of Walmart. In other words, in an ideal scenario, for Costco and Walmart to generate the same revenue, Costco only needs to operate 1 store, while Walmart needs to operate 7 stores, leading to a significant difference in the cost/revenue ratio.

In reality, Walmart's greater number and denser coverage of stores will inevitably allow it to reach a larger total number of users compared to Costco. Therefore, in reality, the difference in the number of individual store users and sales between the two is 1:2~3, rather than the idealized 1:7. However, while increasing the number of stores can help reach more new users, as the total number of stores grows, the marginal utility of attracting new customers to new stores will inevitably trend downward, leading to a decrease in the effect of individual stores. This is a well-known common sense.

For decades, Costco has adhered to a "slow" pace of opening new stores (with most years seeing only a dozen or so new stores), reflecting the philosophy and results behind it. By strictly controlling the pace of opening new stores, Costco tries to mitigate the effect of mutual erosion between stores, preferring to sacrifice the total revenue, and instead focusing on ensuring the number of users and sales per individual store, thereby diluting operating costs. In simple terms, it would rather have 1 store earn 1 unit of revenue than have 10 stores earn 3 units of revenue.

However, for the above logic to hold, the premise is that businesses need to have strong attractiveness to consumers, so that consumers are willing to "go the extra mile," meaning not needing stores to find users, but rather having users seek out the stores. However, evaluating the attractiveness of different supermarkets or retail channels to consumers is a difficult and complex issue to quantify and analyze accurately. But as mentioned earlier, Costco's average operating cost per store is more than double that of BJ’s, and Dolphin Research believes that a possible reasonable explanation is that Costco pays more in fees and employee costs to provide high-quality service to consumers, thereby making them more attractive to consumers.As a side verification, according to research data from a certain recruitment website in the United States (not official disclosure, there may be deviations from the actual situation), Costco's average wages for frontline employees are generally at least 10% to 20% higher than Walmart's. It can be seen that Costco's employee benefits should be higher than its peers.

As another side verification, the logic of "high employee benefits → high-quality service & outstanding consumer experience → strong consumer attractiveness/loyalty" has been verified in China's cross-market as well, with the case of Pinduoduo.

According to the analysis of Pinduoduo's business model on the internet, it can be seen that Pinduoduo's employee wages, vacation time, and various employee benefits are generally much higher than its peers, quite generous. However, Pinduoduo also has quite strict requirements for the service attitude and content of its employees, with the contract being terminated after three instances of providing a poor experience to consumers. In simple terms, by using high benefits and high welfare as "investment", ensuring a relatively high stability and willingness to serve among employees, and then providing consumers with a shopping experience superior to its peers through high standards of service requirements and management for employees. With outstanding service (of course, along with low-priced quality products) attracting consumers, although Pinduoduo only has a few stores with extremely low store density, it is quite common for local and even national consumers to specifically go to Pinduoduo for shopping. This validates the feasibility of the business strategy of "making consumers actively seek out stores".

Therefore, we believe that Costco, with a similar philosophy and experience, is likely to achieve low store density and high operating expenses through similar strategies, but with a higher number of users covered per store and higher single-store sales, thereby diluting operating expenses through a "curve-saving" approach.

In summary, the analysis of the second and third paragraphs above shows that on the sales side, Costco provides relatively low prices among quality, high-priced products, rather than absolute low prices of low-quality products, while on the cost side, Costco also chooses high expenses and good service, relying on stronger single-store sales to dilute costs, rather than a simple and crude cost control logic of low expenses and low service.

4. Streamline SKUs to reduce burden on the supply chain

In addition to "actively" controlling store density and the top store-level efficiency brought by "consumers seeking stores", Costco's "streamlining" of SKU numbers also plays a role in diluting operating costs. According to statistics, Costco's single SKU sales are about 3.9 times that of Sam's, reaching approximately 16x to 40x compared to BJ's / Walmart / Target. Taking the reciprocal of this significant difference in single SKU sales, Costco's average supply chain & management costs per SKU are significantly advantageous after being diluted by sales revenue.

In more straightforward terms, Costco is obviously lower than its peers, with only about 4,000 SKUs. Logically, the management cost on the numerator side is relatively lower (such as fewer suppliers to deal with, fewer differences in storing and transporting goods), while the single-store sales on the denominator side are 2-3 times higher than its peers. The resonance of these two aspects reflects Costco's significant efficiency in product procurement supply chain and cost advantages after dilution.

Extending from Costco's significantly higher sales/SKU ratio compared to its peers, with fewer stocking varieties and stronger sales per unit area, Costco's annual inventory turnover rate has been above 12x, while its peers are generally below 8x. This means that Costco's inventory turnover time is at least one-third lower than its peers, and potential inventory losses will also be reduced.

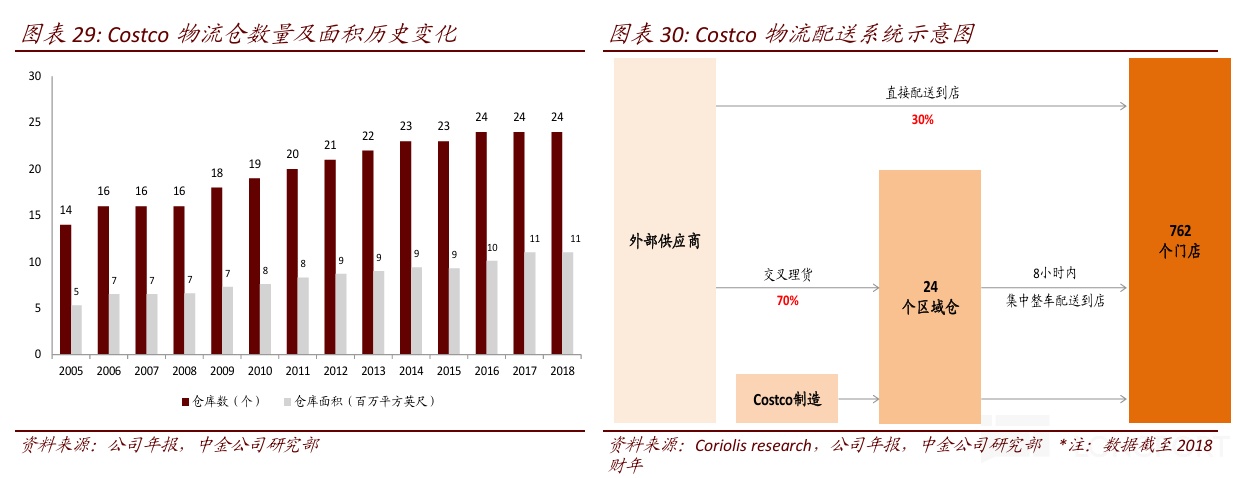

Furthermore, in order to further reduce the costs and expenses of the supply chain and transportation, Costco has specifically built a supporting logistics distribution system. As shown in the diagram below, only about 30% of Costco's products (possibly those with higher timeliness requirements) are directly delivered to 800 terminal stores, while 70% of the supply is first centrally distributed to more than 20 regional warehouses before being delivered to terminal stores. In abstract terms, the complexity of distribution has been compressed from the scale of 800 to 20+, thereby reducing distribution costs.

Between 2007 and 2019, it can be seen that Costco's distribution centers and area have increased by nearly 60%. This is close to the 60% increase in the number of Costco stores from 488 to 783 during the same period. In other words, the pace of adding new distribution centers matches the opening of new stores at a nearly 1:1 ratio, rather than the scenario where Dolphin Research Institute hoped for slower growth of fulfillment centers compared to store growth. It can also be seen that Costco did not seek to increase the workload of individual distribution centers to dilute costs.

On the contrary, in 2020, Costco acquired Innovel (a logistics company), as shown in the image below, the area of distribution centers in 2020 more than doubled, aiming to enhance the efficiency and timeliness of logistics distribution and cope with the growth of Costco's online retail business.

5. Own brand accounts for 1/3, but not outstanding

Looking across various retail channels (not just supermarkets), launching private label/own brand products is a common practice, and Costco is no exception. The benefits of private label products include: ① Reducing the levels of the supply chain, thereby lowering backend production costs and frontend prices; ② Own brand products to a certain extent also solve the problem of homogenization of retail channel products, alleviating the homogenization problem of "I have it, others have it", which is beneficial for user stickiness. In terms of results, Costco's own brand Kirkland accounts for around 30% of revenue and SKU share. From an absolute perspective, Costco's achievements in private label products are quite good.

However, relatively speaking, spanning various retail industries (including mass supermarkets, membership discounts, $10 stores, pharmacies, etc.), Costco's approximately 30% share of private label products can only be considered average. In contrast, Aldi's private label products account for as high as 70% to 80%. Therefore, Costco's private label products do not seem to have any outstanding features.

6. Self-built properties, slow store openings but advantageous in not paying rent

As mentioned earlier, although Costco's scale and market value have been rising, the number of new store openings has mostly remained below 20 per year. The conservative pace of opening stores actually contributes to costs and expenses. Nearly 80% of Costco's store properties are self-owned, and in many cases, Costco selects sites, auctions, and builds stores on its own, with a time span much longer than properties built through leasing, indicating that Costco's store opening pace is significantly slower and indeed constrained by objective conditions.

Compared to the light asset model, which can rapidly expand and reduce initial capital pressure through leasing, Costco goes against the trend by choosing a heavier model, consistently pursuing stability over speed. However, with the majority of Costco's properties being self-owned, the company has significantly reduced the impact of store leasing costs rising with time and inflation. According to the company's disclosure, Costco's leasing costs account for less than 0.15% of revenue, whereas in general, supermarkets have store leasing costs accounting for a low single-digit percentage (e.g., 2% to 5%) of total operating expenses. In other words, after the depreciation period of self-owned properties, only the store leasing cost item can squeeze out a few percentage points of profit margin for Costco

7. Membership Fee Income - A Boost and "Stabilizer" for Profits

Above, we mainly discussed from the perspective of "increasing efficiency and reducing waste" why Costco's operating expense ratio is significantly lower than its peers (at least by 5 percentage points). However, Costco's operating/net profit margin is not excessively behind its peers. From the "open source perspective," the membership model adopted by Costco brings in membership subscription revenue, which is also an important factor. In addition to what we mentioned in the first study, from a business perspective, the membership system actively screens user groups, accurately matches supply and demand, and enhances user stickiness. From a financial perspective, membership fee income is an important supplementary part of Costco's profits.

As shown in the figure below, Costco has adopted a three-tier membership system, namely "Gold Star Member," "Business Member," and "Executive Member," currently charging annual fees of $60/$60/$120 respectively. Historically, the membership fee is raised every few years, but the increase is not significant (each time by $5~$10).

As shown in the figure below, the revenue contribution from membership fees has been in the range of several billion US dollars annually, accounting for approximately 2% of total revenue. The year-on-year growth rate of membership fee income since 2011 has been around 10%, with lower volatility compared to overall revenue. It can be said that membership fee income is not a "driving force" for revenue growth, but more like a "stabilizer."

In terms of profit contribution, in the 2010s, membership fee income once accounted for 70-80% of total operating profit, but the trend has been slowly declining. After the epidemic, the proportion has dropped significantly to around 50-60%. However, unlike some views in the market that membership fee income is the main profit driver for Costco, Dolphin Research believes that this view is "mistaking the means for the end." From the perspective of gross profit margin, the contribution of membership fees of about 15%~17% more accurately reflects the importance of membership fee income to profits, with the retail business itself being the real key.

Although it may seem insignificant, it reflects how to truly value Costco. Membership fees are built on the outstanding and scarce shopping experience brought about by Costco's various trade-offs in operations discussed in the two analyses above, rather than the other way around. Membership fees are more like a small boost to increase profits, which is not qualitatively different from the effect of the company choosing to slightly increase the markup rate by 1%~2%. And as Costco's retail profits continue to improve, the declining proportion of membership fee income is itself silent proof

Fundamentally, the greater value of membership fees lies in: ① Membership fees are paid in advance, before costs and expenses are incurred, providing a predictable and stable source of cash flow, which is particularly important in the early stages of company development (early profit contribution is indeed higher), ② By supplementing and pre-protecting the company's bottom-line profit to a considerable extent through membership fee revenue, Costco as a company has more motivation and possibilities. It operates from the perspective of serving users well rather than determining its own gross profit or profit (for example, selling some goods that may not be of the best quality for the sake of the company's profit margin), thereby better ensuring the interests of users and the company.

8. Conclusion

Through the discussion in these two articles, we have basically explored the revenue end and the cost/expense end from a business perspective. Costco adopts a business strategy of slow store openings, focusing on a limited but high-quality SKU range, and pursuing "relatively low prices under high quality" in both products and services, rather than "absolute low prices under low quality". This approach leans towards "subtraction" and "slow but steady progress". Choosing to "subtract" actually reduces the operational burden, as fewer stores and good SKUs naturally reduce the breadth and difficulty of managing stores and the supply chain for Costco. However, the key point is that Costco relies on high-quality service and products to bring strong user stickiness and store efficiency that is several times higher than its peers, thereby diluting the actual high cost investment.

In the upcoming final article, we will focus on the potential opportunities that have not been fully explored, whether Costco has any special features in shareholder returns beyond performance, and how to interpret Costco's current valuation.

Dolphin Research's previous research on Costco:

September 10, 2024, "Pinduoduo's Idol - Is Costco the 'Ideal Type' of Retail?"

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.