There is no text provided between the '=====' delimiters. Please input some text to be translated.

Hi everyone, I'm Dolphin Analyst.

This morning, on February 3 (February 2 US after-hours), Alphabet Inc. (GOOGL) released their Q4 2022 financial report. Overall, their performance was not good, and they especially mentioned future spending optimization. However, considering the possible pressure on revenue this year, the market may still expect to see more aggressive optimization actions. The key points are as follows:

1. Soft revenue, advertising under pressure but cloud business stable: The overall revenue growth rate for Q4 was 1% YoY, with advertising down 3.6%, worse than market expectations, while Google Cloud maintained a growth rate of over 30%.

The deferred revenue growth rate slowed down in Q4 and the report didn't disclose the amount of confirmed contracts, but with the assumption that Google Play will probably see a YoY decline, cloud services may contribute more to growth. Therefore, it's still too early to say whether cloud services will have a significant slump in the short term, but some caution is needed due to Microsoft's warning about Azure. Also, from Bloomberg's consensus forecast, the market's expectations for 1Q23 are still somewhat high.

2. Lagging profit but signals of acceleration for optimization: The profit for Q4 was also lower than expected due to the drag of weak ad revenue and because the cost-cutting measures started too late. Although spending was controlled in Q4, it wasn't enough to offset the impact of the revenue headwinds and boost profit significantly.

The announced layoff of 12,000 employees in January is expected to be reflected in costs in the next quarter. In the meantime, management emphasized in the performance report that they will optimize office space and extend server usage life in Q1 to achieve cost reduction and efficiency improvement goals.

There were signs of marginal contraction in Q4 based on the net increase in employees. This quarter saw an increase of 3,455 people, nearly half of the expected 6,000 and a significant slowdown compared to the pace of adding over 10,000 people in each of the first three quarters of last year.

3. High exchange rates significantly influence YoY performance: In Q4 of last year, the US dollar index was still relatively high, which had a big impact on Google because over 50% of their revenue comes from regions outside North America. Excluding exchange rate effects, Google's total revenue growth rate was 7% YoY, far higher than the 1% under variable exchange rates. In terms of region, the impact was greatest in Europe and Asia-Pacific, with positive growth rates of 7% and 5% respectively under constant exchange rates, which was significantly better than the YoY decline of 6% from the original disclosure.

4. The company's strategic focus continues to tilt towards AI and DeepMind will be spun off into a separate column. The description of business progress and future guidance from management in performance reports has always been minimal. This time, the main focus was on their investment and planning in the AI field, as well as some temporary market changes (such as the explosive popularity of ChatGPT). The report mentioned that the company will separate DeepMind from their innovation business and focus on disclosing key information. 5. For more outlook and guidance for next year, please pay attention to the conference call. We will also release the summary and key information to the Longbridge app and user group as soon as possible. Interested parties can contact the assistant (WeChat: dolphinR123) to obtain it.

- Comparison of Key Indicators and Expectations

Dolphin Analyst's View

Meta's results exceeded expectations, so the market had higher expectations for Google's performance today. In addition, the dovish tone of the Fed's remarks led to a strong showing of Google's stock price last night.

In terms of this quarter's financial report, it is certainly not good, mainly due to the unstable macro environment. According to research information from advertising agencies, cautious advertisers in the fourth quarter led to a weak industry, and this trend has continued into January of this year.

Therefore, the pressure on the revenue side in the first quarter is still not small. At the same time, relatively strong search advertising last year will also face the impact of a high base this year. YouTube Shorts ads are about to be launched, and the performance of Reels can make this business area expected to grow. However, since the proportion of YouTube's revenue is not high, one cannot be too optimistic.

However, the Dolphin Analyst believes that Google's current investment logic is not without merits, mainly reflected in:

- The core focus is on the space for improving profits through cost reduction and efficiency improvement: In the three years of the epidemic, Google added more than 70,000 employees, an increase of 60%. Especially in 2022, there were more than 30,000 new employees. However, since the income growth during the epidemic was 75%, it can be understood that there were too many hires. However, after the epidemic bonus is over, the growth style will switch, and the investment in personnel and other costs naturally needs to be adjusted.

The Dolphin Analyst believes that judged by the future growth rate level and the ratio of manpower efficiency, the layoffs of 6% last month may not be enough, and the overall personnel structure still appears bloated. Under the supervision of shareholders, there may be further downsizing in the future. In addition, equity incentive compensation, which accounts for 20%+ of expenses, may also be the direction for management to cut expenses.

If the management team has further actions in the future, whether from the perspective of improving profits or more positive market feedback in the current environment of contraction, there is hope that it will stimulate the stock price.

- The world's leading AI technology gradually generates commercialization capabilities on the business path: As certain application fields are currently developing rapidly, they can enjoy dividends and resist the pressure on the overall advertising business. In the short term, this part of the revenue is also difficult to give a significant contribution to the overall revenue, and more is a good sentiment.

Google's short-term increase is not completely consistent with the current performance, so pay attention to the remarks on the conference call by management (whether there are signals of better-than-expected expenditure optimization). If the conference call does not have a related description, the Dolphin Analyst believes that due to the headwind of search advertising, in the short term, it is best to give up some safety space to realize the two logic viewpoints mentioned above. Currently, the market value of 14 trillion yuan is in the central range relative to the 2023 performance expectations, and the short-term risk-reward ratio is slightly unsatisfactory.

However, if taking a medium- to long-term perspective beyond the lows of this year, Dolphin Analyst still sees the long-term competitiveness of Google, driving profitability back into the normal growth range.

Later, Dolphin Analyst will share conference call notes with Longbridge's Dolphin users through the Longbridge App. Interested users are welcome to add the WeChat account "dolphinR123" to join the Dolphin Research Group and obtain conference call notes as soon as possible.

The following is a detailed interpretation of the financial report.

I. Basic Introduction to Google

Google's parent company, Alphabet, has a wide range of businesses and its financial report structure has changed many times. For those who are not familiar with Alphabet, let's take a look at its business structure.

To briefly explain the long-term logic of Google's fundamentals (which differ from short-term logic):

- Advertising business is the main source of revenue and contributes to the company's main profits. As search advertising faces a long-term crisis of being eroded by information flow advertising, high-growth streaming media YouTube is the perfect replacement.

- Cloud business is the company's second growth curve, although it is not yet profitable, its recent signing momentum is strong. With advertising constantly being dragged down by weak consumption, the development of cloud business becomes increasingly important in supporting company performance and valuation imagination.

II. Advertising pressures are considerable, cloud services are relatively strong

1. Weak revenue exceeded expectations, both main businesses are under pressure this year

In Q4, Google's overall revenue was 36 billion yuan, a year-on-year increase of 1%, lower than the market expectation of 36.5 billion yuan. The main reason was that advertising was much worse than expected. Meta's financial report released yesterday showed that the growth rate of advertising revenue slowed down in Q4, which actually gave the market more expectations in the short term.

Cloud business grew by 32% year-on-year, and the month-on-month growth rate slowed down slightly. In the short term, although the growth rate of deferred revenue has slowed down slightly, which may be more related to the general payment performance of Google Play, it is still suggested to remain cautious about Google Cloud's situation this year, and the current market expectation is a bit too high (a quarterly growth rate of 30%+ in 2023). It is suggested to pay attention to the indicators such as "pending contract amount" in the complete financial report. Comprehensive income varies by region, with better performance in Europe and the United States, and Europe experiencing the highest growth rate when excluding the exchange rate impact. This also reflects that the market is too pessimistic about the economies of the two regions in the short term.

"Although the current economy is not that bad, advertisers are still holding onto their money tightly."

Actual performance in Q4 advertising revenue was CNY 59 billion, a year-on-year decrease of 3.6%, weaker than the market's expected CNY 60.6 billion, a year-on-year decrease of 1%. Search ads (-1.6% YoY) and YouTube ads (-7.8% YoY) both underperformed the core investment bank's expectations. "The accelerated decline from the previous year to match the reduction in advertiser willingness to invest only depends on the degree of acceleration. Meta's better-than-expected performance may still be attributed to its own competitiveness."

Dolphin Analyst expects that "search ads in the first quarter and the first half of the year may still face considerable pressure due to high base numbers," while YouTube ads will need to wait for the commercialization of Shorts to see limited revenue growth for 1-2 quarters.

"Cloud services are strong due to abundant resources, but beware of the impact of the industry's cautious Capex cuts."

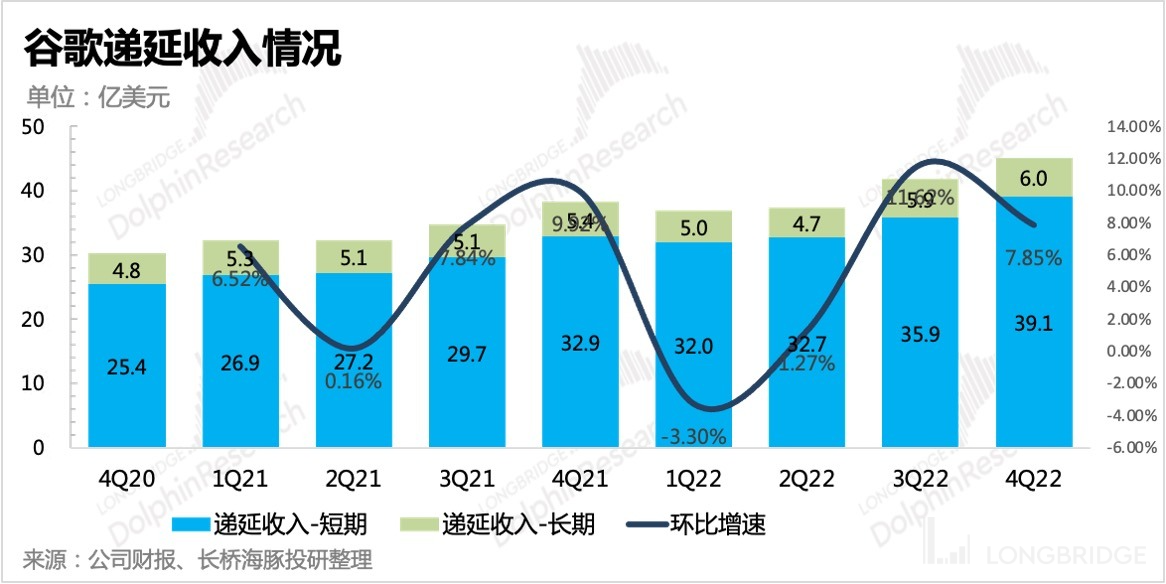

Last year, Google Cloud grew relatively easily due to the signing of several large contracts. In Q4, cloud revenue was CNY 7.3 billion, a year-on-year increase of 32%, which is basically in line with expectations.

As of Q3, there are still CNY 52 billion in contracts to be executed. However, the quarter-on-quarter growth rate of deferred revenue in Q4 did not accelerate as in the past. In addition to the impact of Google Play revenue, the cloud business cannot be ignored.

In conjunction with the guidance given by Microsoft management, caution needs to be exercised for the future expectations of Google Cloud, and the contractual data indicators in the complete financial report can be observed in the future.

!

The histogram description of the chart has been automatically generated

!

The histogram description of the chart has been automatically generated

{kind=link}

3. Further expense optimization is needed

Costs and expenses in the fourth quarter have not improved significantly. Gross profit margin and operating margin are both declining, but the deterioration of profit margin is mainly due to pressure on advertising revenue and an increase in the proportion of loss-making cloud business revenue. In the short term, the comprehensive operating margin will naturally decrease due to changes in the business structure.

Compared with the third quarter, where business investment was still expanding against the trend, the costs, expenses, and net increase in employees in the fourth quarter have all significantly slowed down, indicating that the company has at least adjusted the pace of investment.

Next quarter, the layoff effect of 12,000 people is expected to be reflected, and at the same time, the company will also optimize office space. These two short-term measures will also generate severance compensation and fixed asset disposal expenses, most of which will be confirmed next quarter, with an estimated one-time impact on profits of nearly $6 billion.

In addition, the company has extended the service life of some servers, which will result in a decrease in depreciation costs next quarter.

However, the Dolphin Analyst believes that the current 6% layoff rate is not enough. Compared with the rapid expansion of employees during the three-year period of the epidemic (an increase of 60% compared to the end of 2019 in 2022), employee costs still need to be significantly optimized to match this year's single-digit revenue growth. Whether it is through continued layoffs or salary reductions, especially the equity incentive expenses that account for a relatively high proportion in the Google compensation system (20-25% of total operating expenses), the goal is to improve operating efficiency, maintain and improve profit levels, and avoid shareholders choosing to vote with their feet because of damaged rights and interests.

Dolphin Investment Analysis "Google" Historical Collection:

Earnings season 2022 Phone Conference on October 26th: "Short-term optimization resources, opportunities still lie with search and YouTube (Google 3Q22 phone conference summary)"

2022 Financial report review on October 26th: "Google: Recession is approaching, ad giant has fallen"

2022 Phone Conference on July 27th: "Google: High uncertainty in the economy for the second half of the year, focused on investing in better long-term prospects (phone conference summary)"

2022 Financial report review on July 27th: "Google: 'Hard-line turn' in anticipation of a financial storm"

2022 Phone Conference on April 27th: "Management remains evasive about TikTok, but intensifying competition is still behind the emphasis on Shorts (Google phone conference summary)"

2022 Financial report review on April 27th: "Google: Tackling headwinds, even the giant is struggling"

2022 Phone Conference on February 2nd: "Google is actively seeking expansion through increased investment and accelerated hiring (phone conference summary)"

2022 Financial report review on February 2nd: "Google is expected to soar again with bright performance and rare stock splits"

In-depth

On July 1, 2022, "TikTok teaches 'big brothers' how to do things, Google and Meta are going to change"

On February 17, 2022, "Internet advertising review-Google: watching the changes in the situation"

On February 22, 2021, "Dolphin Research: Dissecting Google - Has the recovery market for advertising giants ended?"

2021, November 23rd, "Google: Performance and stock price soar, strong recovery is the main theme this year"

**Risk Disclosure and Statement of this Article:** [Dolphin Research Disclaimer and General Disclosure](https://support.longbridge.global/topics/misc/dolphin-disclaimer)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.