Netflix: Squeezed user growth, market not buying it?

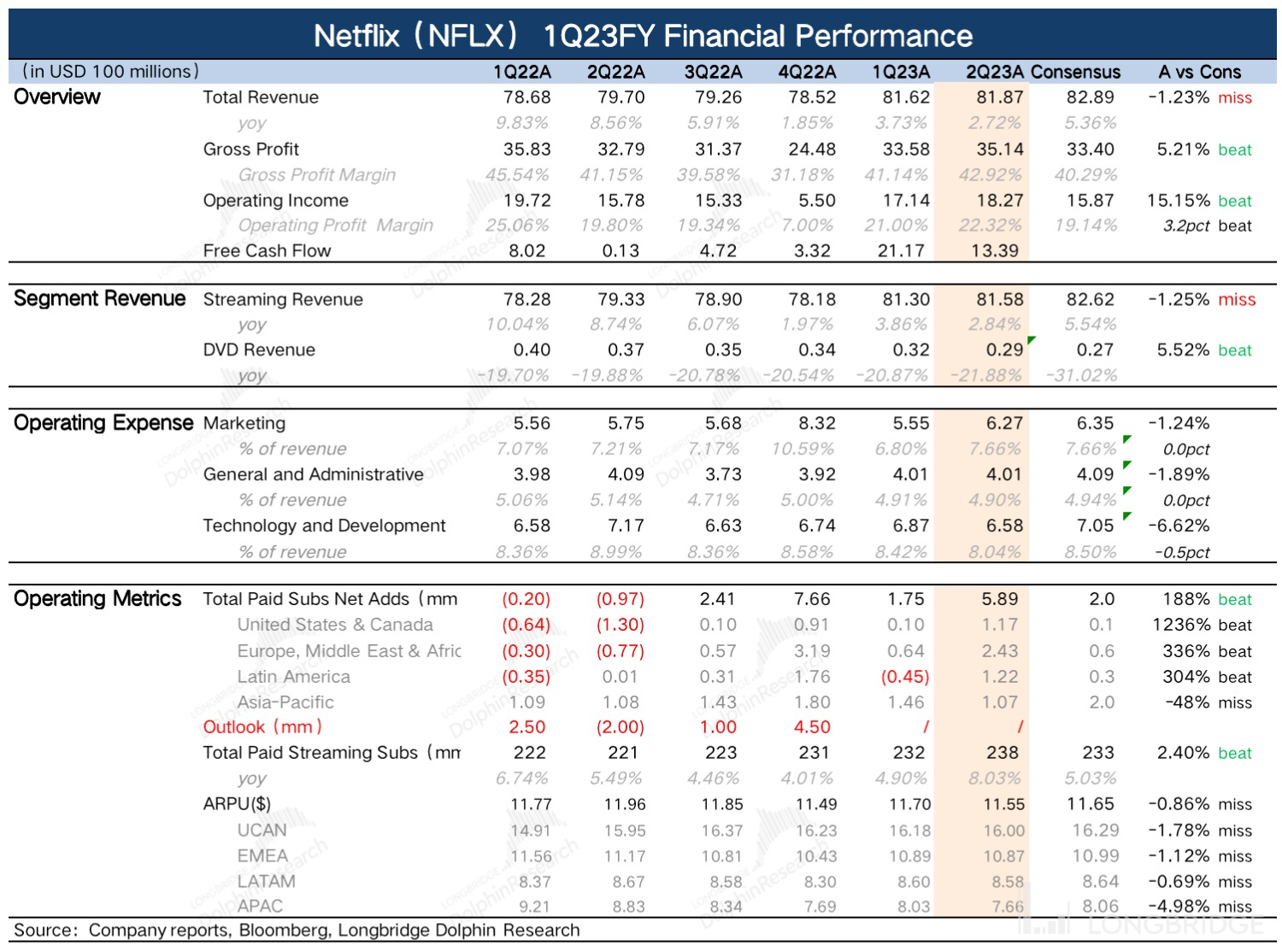

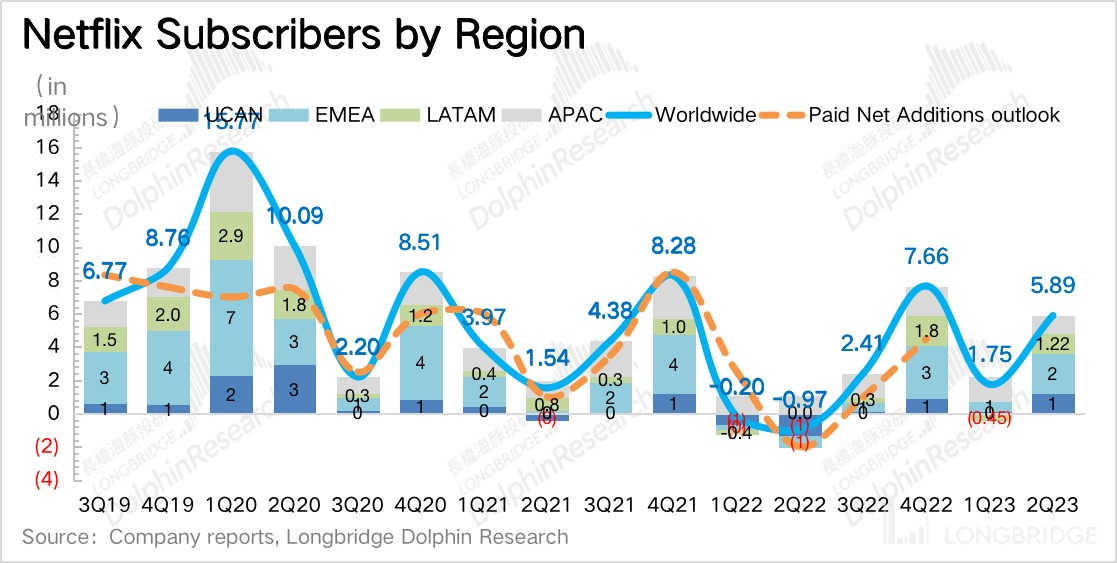

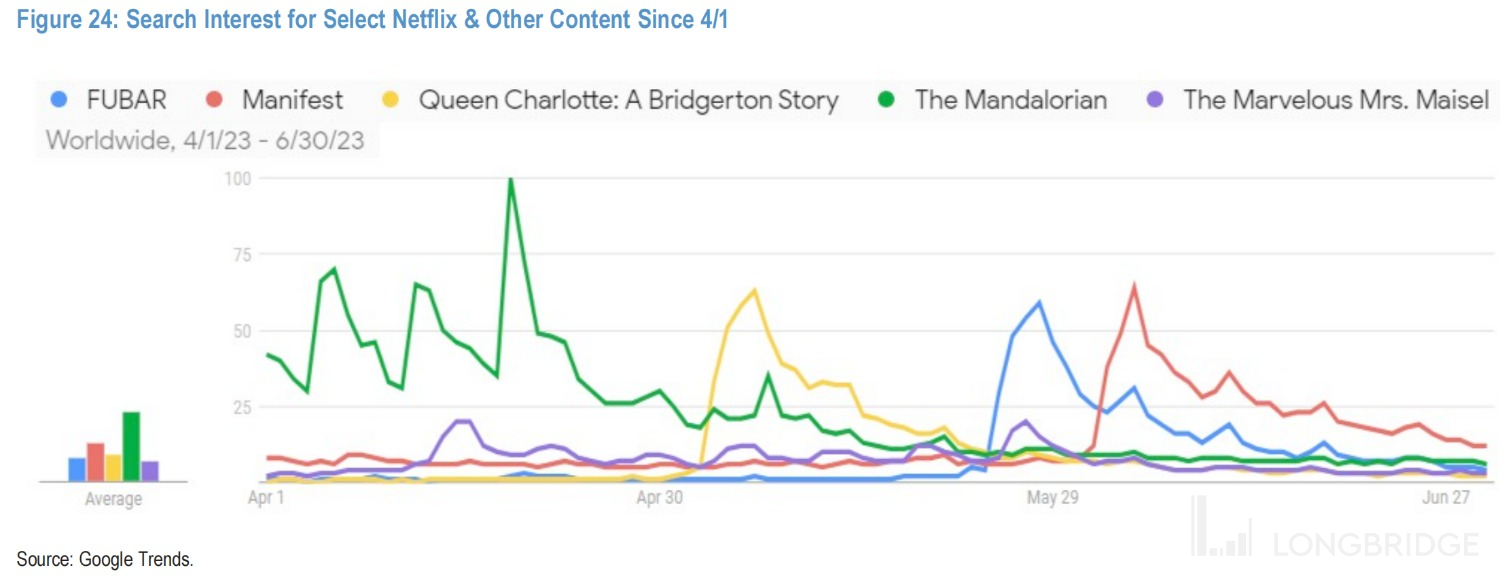

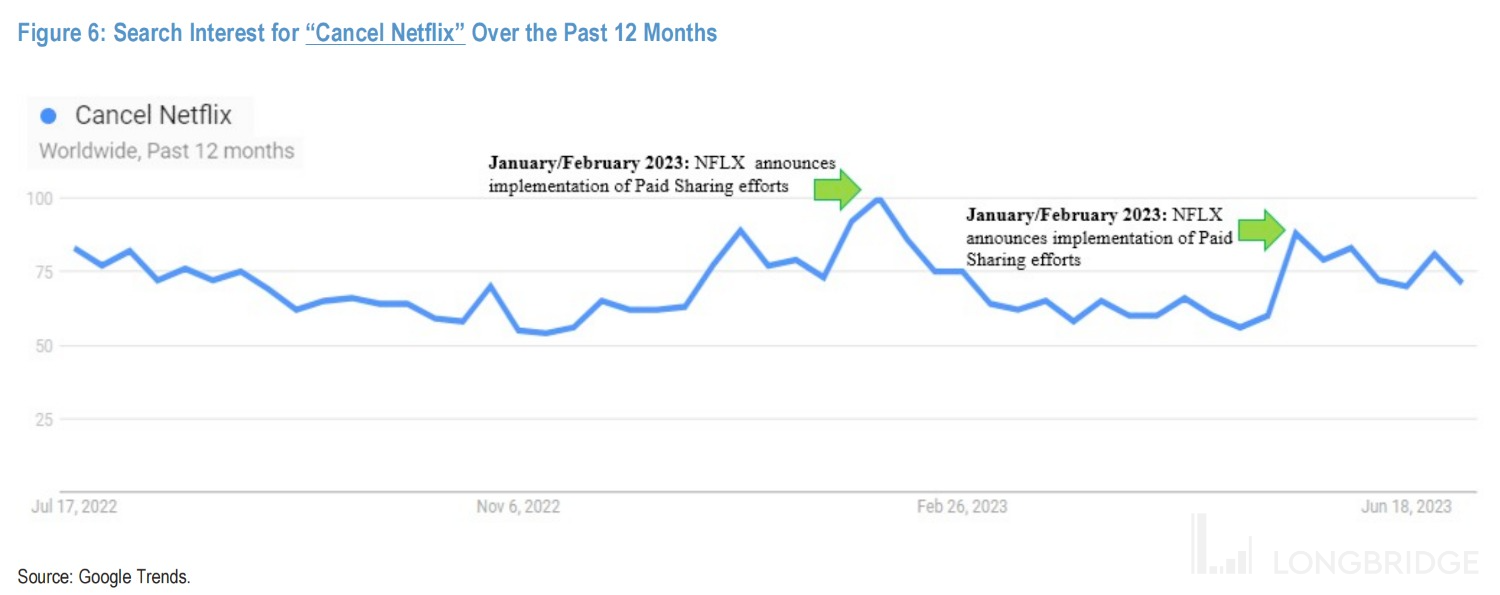

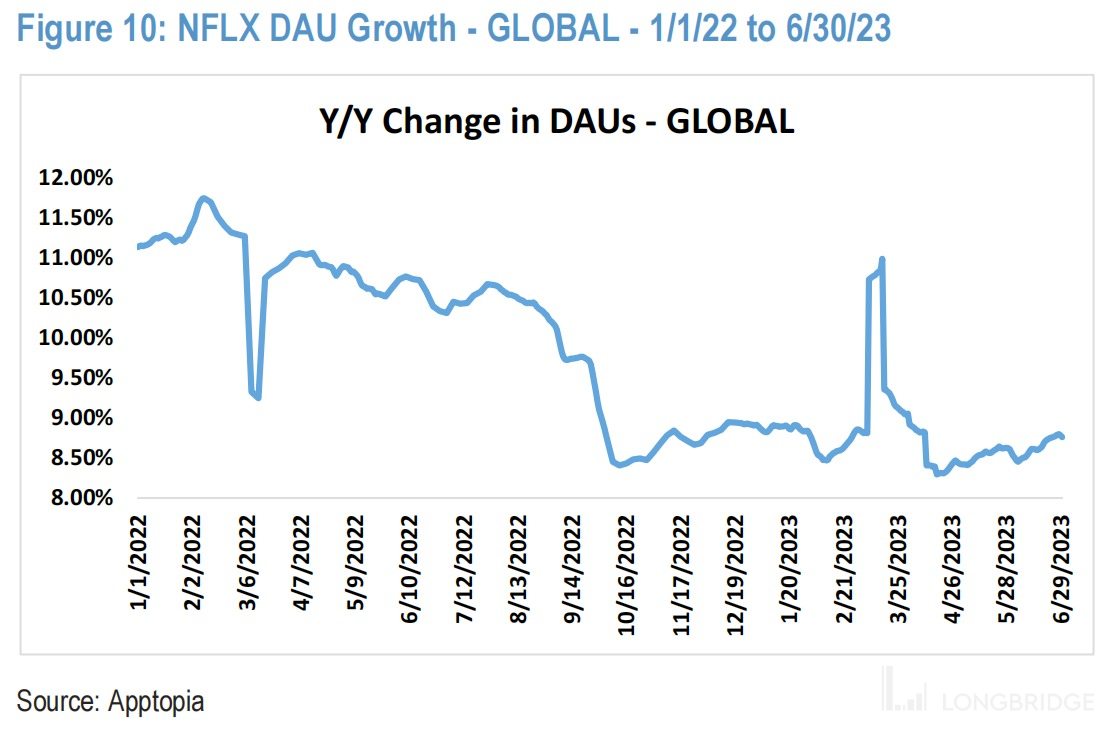

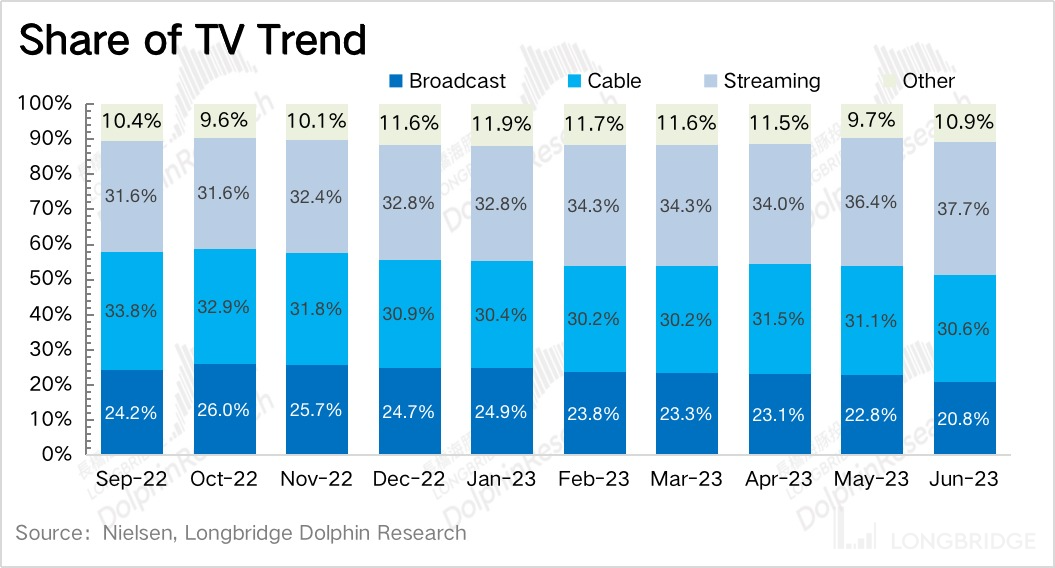

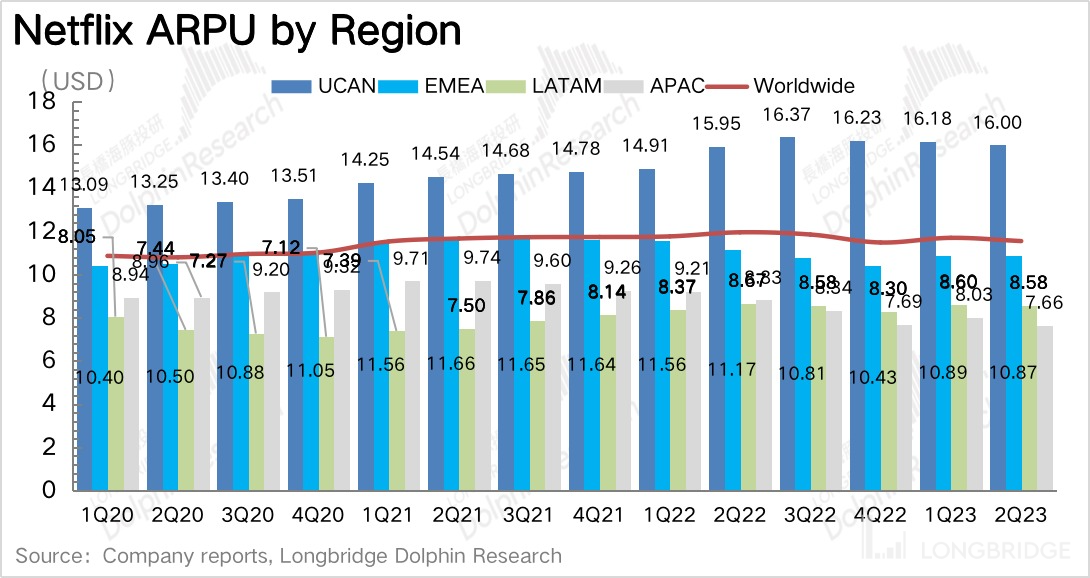

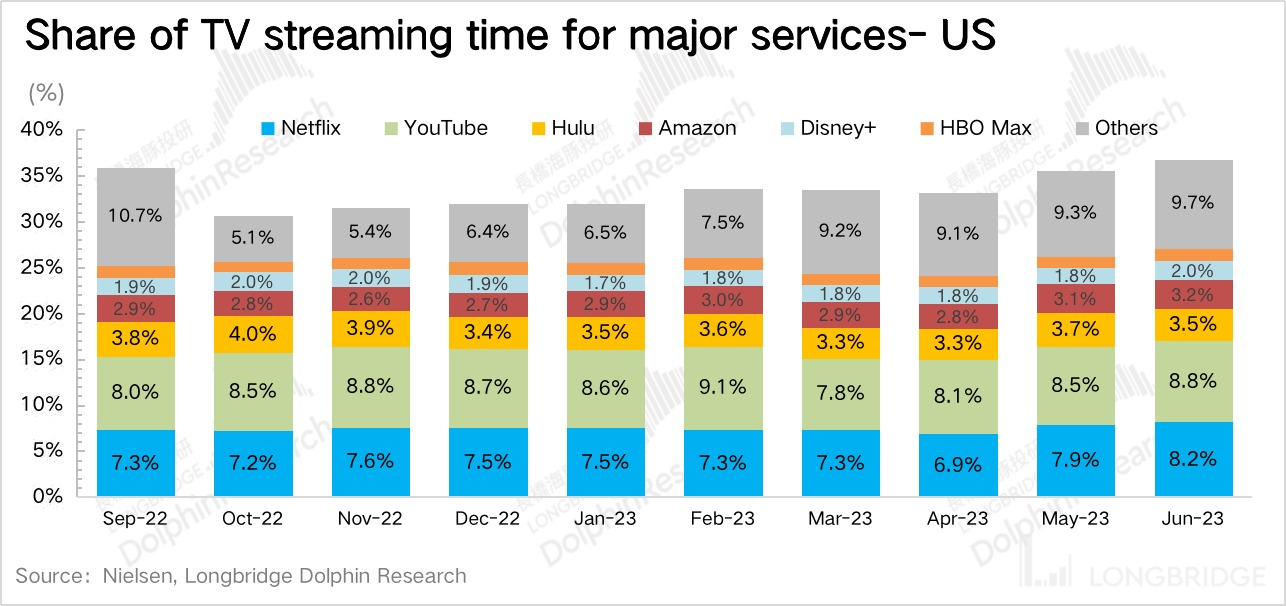

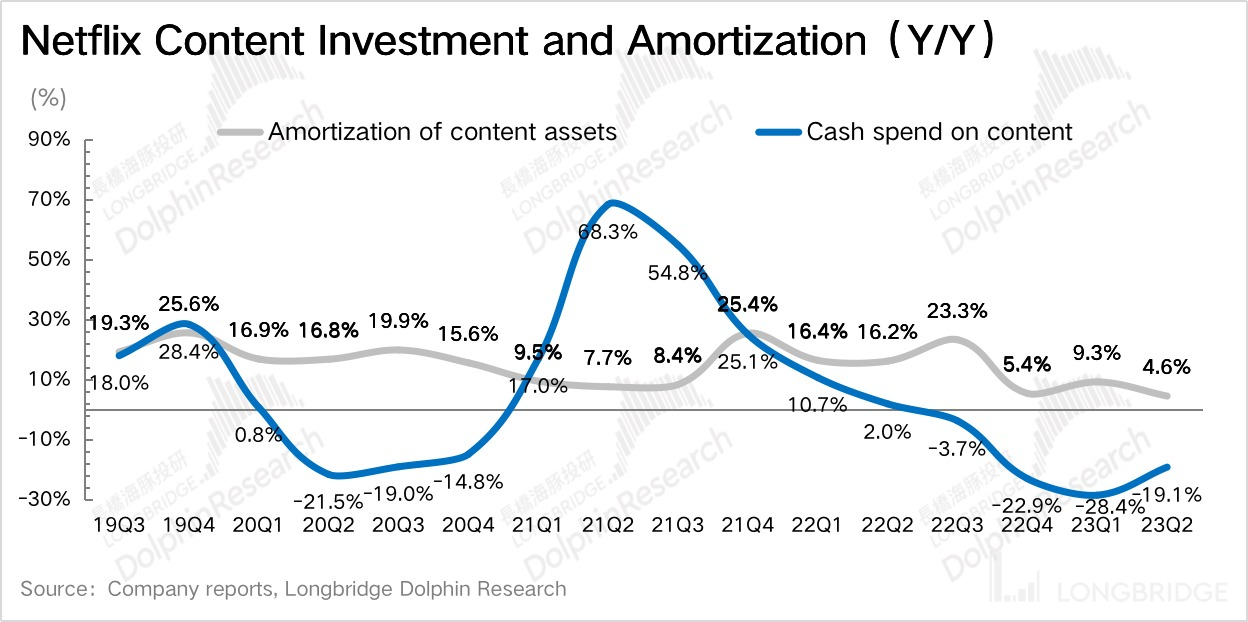

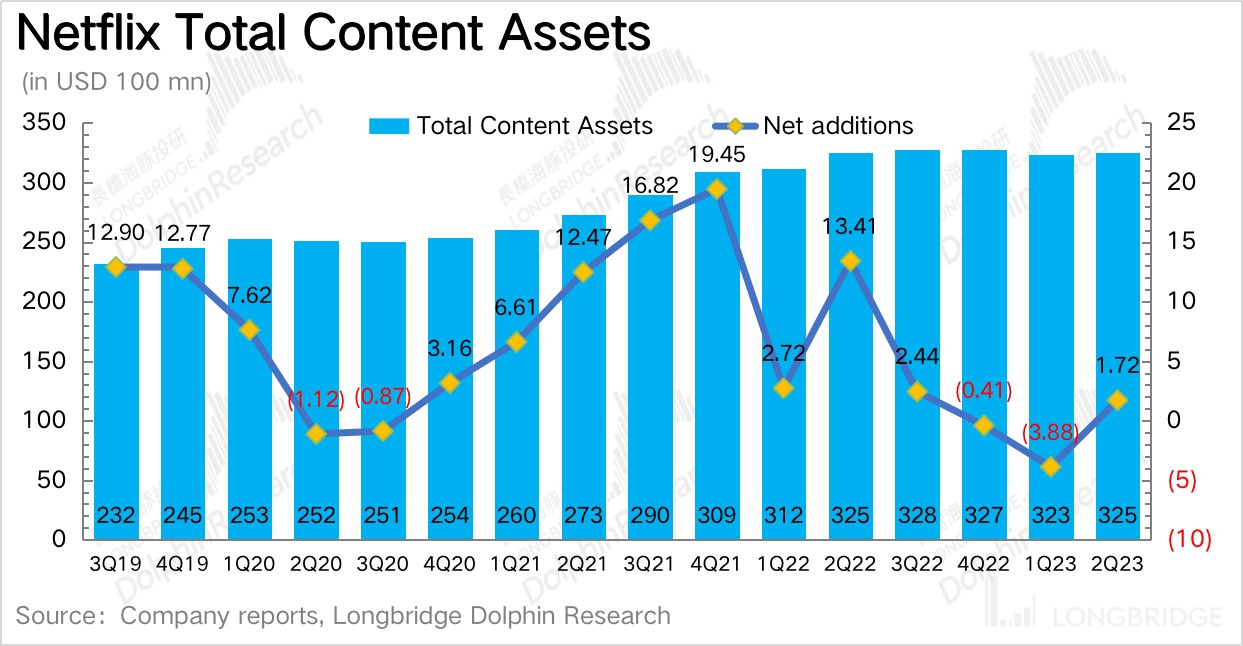

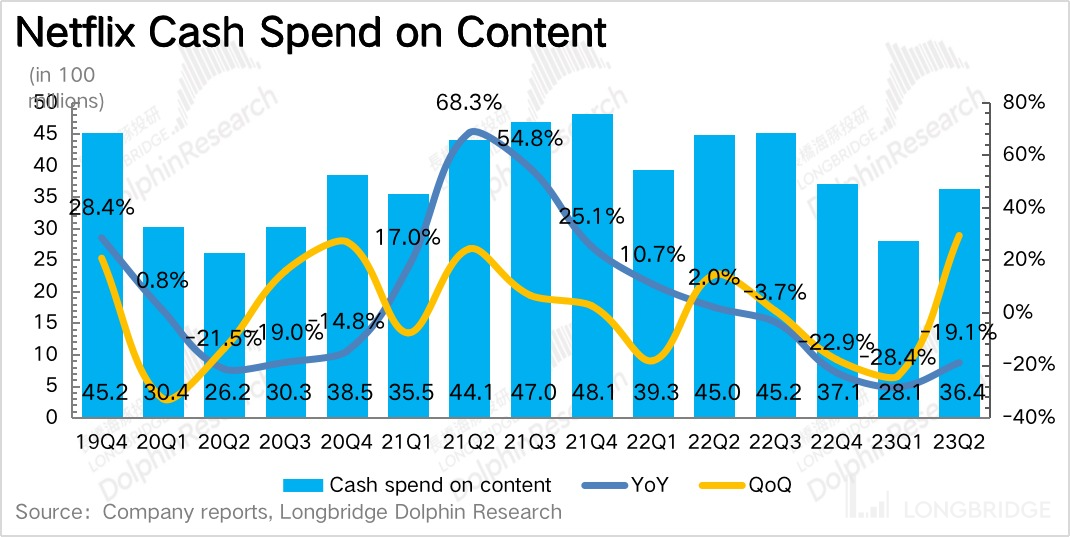

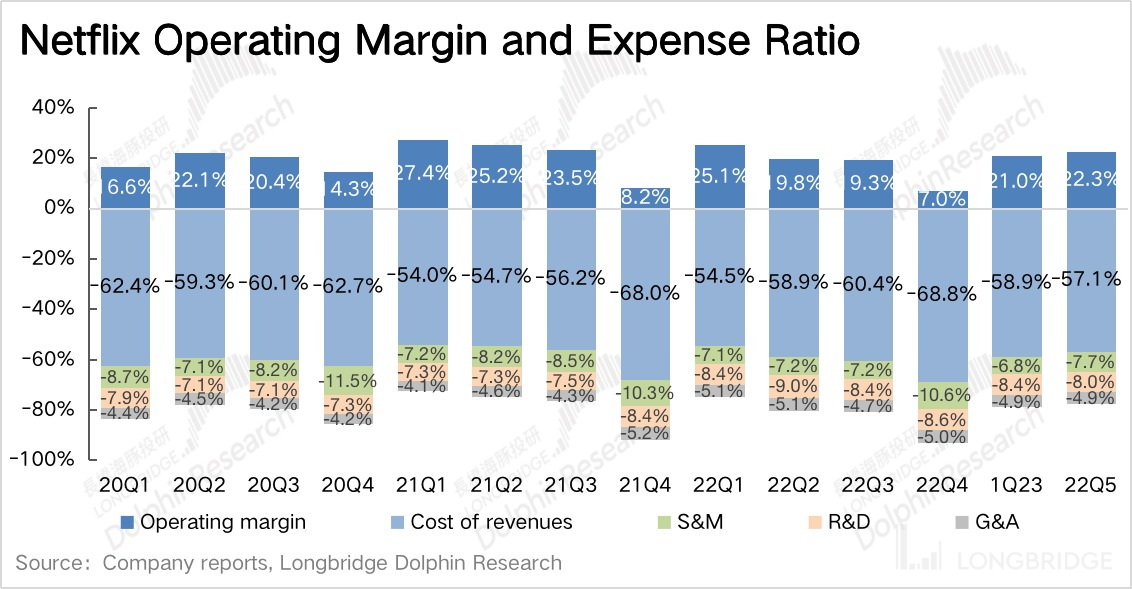

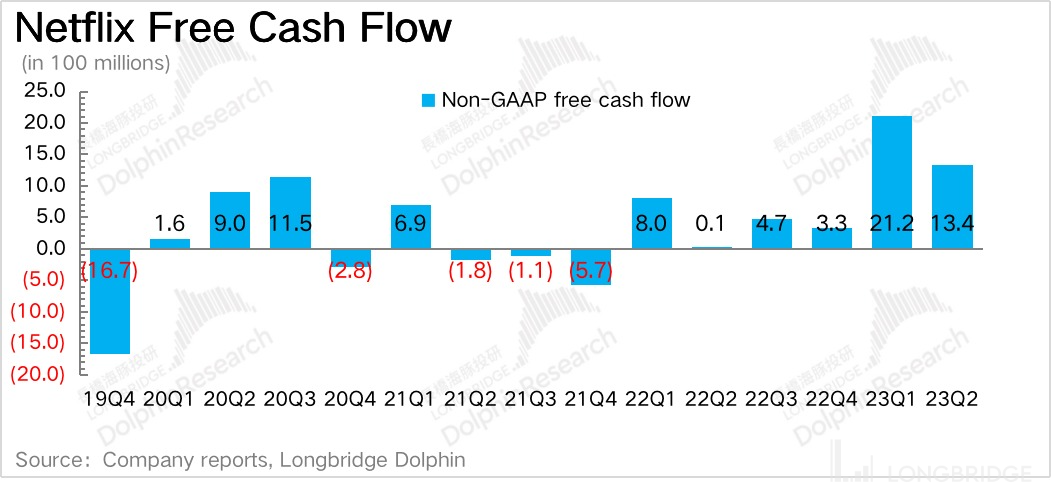

$Netflix(NFLX.US) Beijing time released its 2023 second quarter financial report in the early morning of July 20. The highlight was a larger-than-expected net increase in the number of subscribers under the crackdown on account sharing and the introduction of ad-supported packages. The after-hours decline is mainly due to the gap between the current and next quarter's revenue guidance and expectations. At present, the valuation is higher and the growth expectation is relatively sufficient. Therefore, the market will be more demanding on Netflix's performance at this time. Specifically: 1, Users Exceeded Expectations The net increase in subscribers in the second quarter was 5.89 million, significantly exceeding the market's expected 2 million after the recent increase. The increase in users is mainly due to the launch of the business strategy to combat account sharing in more than 100 countries around the world. In the second half of the year, Netflix will continue to promote this strategy in the remaining countries and regions. At present, Dolphin Jun thinks that the impact of this account sharing is very good. First of all, the second quarter is not the streaming season in the traditional sense, and the content broadcast by Naifei in that season is not particularly popular. In the second quarter report, the company also mentioned that some users resisted unsubscribing because of restrictions on account sharing. But still because the Netflix's content advantage is tough, the loss of users will soon return. No specific user guidelines were given in the third quarter, but management stated that Q3 and Q2 net additions were similar. If the 6 million forecast exceeds the original market expectation 5.38 million (BBG), some institutions may be more optimistic (+600~7 million). However, the management also mentioned that it will stop providing the basic package of US $9.99 for new users in North America and make corresponding price increases in other regions, which may also make the market worry about the weak growth of subsequent users. * * 2, revenue is a bit inferior * * In the second quarter, Netflix's total revenue reached 8.19 billion US dollars, up 2.7 percent year-on-year. The revenue guidance for the next quarter is 8.52 billion, with a year-on-year growth rate of 7.5, which is also lower than the market's expected 8.67 billion. Although the increase in users significantly exceeded expectations, why is revenue not as high as market estimates? Dolphin Jun believes that there are three main reasons: (1) Most of the net increase in users is mainly due to the increase in subscriptions after the May 23 crackdown on account sharing action, paid less than 3 months, revenue contribution is not much as market expectations, but also pulled down the monthly per capita payment amount ARM. (2) In the implementation of the strategy to combat account sharing, Naifei suspended the progress of price increases. (3) Advertising revenue is much less than market expectations and cannot make up for the gap caused by the above two factors for the time being. 3, research and development, administrative costs reduced, profit bright eye In the second quarter, Nai Fei in the cost of the overall is more restrained, especially reflected in the research and development, administrative costs, year-on-year decline, significantly less than the market expected to spend. Sales expenses increased by 9% year-on-year due to the introduction of content broadcast, account sharing strategy and advertising package, which is also expected. This, coupled with the nearly 2pct gross margin repair, resulted in an operating profit of $1.83 billion, up 16% year-on-year and significantly exceeding market expectations of $1.59 billion. The operating profit margin under GAAP has increased to 22.3 per cent in the second quarter, and the rate of improvement is still much faster than expected. 4, content investment rebound, but mention full-year cash flow target In the last two quarterly earnings reviews, Dolphin Jun mentioned that a new round of content investment cycle is approaching. In terms of year-on-year growth in content spending, an inflection point has begun to emerge in the second quarter. This also resulted in a lower free cash flow 1.34 billion for the second quarter than for the first quarter, with higher net 2.1 billion. However, the current cash flow is still relatively healthy. Even if investment is increased in the second half of the year, it is the peak demand season, so there is no need to worry about the avalanche of cash flow. Despite entering a new content cycle from a growth trend, Netflix still hopes to continue to improve the company's cash flow by adjusting the size of its original content spending, with management raising its full-year free cash flow target from 3.5 billion to 5 billion in the second quarter. As of the end of the second quarter, the net debt (cash assets -long-term and short-term debt) on Naifei's account was 5.9 billion. In the second quarter, the company repurchased 1.8 million shares at a cost of US $0.645 billion million, with 3.4 billion remaining in the repurchase amount. Because the current cash 7.7 billion on the books is significantly higher than the minimum cash size requirement set by the company (two months of revenue, about 5.5 billion), management intends to increase buybacks in the second half of the year. Dolphin View **Naifei's second quarter results are still very good, at least much better than Dolphin Jun's expectations, and higher than most institutions in the market expected. Although there are flaws in the income, we think the problem is not big. In the context of an improving capital environment and increasing competitive trends, it is more important to increase more user penetration than to make short-term efforts to make financial figures on revenue. **** Similarly, we believe that entering a new cycle of content investment should also be viewed positively. The current investment is for the next 1-2 years of content reserves, as long as the content reserves are rich, the dominant position will be more stable. **** However, the main problem with Netflix is valuation. In the long term, Netflix's valuation has not been low. The pull-up in the past month or so is due to market sentiment and the unexpected effect of the recent account sharing blow. Therefore, it is also reflected that the market has instead given more negative feedback (up to now, down 8% after-hours) when the current and guidance revenues have fallen short of expectations. **** In fact, the current U.S. stock growth stocks are more or less suspected of stagflation, short-term does not rule out the risk of a correction. If Netflix can take this opportunity to pull back to around $170 billion ($380, corresponding to 2024e 25xPE), that may be a relatively reasonable valuation level. * *! * * The following are the details * * * The 1. crackdown on account sharing worked, and the increase in users exceeded expectations * * The net increase in subscribers in the second quarter was 5.89 million, significantly exceeding the expected 2 million after the market had recently increased. The increase in users was mainly due to the launch of the business strategy to combat account sharing in more than 100 countries around the world in May, and the management announced that it would continue to promote this strategy in the remaining countries and regions in the second half of the year. By region, the second quarter of the regional increase in the number of people distribution is relatively balanced, the increase in Europe and the United States is significantly higher.! There are also many high-quality films broadcast on the content, which also play a certain role in the growth of users. For example, "The Mandalorian" and "Queen Charlotte" began to broadcast in the third season of "The Withcher" at the end of June, continuing the popularity of the previous two seasons and receiving the highest ratings on the Netflix platform at the current time.! For now, Dolphin Jun thinks that the impact of this account sharing is very good. First of all, the second quarter is not the streaming season in the traditional sense, and the content broadcast by Naifei in that season is not particularly popular. In the second quarter report, the company also mentioned that some users resisted unsubscribing because of restrictions on account sharing. However, it is still because the Netflix content advantage is tough, and the lost users will soon return.! ! No specific user guidance was given in the third quarter, but management stated that Q3 and Q2 net increments were similar. If the 6 million forecast exceeds the original market expectation 5.38 million (BBG), some institutions may be more optimistic (+600~7 million). Judging from the Apptopia third-party data, at the end of the second quarter, the trend of user growth was more obvious. Therefore, Dolphin Jun is relatively optimistic about the user growth in the second half of the year.! Medium Confidence Description in Chart Has Been Automatically Generated The medium-and long-term growth logic that Naifei's management has been explaining-streaming media replaces traditional cable TV demand. Judging from the Nielsen data, this logical trend has been continuing and has accelerated further since May.! Chart, bar chart description has been automatically generated * * 2. to suspend price increases, advertising performance is generally difficult to make up for in the short term * * revenue of $8.187 billion in the second quarter, up 2.7 percent year-on-year, exchange rate impact has been significantly weakened. In terms of business segments, streaming media revenue (subscription + advertising) was $8.16 billion, up 2.8 percent year-on-year, mainly driven by user growth; DVD sales continued to decline 21 percent as expected, and the company expects to shut down the business completely by the end of the third quarter of this year. In the second quarter, in order to reduce short-term user resistance, Nafta did not continue to raise the price of membership fees in the second quarter because Nafta began to promote account sharing restrictions in large countries and regions around the world. Coupled with the large-scale price reduction in low-income areas in the first quarter, many new users who started subscribing to members after May lowered the overall level in the second quarter when calculating the average monthly payment amount ARM. At the same time, after the launch of the advertising package, the advertising revenue is not amazing at present, and it can not make a significant enough contribution to the overall revenue, so it can not make up for the above gap.! Schedule Description Automatically Generated However, Naifei's management announced that it would stop providing basic accounts of US $9.99 to new users in North America. With the weakening of the impact of account sharing restrictions, the arrival of the content peak season and the more mature advertising business, ARM is expected to recover to flat year-on-year or resume growth in the second half of the year.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

- streaming media competition: competition continues, the advantages are not reduced * * streaming media internal and external competition has always existed, but because of the pressure of the general environment, some catch-up parties/new entrants for this loss-making business, short-term business strategy has been adjusted. For example, peer-to-peer cooperation (Paramount and Showtime), reducing investment and increasing external content licensing (Disney). Of course, there is no shortage of rich and powerful warriors (Amazon Prime) who continue to fight high. Dolphin Jun believes that the competition margin has slowed slightly in the past six months, mainly from the pressure of the capital market, and the streaming media giant has reduced some content investment. Of course, outside the industry, streaming media is more in the bonus period of increased penetration. Still from the Nielsen data, Netflix's share of streaming media fell to 6.9 per cent in April, when the content was flat than before. After the account sharing limit in May, the platform's viewing share jumped to 7.9 percent and continued to rise to 8.2 percent in June.! Schedule Medium Credibility Description Automatically Generated 4. entered a new investment cycle, but spending targets are still down Dolphin Jun has repeatedly mentioned in his earnings reviews over the past few quarters that Netflix's content amortization has been increasing, but content investment is declining at an accelerated pace. When the size of content assets began to turn negative on a year-over-year basis last quarter, it means that Nifty's content investments may have to bottom out. In the second quarter, content investment expenditure 3.64 billion, down 19% year-on-year. This downward trend no longer expands. At the end of the second quarter, the scale of content assets also showed a net increase from the previous quarter. To a certain extent, it can be said that the next content investment of Netflix will rebound quarter by quarter, which means that a new round of content investment cycle has begun.! Graphic Description Generated Automatically! Chart, bar chart, histogram description has been automatically generated However, due to the management's demand for profit and cash flow improvement, Naifei is also lowering its investment budget under the aggressive investment of peers in the first two years. Therefore, the absolute value of subsequent re-content expenditure is unlikely to increase significantly in the first two years.! Chart, Histogram Description Automatically Generated * * 5. Slowing Down Team Expansion, Releasing Exceeding Expected Profits * * Cost and Expenses in the Second Quarter were Optimized Ring-on-Ring, Gross Profit Rate Increased from 41.1 to 42.9 of Q1, Operating Profit Rate Increased from 21% of Q1 to 22.3.! The picture includes a schedule description that has been automatically generated Generally speaking, the second quarter will be warmed up before the content peak season in the second half of the year. However, because the second quarter itself is a low season, if there is no particularly hot content, the revenue performance will be relatively flat, so the operating profit margin in the second quarter will generally be slightly lower than that in the first quarter. However, in the second quarter, Naifei optimized costs by slowing down the recruitment of personnel and other cost management means, while also controlling the research and development costs, management expense rate. However, it may be due to the promotion of account sharing restrictions, advertising packages and other actions, marketing investment has increased. The company's operating margin target for 2023 remains unchanged, still in the 18% to 20% range. Combined with the reduction in content spending, it is expected to release more free cash flow in the second half of the year than last year, so the company also raised its 2023 free cash flow target from 3.5 billion to 5 billion. As a result, Netflix may have a lot more cash on its books, but management insists on maintaining a minimum cash size of 2 months for normal operations, and the excess is intended to be fed back to shareholders in a buyback.! Schedule description has been automatically generated Long Bridge Dolphin Investment Research" Netflix "History Article Earnings Season April 19, 2023 Call "Focus on Talking about the Prospect of Advertising and Account Payment Sharing (Netfllix 1Q23 Call Minutes)" April 19, 2023 Earnings Review "Bai Piao Party Difficult to Fight, the familiar Naifei" flies "motionless" January 20, 2023 telephone conference "Top-level changes do not hinder content strategy, advertising revenue target is more than 10% (Naifei 4Q22 telephone conference minutes)" January 20, 2023 financial report review "Explosions Drama Save Advertising, naifei Perfect Interpretation of" Content First "" Call on October 19, 2022 "Naifei: In addition to advertising, next year will also focus on cracking down on account sharing (3Q22 Call Record" Financial Review on October 19, 2022 "Naifei: Another Surge Against the Trend, good content is the real" good medicine "" July 20, 2022 teleconference "advertising model is a new story Netflix the future (phone minutes)" July 20, 2022 financial report review "Naifei: performance did not release thunder, but carnival is not necessary" April 20, 2022 teleconference "focus on how to make big revenue, actual" exposure "lack of confidence in user growth (Netflix call minutes)" April 20, 2022 earnings review "overnight plunge of 25%, naifei Logic Collapses" January 21, 2022 Call "Management Says Poor Guidance Expectations Due to Forecast Uncertainty from Epidemic (Minutes of Naifei's Fourth Earnings Call)" January 21, 2022 Earnings Review "Plunging 20%? Naifei Becomes a Copy of Aiqiyi" Call on October 20, 2021 "Ambitious, Naifei's Next Goal is to Learn" Disney "(Minutes of Third Quarter Call)" Financial Report Review on October 20, 2021 "Naifei: Streaming Media Boss Comes Back, Is It Accidental or Destined?" July 21, 2021 Call "Minutes of Nye's Second Quarter Call" July 21, 2021 Earnings Review "Guidance Remains Conservative, When Will Nye, the King of the Post-Epidemic Period, Return? | Dolphin Investment Research" April 21, 2021 Call "Netflix First Quarter Call Q & A: Take a Look at Management's Answers to User Growth Questions" April 21, 2021 Earnings Review "After the End of the Epidemic Bonus Period, the growth of Naifei's users has collapsed a bit * * Depth * * February 16, 2022 Depth" Consumer Internet "King" Controversy, Meta, Google, Naifei Fight bayonets "November 23, 2021 Depth" Long Video Melee to Come "American Reproduction", Naifei and Disney are miserable? Dolphin Investment Research Disclaimer and General Disclosures

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.