NVIDIA: Exploding Once Again, the "One-Man Show" of AI Kings

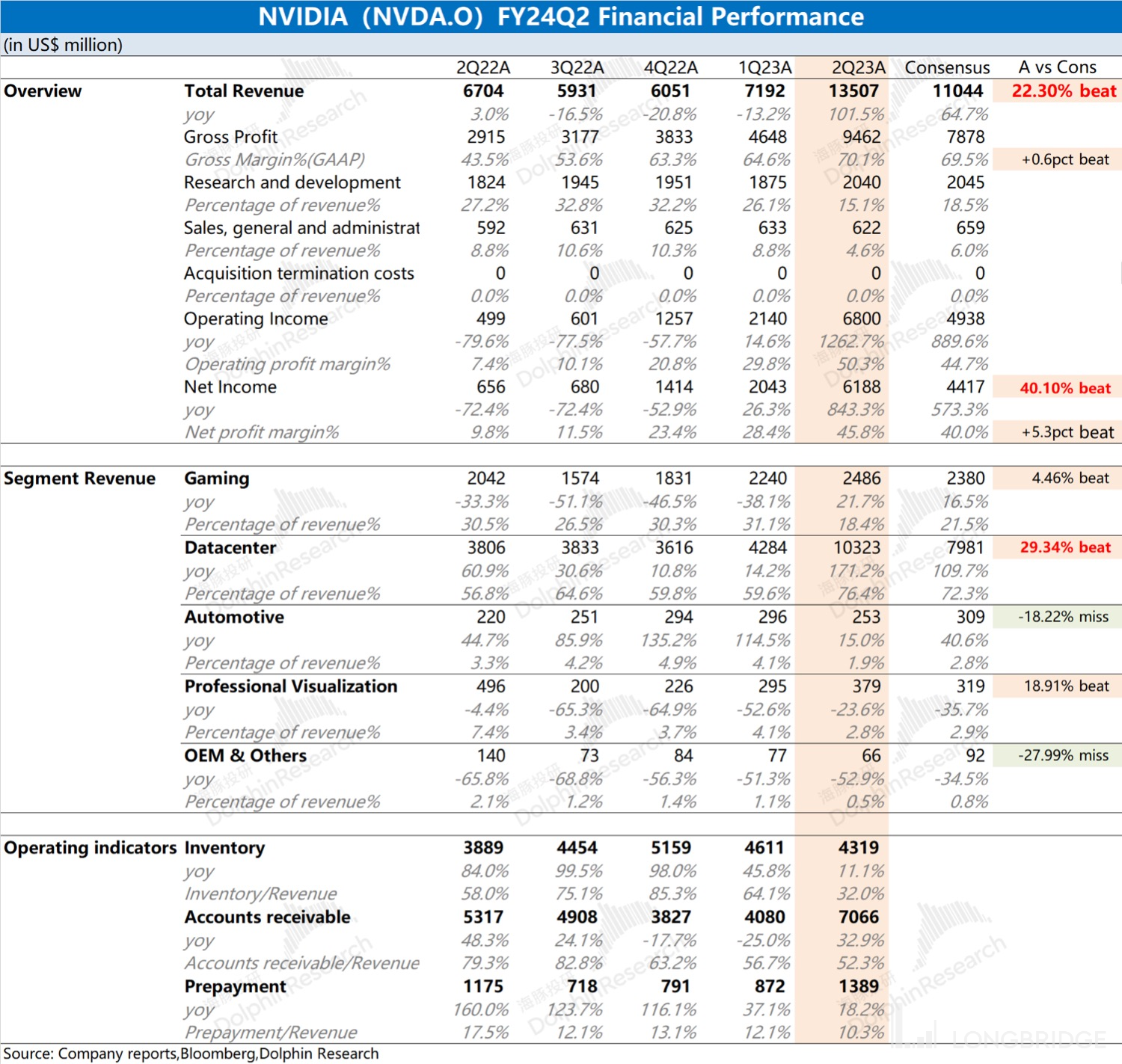

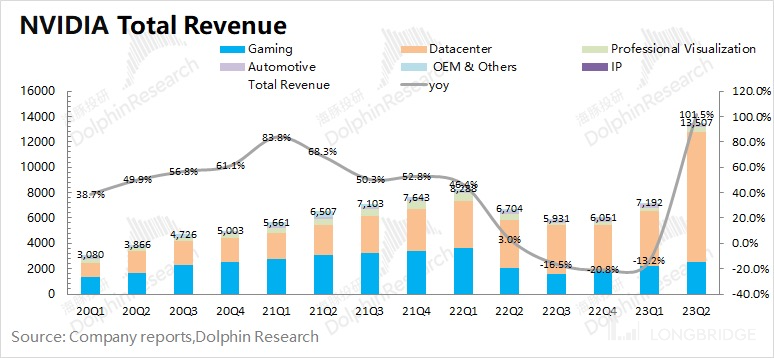

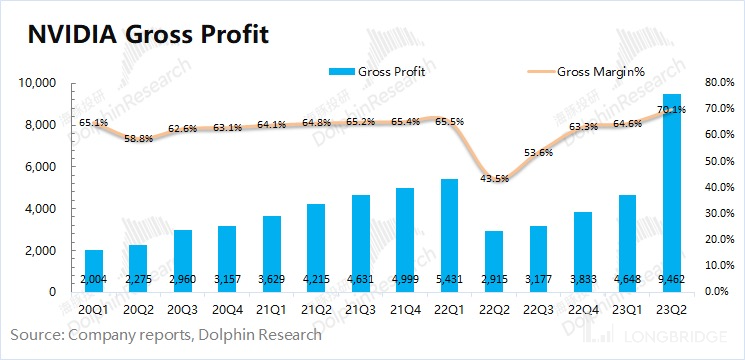

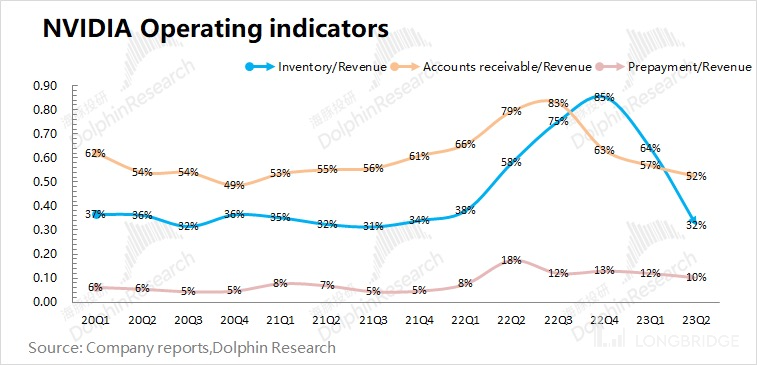

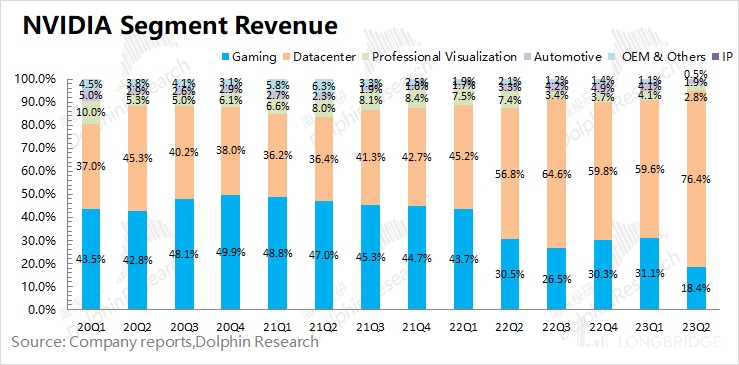

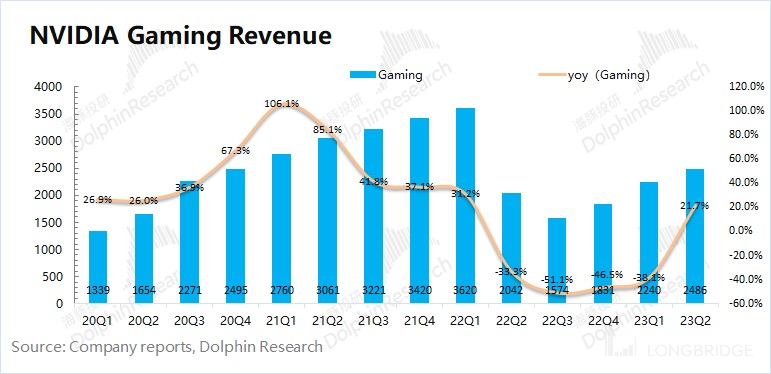

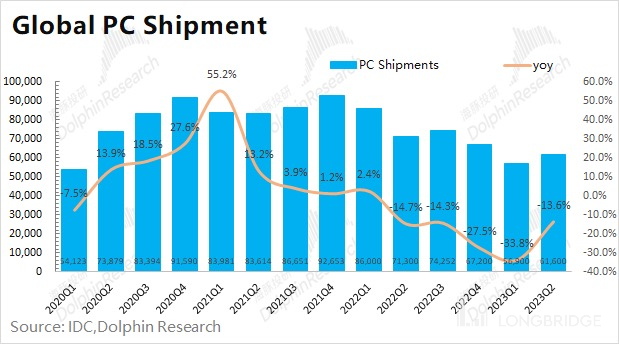

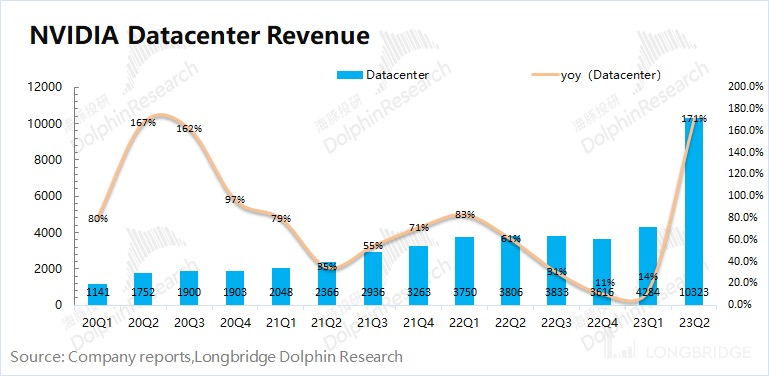

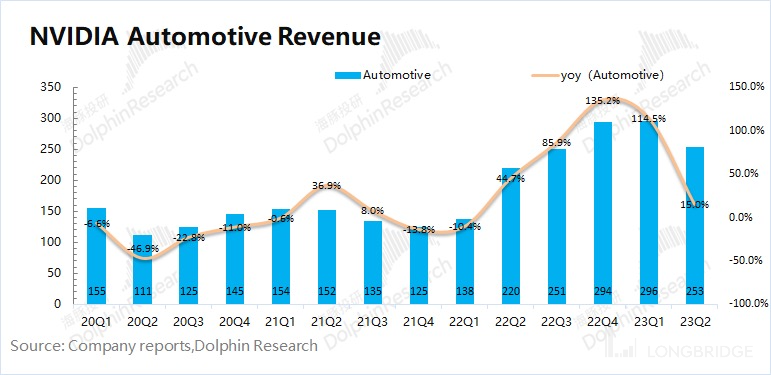

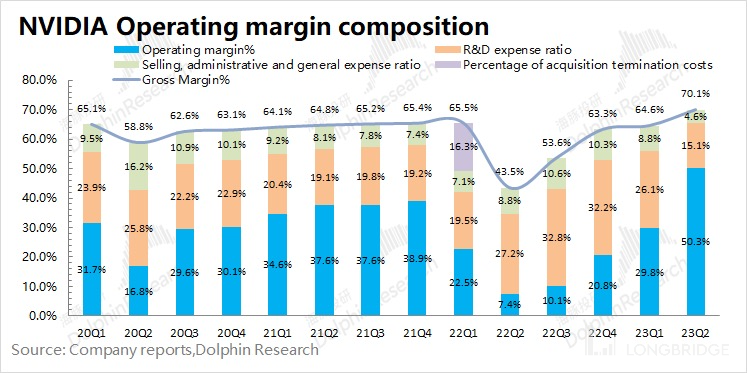

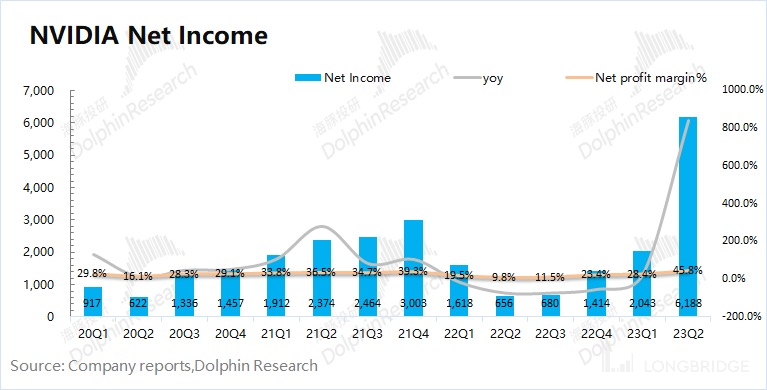

Nvidia (NVD$Agilent Tech(A.US)) In the early morning of August 24, Beijing time, U.S. stocks released after-hours financial results for the second quarter of fiscal year 2024 (as of July 2023): * * 1. Overall performance: revenue & gross profit margin, both exceeding expectations * *. This quarter $NVIDIA(NVDA.US) achieved revenue of $13.507 billion, up 101.5 percent year-over-year,. **NVIDIA Achieved Gross Margin (GAAP) 70.1% for the quarter * *, * *. **Gross margin is at an all-time high, mainly due to the current" supply exceeds demand "on the product side * *. The net profit for this earnings report was $6.188 billion, up 843.3 percent year-over-year, **and the profit side is also at an all-time high * *. * * * * 2, core business situation: "hard core" data center. * * Game business and data center business accounted for nearly 95% of the company's revenue, the game business began to pick up, and data center performance "burst". * * 1) The game business grew 21.7 year-on-year in this quarter and continued to show a recovery trend * *. * * Dolphin Jun believes that the main reasons for the recovery of the company's game business this quarter are: a) there is a certain demand for replenishment in the PC market, which has also increased the demand for GPU to a certain extent; B) this quarter <span class =" security-tag "type =" security-tag "counter_id =" ST/US/AMD "name =" AMD "trend =" ">$$AMD(AMD.US) the game business dropped month on month, while Avida continued to pick up, and the current market demand for Avida alone is relatively good * *; * * 2) Data center business grew 171 percent year-over-year in the quarter * *, although the total capital expenditure of large U.S. factories decreased in the quarter, which did not affect the demand for Nvidia's AI. **3. Key financial indicators: cost rates are at historically low levels. * * Nvidia's operating expense rate fell to a historical low of less than 20% in the quarter. This is mainly due to a surge in the revenue side, which has significantly reduced the share of the expense side. And in the inventory side has been significantly improved, *the company's inventory continued to decrease by nearly $0.3 billion this quarter, inventory indicators began to move towards" in short supply " *. * * 4. Guidance for the Next Quarter * *: * * Avida expects revenue of US $16 billion (plus or minus 2%) in the third quarter, up 170 year on year, exceeding market expectations of US $12.5 billion. Gross profit margin in the third quarter was 71.5 (plus or minus 0.5), which also exceeded market expectations by 69.95, reaching another record high * *.! **Overall view: Nvidia once again beat expectations * *. The two core indicators of revenue and gross margin in the quarter clearly exceeded market expectations, mainly due to the burst performance of the data center business. In addition, **the Company's inventory continued to decline by $0.3 billion during the quarter * *. *With higher revenues and lower inventories, Nvidia is already" a standout " *. **What is more explosive than the earnings data is the company's guidance * *. * * Nvidia handed over a horrible $16 billion and 71.5 percent guidance for next quarter's revenue and gross margin, * *. Revenue for the next quarter was $16 billion, up 170 percent year-on-year, while gross margin for the next quarter was 71.5 percent, up 17.9pct, * *. For such an over-expected guidance for the third quarter, Dolphin Jun believes that the PC and gaming businesses are beginning to pick up, and the main over-expectation is still the surge in demand for AI and big language models * *. In the case of relatively weak data in the second quarter of most technology stocks in the United States, Nvidia showed a "win-win" situation. **This shows that the market still has a strong demand for data center business, and Nvidia has an absolute leading position in the market. **** Nvidia's "burst" results are expected to continue to boost the company's share price in the short term. However, as the market has given the company high growth expectations, the stock price also needs to be supported and maintained by each "over-expected performance. **Combined with next quarter's guidance, Dolphin Jun expects the company's profits to continue to improve, but the quarter-on-quarter growth is smaller than this quarter. * * This time the results "opened up" and saw a certain increase (6.58 per cent) after the session, but the increase was far less than the increase (20 per cent +) at the time of the last results announcement. This is mainly because although the performance is good, it can bring short-term upward performance. However, as the company itself enjoys the valuation brought about by high expectations, "higher growth" also requires "stronger performance". * * Dolphin Jun's specific analysis of Avida's financial report is detailed below: * * 1. core performance indicators: revenue & gross profit margin, both exceeding expectations * * * 1.1 operating income *: * * Avida achieved revenue of US $13.507 billion in the second quarter of fiscal year 2024, up 101.5 year-on-year, exceeding previous company guidelines (US $11.044 billion) * *. The company's revenue "doubled" in the quarter, mainly due to strong demand from its downstream data center business.. *NVIDIA expects 3Q revenue of $16 billion (plus or minus 2%) *,. The continued explosion of the data center business also means that the AI era may not be far away.! * * 1.2 Gross Margin (GAAP): NVIDIA achieved a gross margin (GAAP) of 70.1 percent in the second quarter of fiscal year 2024, * * * *, a record high gross margin for the quarter. * * The company's previous sharp drop in gross profit margin was mainly due to the company's inventory write-down. When gross margin returns to 63%-64%, inventory is no longer a problem. * * Combined with the company's inventory situation, Nvidia's inventory continued to decline this quarter, falling to $4.32 billion, and Nvidia's products began to show a "short supply" situation * *. * * Nvidia's gross profit margin in the third quarter is expected to return to 71.5 (plus or minus 0.5), exceeding market expectations (69.95), and the company's gross profit margin in the third quarter is also expected to reach a new high. * *! * * 1.3 Operating Indicators * * * 1) Inventory/Revenue: This quarter's ratio was 32%, down 32pct **from the previous quarter * *. 2) Accounts receivable/revenue: 52% in the quarter, down 5pct from the previous quarter * *. The proportion of accounts receivable decreased, and the company's collection situation continued to improve.! * * 2. Core Business: "Hard Core" Data Center * * * Driven by AI and other demands, NVIDIA's data center business continued to expand its share of formula revenue in the second quarter of fiscal year 2024, reaching 76.4 per cent * *. Although the game business has risen steadily this quarter, the proportion is still compressed to less than 20% by the fast-growing data center. **, the combined income of the two accounts for nearly 95%. * *! * * 2.1 Game Business: NVIDIA Game Business Realized Revenue of US $2.486 billion in the Second Quarter of Fiscal Year 2024, * * * *. **After several quarters of downturn, the game business has picked up and returned to positive growth for the first time.! According to IDC's latest data, the global PC market shipped 61.6 million units in the second quarter of 2023,. Although there is still a decline, but the decline is better than the previous two quarters, which is mainly the current PC market replenishment demand began to pick up;! **2.2 Data Center Business: NVIDIA's data center business achieved revenue of $10.323 billion billion in the second quarter of fiscal year 2024, up 171 percent year-over-year. * * Nvidia's data center business reached a new high this quarter, mainly due to strong demand for generating AI and large language models.! $Amazon(AMZN.US)$Microsoft(MSFT.US)$Alphabet(GOOGL.US)$Meta Platforms(META.US)$Apple(AAPL.US) **Decline in Total Capex, It did not affect Nvidia's data center business. This is mainly due to the contraction of non-AI related expenditures by various manufacturers, while the AI demand for Avida A100 and H100 has not decreased. For the company's strong revenue guidance of $16 billion for the next quarter, Dolphin Jun believes this is still primarily due to continued volume growth in data center demand * *. In the next quarter, NVIDIA's data center business is expected to stand firm at 10 billion revenue. * * 2.3 Automotive Business * : * * In the second quarter of fiscal year 2024, NVIDIA's automotive business achieved revenue of US $0.253 billion billion, up 15% year-on-year. These increases were mainly due to revenue from autonomous driving and artificial intelligence cockpit solutions. * * * * Although the company's automobile business has declined to a certain extent from the previous month, it currently accounts for a small proportion of revenue (less than 5%) *. The current performance of Nvidia is mainly focused on the performance of the data center and gaming business.! * * 3. Key Financial Indicators: Expense Rate Enters Historically Low * * * 3.1 Operating Margin * * * * NVIDIA Operating Margin Rebound to 50.3% in Q2 of FY2024 * *, * * Closes to Reasonable Range * *. **The recovery in operating margins in the quarter was primarily due to the dual impact of higher gross margins and lower expense ratios. * * From the composition of operating profit margin, the specific changes: * * "operating profit margin = gross profit margin -research and development expense ratio -sales, administrative and other expenses accounted for" * * * 1) gross profit margin: 70.1 * *, this quarter * *,. After the gross margin returned to the normal range, the shortage of some products drove the company's gross margin to continue to rise * *,. The absolute value of the company's research and development expenditure has increased, but due to the surge in revenue, the expense rate has decreased significantly * *,. Under the current "supply exceeds demand" situation, the company's sales expense rate has entered a historical low. **The value of the company's operating expense guidance for the third quarter continues to rise to $2.95 billion, but the operating expense rate is expected to remain low at around 18.4 percent in the third quarter compared to the growth on the revenue side. The rapid growth of the revenue side directly continues to reduce the cost rate. * *! * * 3.2 Net Profit (GAAP) Rate * * * * In the second quarter of fiscal year 2024, NVIDIA's net profit was US $6.188 billion billion, up 843.3 percent year-on-year, and the net profit margin for the quarter soared to 45.8 percent. * * This quarter, the company's revenue side doubled year-on-year and gross profit margin reached a record high. The operating expense rate fell to an all-time low, directly driving a significant increase in profit.! Dolphin Investment Research on History of NVIDIA Retrospect: Depth June 6, 2022 "U.S. Stock Shock, Are Apple, Tesla, NVIDIA Killed by Wrong?" February 28, 2022 "Nvidia: High Growth Is Not False, Cost Performance or Almost Mean" December 6, 2021 "Nvidia: Valuation Can't Only Rely on Imagination" September 16, 2021 "Nvidia (Part I): How Did Five Years and Twenty Times Chip Daniel Be Tempered?" September 28, 2021 "NVIDIA (Part II): No more two-wheel drive, Davis double kill?" * * Earnings Season * * May 25, 2023 Call "Out of the Low, Embrace AI Era (Avida FY24Q1 Call)" May 25, 2023 Earnings Review "Exploding Avida: AI New Era, Future Has Come" February 23, 2023 Call "Performance Bottom Will Pick Up, AI is the new focus (Avida FY23Q4 call)" February 23, 2023 financial report review "survive the cycle, and on ChatGPT, Avida faith returns" November 18, 2022 call "continue to rise inventory, can it be digested in the next quarter? (NVIDIA FY2023Q3 Call)" November 18, 2022 Earnings Review "NVIDIA: 30% off profit, when will the inflection point come?" August 25, 2022 teleconference "How does management explain the" flash crash "gross margin? (Nvidia FY2023Q2 Call)" Financial Report Review on August 25, 2022 "Nvidia, stuck in quagmire, will it go back to 2018?" August 8, 2022 Performance Forecast Review "Thunder Rolling, NVIDIA Performance Performance" Free Fall "" May 26, 2022 Telephone Conference "Epidemic Overlay Blockade, Game Decline Drags down Second Quarter Performance (NVIDIA Telephone Conference)" May 26, 2022 Financial Report Review "" Epidemic Fat "Is No, nvidia's Performance Is Damped" February 17, 2022 Telephone Conference "Nvidia: Multi-Chip Promotion, Data Center as Company Focus (Minutes of Telephone Conference)" February 17, 2022 Financial Report Review "Nvidia: Hidden Worries Behind Exceeding Expected Performance | Reading Financial Report" November 18, 2021 Telephone Conference "How Does Nvidia Build Yuanuniverse? Management: Focus on Omniverse (NVIDIA Call)" November 18, 2021 Earnings Review "Calculating Power Explodes, Yuan Universe Blessing, NVIDIA Will Keep Down? * * Live * * May 26, 2022" Nvidia Corporation (NVDA.US) First Quarter Results Call for Fiscal Year 2023 "February 17, 2022" Nvidia Corporation (NVDA. US) Fourth Quarter 2021 Results Call "November 18, 2021" NVIDIA (NVDA.US) Third Quarter 2022 Results Call "Risk Disclosure and Statement in this article: Dolphin Investment Research Disclaimer and General Disclosure

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.