Is this overseas "stock and bond rally" too strong and too fast? Without fundamental and technical support?

摩根士丹利認為,美股仍缺乏技術面和基本面的支持,上週大漲主要是受債券收益率下降的影響。目前的行情看起來更像是熊市反彈,並非持續反彈的開始,特別是在更弱的盈利預期和宏觀數據面前。

上週非農點燃加息結束預期,美國股債掀起狂歡,10 年期美債收益率全周累計下降近 26 個基點創一個月新低,美股經歷了年初以來最強勁的周度漲幅。

然而,這場狂歡終究可能又是曇花一現。

摩根士丹利認為,美股仍缺乏技術面和基本面的支持,上週大漲主要是受債券收益率下降的影響。目前的行情看起來更像是熊市反彈,並非持續反彈的開始,特別是在更弱的盈利預期和宏觀數據面前。

而債市大漲主要有兩個原因,一是財政部的長債發行量低於市場預期,二是經濟數據開始顯示增長放緩跡象,讓投資者開始想象美聯儲明年在勞動力市場沒有超預期惡化之前就提前降息。

巴克萊也認為,金融市場可能過於樂觀了,投資者高估了美國勞動力市場的疲軟程度,而通脹凸顯粘性,美聯儲本身還不願意宣佈結束緊縮政策(這點從鮑威爾週五在 IMF 會議上的發言也可以看出)。

摩根士丹利和巴克萊認為,上週的反彈可能會在未來一到兩週內結束,美國經濟勢頭依然強勁,美聯儲不大可能提前降息,另外,中東局勢未見明顯緩和,戰爭升級風險依然存在。

正如華爾街兩大投行預計的那樣,本週美國股債均表現不佳。尤其是鮑威爾放鷹後,美債盤中跳水,標普納指終結兩年最長連漲。

對於結束加息,金融市場可能過於樂觀

摩根士丹利大空頭 Michael Wilson 分析師團隊在週一公佈的報告中表示,上週股市大漲主要是受債券收益率下降的影響,收益率下降主要有兩個原因:

1) 美國財政部發行的長期國債發行量低於市場預期。

2) 經濟數據開始顯示增長放緩跡象。具體來看,製造業和服務業 PMI 均不及預期;勞動力市場數據也顯示進一步放緩,失業率上升。

摩根士丹利認為,這表明經濟增長正在從第三季度的過熱狀態放緩,有助於債券需求增加並帶動收益率下降。

值得一提的是,許多多頭將收益率強勁上漲解讀為美聯儲已經完成加息週期的信號,預測美聯儲明年可能開始降息,即使勞動力市場不繼續惡化,或者出現其他對經濟增長不利的因素。

但摩根士丹利表示,當前的經濟前景顯然不支持美聯儲降息或者每股收益增長大幅加速。巴克萊也警告投資者,不要高估美國經濟的疲軟程度。

根據美國勞工部公佈的數據,美國 10 月非農新增就業人數增加 15 萬人,略低於普遍預期,但這主要是因為前兩個月的新增就業人數被下調 10.1 萬人。

失業率現在已從 1 月低點上升近 0.5 個百分點,每週工作總時長一直處於平穩狀態。

另一方面,如果扣除罷工的影響,過去 3 個月的新增就業人數平均值為 22.3 萬,作為比較,5-7 月的 3 個月平均值為 20.萬,2-4 月為 22.7 萬。

此外,工人在罷工行動中取得勝利,也反映了一個強勁的勞動力市場。

美國汽車工人聯合會(UAW)最近在與底特律三巨頭談判中取得勝利,並計劃聯合豐田、特斯拉和其他未加入工會的美國汽車廠發起組織行動。

巴克萊表示,當前美國經濟仍表現出相當的彈性,超額儲蓄的規模遠遠超出了先前的預期。

上週,金融狀況指數(FCI)有所放鬆,美國成功擺脱了自 3 月以來銀根收緊的影響。市場普遍認為美聯儲相對鴿派,12 月加息的可能性似乎不大,但鮑威爾卻指出,金融狀況的收緊需要持續一段時間才能產生實質影響。

巴克萊表示,美聯儲現在還不願意宣佈結束緊縮週期,而金融市場已經走得太遠,美國經濟仍具有強大的上行動力,不認為美聯儲已經進入寬鬆模式。

北京時間週五凌晨,鮑威爾在國際貨幣基金組織(IMF)的會議上放鷹,稱沒有信心政策已收到足夠緊的程度讓通脹降至 2%,重申保持謹慎,但如果合適,美聯儲將毫不遲疑地加息。

鮑威爾放鷹加上美債標售慘淡,美債盤中跳水,標普納指終結兩年最長連漲。

市場既無基本面、也無技術面支撐

摩根士丹利表示,目前市場仍缺乏技術面和基本面的支持,上週 “股債齊漲” 的行情可能難以為繼。

首先來看美股上市企業的三季度盈利情況。根據摩根士丹利的研報,三季度財報業績好於預期,但企業指引較弱,未來盈利預期被下調,企業目前仍處於盈利衰退階段。

標普 500 指數 7.5% 的盈利明顯高於平均水平(4.5%),這主要是利潤率的彈性帶來的。然而,銷售增速創 2019 年的最低紀錄,這是因為企業的定價能力持續下降,特別是零售商品。

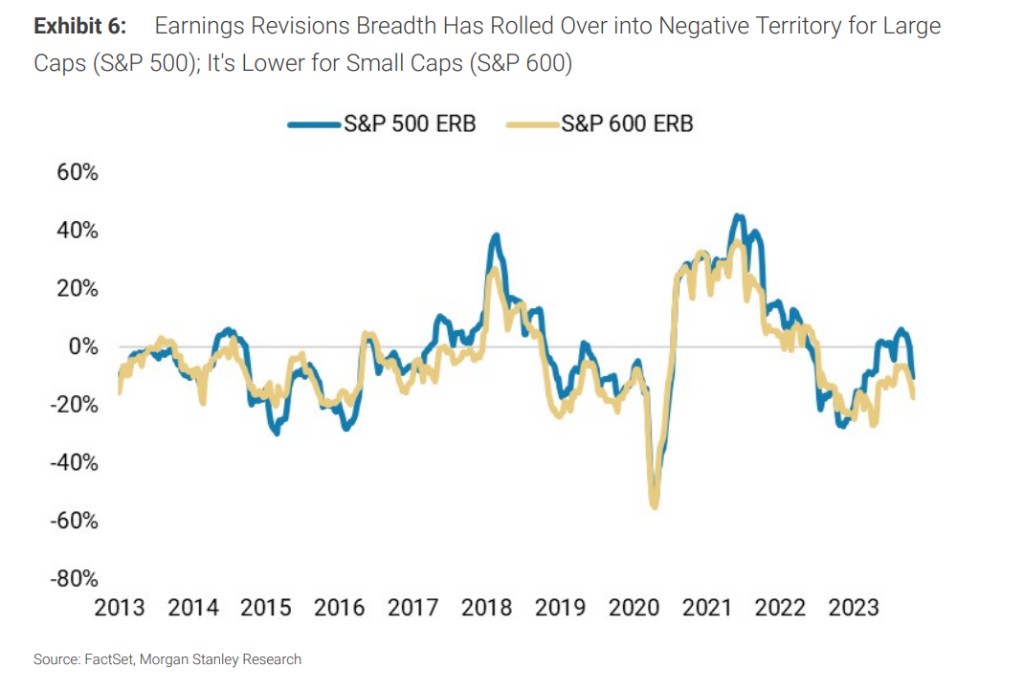

摩根士丹利指出,在過去 2 個月中,盈利預期改善廣度指標和表現廣度指標都顯著惡化。

2024 年盈利預期改善廣度繼續為負值 (-10%),為 3 月以來的最低水平,這意味着下調預期的公司數高於上調預期的公司數。標普 500 指數成分股的 70% 都面臨負面的盈利預期廣度。保險和消費服務行業絕對預期廣度最強,而汽車和運輸行業最弱。小盤股的盈利預期也開始變差,且低於大盤股。隨着盈利季的推進,我們看到財報公佈後的第一個交易日,盈利預期有所改善,現在為 0%,比兩週前的-0.8% 有所改善。

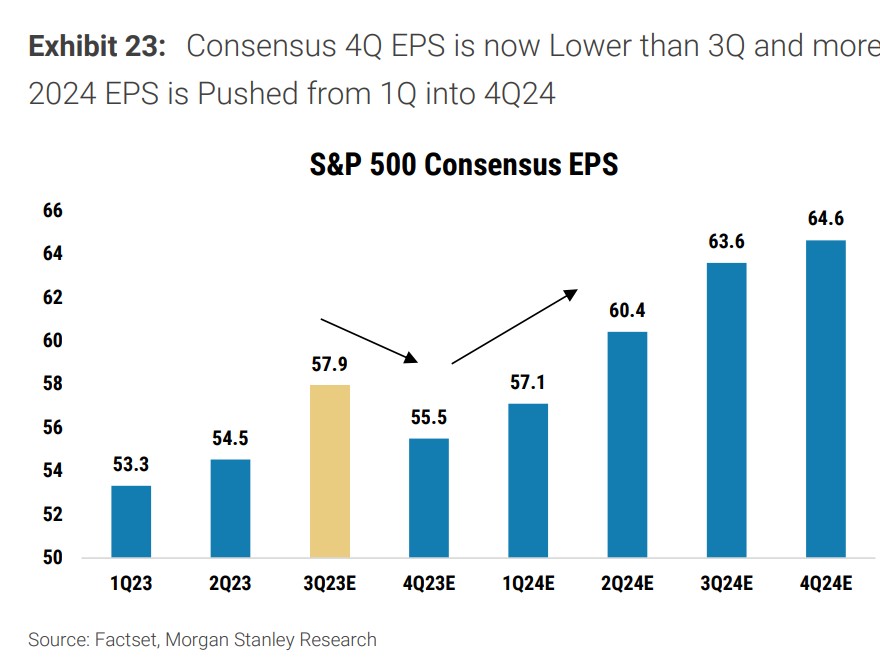

摩根士丹利表示,雖然三季度利潤保持穩定,但自財報季開始以來,第四季度預期大幅下調。

三季度銷售疲軟以及利潤預期被下調,背後的原因是消費者仍對大環境感到悲觀,因而在消費方面較為保守。

根據摩根士丹利最新一期的消費者調查,消費者更願意在必需品和家居用品上花錢,在小家電、消費類電子和外出用餐方面的消費意願最低。

尤其是在放假季,27% 的受訪消費者預計今年將比去年在假期購物上花費更少;25% 的人預計會花更多。

大多數假期消費者 (69%) 等待零售商打折才開始假期購物,平均折扣達到 30% 才願意花錢。

超過一半 (53%) 的消費者計劃在未來六個月內出行,這一比例略低於上個月的 55%。

隨着今年秋季學生貸款支付暫停期結束,債務償還成為消費者關注的焦點,逾期或已經錯過賬單或貸款還款的消費者比例,從我們前一次調查的 34% 上升至 40%。

摩根士丹利維持對防禦性成長股和後周期週期性股票的槓鈴配置的建議。具體而言,摩根士丹利看好醫療保健、必需消費品和公用事業等傳統防禦股,以及工業和能源等後周期週期性股。

Source: 華爾街見聞 The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.

Post your comment

No Comments