Morgan Stanley bear Wilson: Global stock market rise not due to fundamentals, but because financial environment too loose

Wilson 指出,在美聯儲最新的政策態度下,假設其對通脹或更寬鬆的金融環境不再過於擔憂,大宗商品導向型的週期性股票特別是能源股或許即將迎來追趕的機會。

過去 5 個月裏,MSCI 全球股票指數上漲了大約 25%。華爾街知名大空頭——摩根士丹利首席投資官兼美國股票策略分析師 Mike Wilson 認為,其主要原因在於更加寬鬆的金融環境和估值的上升,而非基本面的持續改善。

Wilson 指出,在美聯儲最新的政策態度下,假設其對通脹或更寬鬆的金融環境不再過於擔憂,那麼,大宗商品導向型的週期性股票特別是能源股或許即將迎來追趕的機會。

未來兩年盈利預期不變

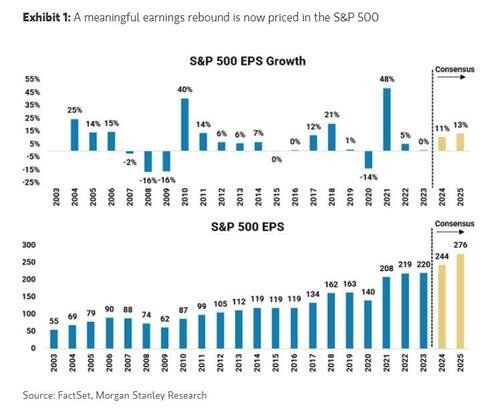

Wilson 在最新發布的文章中將當前的估值與 2021 年進行了比較,並指出,2024 年和 2025 年的盈利預期幾乎未見調整,因此很難僅根據基本面來證明較高估值的合理性。

我們在 2020 年,針對疫情應對策略轉向更多依賴財政政策的情況,提出了"繁榮 - 衰退"的預測理論。基於對 2020-2021 年經濟強勁復甦帶動盈利增長的預期,我們對股市持積極態度。預期中的這波盈利增長,以及由於疫情期間人們居家隔離使企業能夠降低人工成本和其他開支,從而帶來的巨大經營槓桿效應,最終實現了三十年來最快的盈利增長速度和創紀錄的利潤率,股價繁榮之後緊接着的就是盈利繁榮。

支撐股價上漲的不僅是盈利的增長,還有歷史上最為寬鬆的貨幣政策的助力,在經濟從疫情中復甦的過程中,美聯儲將利率長期保持在零水平,並在 2021 年全年繼續實施量化寬鬆政策。那一年標普 500 的盈利增長超過 45%,達到歷史最高。

目前,股票的估值已與 2021 年相當,這主要是基於對於經過去年盈利放緩後成長預期的改善。儘管最近金融環境的寬鬆可能預示着盈利的加速,但對 2024 和 2025 年標普 500 指數每股收益(EPS)的預期在美聯儲第四季度採取較為鴿派立場後依然保持不變。

另外根據股市最近一年的表現,Wilson 發現,盈利在推動股票上漲方面存在一定的侷限性。因此,大多數股票的價格仍未達到 2021 年的高點。

儘管股市整體表現受限,但注重運營效率的企業仍有所表現,這也是市場能否尋找到持久增長動力的關鍵所在。

作為補充,企業正日益致力於提高運營效率,這已經成為我們過去兩年的關鍵主題,也是我們最近的 TMT 會議上討論的熱點問題。持續提升運營效率,以此來抵消週期性逆風並推高利潤率,可能成為股市盈利調整的催化劑。

工業與能源板塊潛力巨大

展望未來,Wilson 表示,工業與能源兩大行業憑藉政策驅動和技術創新展現出較強的市場表現潛力,特別是在美聯儲緩和對通脹的擔憂後,資源導向的週期性行業,如能源,或將迎來估值修復和盈利增長的良機。

Wilson 指出,在美聯儲最新的政策態度下,假設其對通脹或更寬鬆的金融環境不再過於擔憂,那麼,大宗商品導向型的週期性股票特別是能源股或許即將迎來追趕的機會。

從估值和相對盈利修正趨勢來看,能源板塊已經表現出吸引力。值得注意的是,與任何其他行業相比,自疫情以來,能源行業對標普 500 盈利變動的貢獻最大,但它仍然是市場上最為低估和最少持有的領域之一。

鑑於美聯儲最新利率決議維持了年內降息三次的預期並上調了經濟前景預期,交易員們感覺到了美聯儲基調的變化:對實現2%通脹目標的道路緩慢感到越來越放心。

並且,在會議後的新聞發佈會上,鮑威爾迴避了關於金融環境是否過於寬鬆的問題,被市場解讀為金融環境短期內不會收緊的“買入” 信號。