China Passenger Car Association: Passenger car retail sales in April decreased by 5.7% year-on-year, while new energy vehicle retail sales increased by 28.3% year-on-year

展望後市,乘聯會預計,汽車以舊換新補貼對車市私人新車消費會帶來百萬量級的增量,也能帶來千億元以上的年消費增量,5 月車市有望一掃低迷狀態實現恢復性增長。

受傳統淡季、消費者觀望氣氛濃重等因素影響,4 月車市表現低迷,全國乘用車市場零售同比下降 5.7%,但以舊換新政策落地帶來重大利好,乘聯會預計 5 月車市零售會好於 4 月。

5 月 10 日,乘聯會發布 4 月份乘用車市場分析報告。4 月全國乘用車市場零售 153.2 萬輛,同比下降 5.7%,環比下降 9.4%。今年以來累計零售 636.4 萬輛,同比增長 8.0%,一季度車市零售基本實現預期中的開門紅走勢。

乘聯會指出,價格不穩等因素導致消費者觀望氣氛濃重,抑制了銷量提升空間:

雖然 4 月 22 個工作日,同比多兩日,但因價格不穩等因素導致消費者觀望氣氛濃重,4 月乘用車零售出現週期性環比下行走勢。新能源車的新車價格戰帶來一定增量,但持續性也不強,內部分化嚴重。

持續價格戰下的常規燃油車型大部分沒有持續降價的空間,因此市場被新能源車加速侵蝕,帶來部分用户的觀望,這進一步抑制了銷量提升空間。

此外,乘聯會表示,由於 4 月廠商生產和出口創新高,但零售偏弱,形成了廠商產量高於批發 3.6 萬輛,而廠商國內批發高於零售 0.8 萬輛的加庫存走勢。廠商與渠道庫存 3 月開始加大,4 月一般是去庫存特徵,今年因 “五一” 備庫存而稍高。

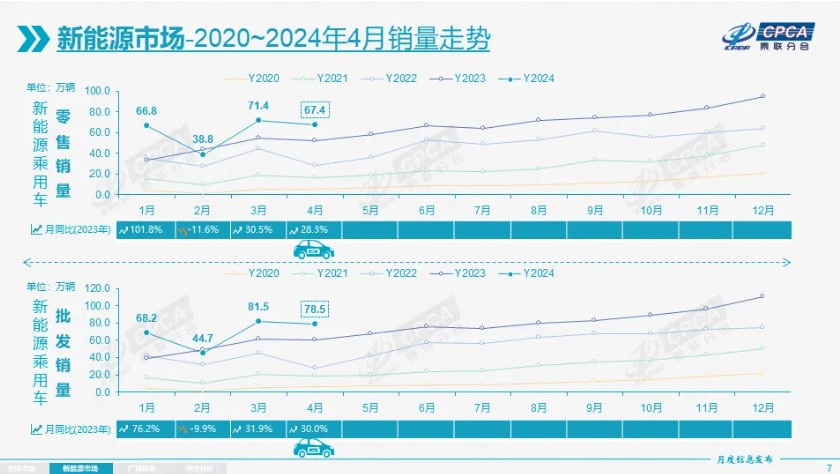

4 月新能源車零售同比增 28.3% 國內零售滲透率 43.7%

新能源車方面,4 月新能源乘用車產銷增幅放緩增長:

4 月新能源乘用車生產達到 80.2 萬輛,同比增長 33.5%,環比增長 0.9%;

4 月新能源車市場零售 67.4 萬輛,同比增長 28.3%,環比下降 5.7%;

出口 11.5 萬輛,同比增長 26.8%,環比下降 4.1%;

乘聯會指出,4 月新能源月度批發銷量突破萬輛的廠商達到 14 家(環比持平,同比增加 3 家),佔新能源乘用車總量 86.6%(上月 86.5%,去年同期 80.7%),其中比亞迪汽車 312048 輛、特斯拉中國 62167 輛、吉利汽車 51428 輛。4 月廠商出口方面,比亞迪汽車 41011 輛、特斯拉中國 30746 輛。

出口方面,4 月新能源乘用車出口 11.5 萬輛,同比增長 26.8%,環比下降 4.1%,佔乘用車出口 27.9%,較去年同期下降 2.9 個百分點。乘聯會表示:

伴隨着中國新能源車的規模優勢顯現和市場擴張需求,中國製造的新能源產品品牌越來越多地走出國門,在海外的認可度持續提升,雖然近期受到歐洲的一些干擾,但長期看新能源出口仍然市場向好,前景光明。

從監控的自主品牌出口的海外市場零售數據看,A0 級電動車佔比近 50%,是自主出口絕對主力,上汽等自主品牌在歐洲表現較強,比亞迪在東南亞和南美等市場崛起。除了傳統出口車企的靚麗表現,近期新勢力出口也逐步增量,海外市場也有數據開始顯現。

滲透率方面,乘聯會指出,4 月新能源車國內零售滲透率 43.7%,較去年同期 32% 的滲透率提升 11.7 個百分點。4 月,自主品牌中的新能源車滲透率 66.8%;豪華車中的新能源車滲透率 22.6%;而主流合資品牌中的新能源車滲透率僅有 7.5%。

從各車企表現來看,乘聯會表示:

4 月新能源乘用車企業總體走勢較強,比亞迪純電動與插混雙驅動夯實自主品牌新能源領先地位;以賽力斯汽車、理想汽車、長安汽車、零跑汽車等為代表的增程式電動車市場表現尤為較強。

2023 年全年新能源批發結構中:純電動 69%、真插混 23%、增程式 8%,增程式有效彌補純電動的續航焦慮,應該屬於純電動的新分支。

5 月車市有望實現恢復性增長

展望 5 月車市,乘聯會表示:

今年 5 月共有 21 個工作日,與去年相同,但今年連續 5 天的假期壓縮了 5 月的產銷時間間隔,隨着夏季的淡季臨近,車市進入平穩期。4 月份,中國製造業採購經理指數(PMI)、非製造業商務活動指數和綜合 PMI 產出指數分別為 50.4%、51.2% 和 51.7%,三大指數繼續保持在擴張區間,對車市的穩定促進有明顯作用。

隨着國家 “以舊換新” 的政策落地實施、各地相應政策措施出台與跟進,加之車市新品價格戰階段性降温,市場觀望羣體消費熱情被激發,市場應進入相對較好的發展階段。

乘聯會還提到,今年假期的自駕遊火爆程度又有提升,私車自駕、租車自駕等個性化、低成本出行方式成為更多人的選擇。輔助駕駛帶來更多駕駛樂趣,智能座艙的獨立空間體驗享受,以大長假錯峯的形式實地驗證補能網絡基礎設施完善情況,均有利於新能源車的消費熱情提升、消除常規燃油車消費者的轉型顧慮。

以舊換新政策落地是重大利好

乘聯會指出,以舊換新政策落地,對車市是重大利好,雖然 5 月休假時間長,但預計 5 月車市零售會好於 4 月。

乘聯會發文指出,

從春節後消費者就關注以舊換新的政策,期待政策帶來購車實惠,因此政策的實施對車市是重大利好,預計年度報廢總量應能達到近千萬輛的規模,汽車以舊換新補貼對車市私人新車消費會帶來百萬量級的增量,也能帶來千億元以上的年消費增量,5 月車市有望一掃低迷狀態實現恢復性增長。

預計補貼政策的財政效果也會很顯著,初步估算 1 元補貼投入的產值,能拉動的比例為 1:15,而且 1 元財補私人報廢更新的税收拉動比例為 1:3。

此外,常規燃油車消費的持續低迷是抑制車市全面回暖的重要因素,乘聯會認為此次以舊換新、報廢更新等政策,合理保證了燃油車消費羣體的換購需求,有益於未來幾個月的車市逐步走強。

1-3 月中國佔世界新能源車份額 62% 行業利潤率 4.6%

乘聯會表示,世界新能源 1-3 月相對前幾年的走勢放緩較多,中國新能源乘用車的增速強於世界平均增長速度

2024 年 3 月世界新能源乘用車銷量 128 萬輛,同比增長 17%,環比增長 60%。1-3 月世界新能源乘用車達到 311 萬輛,同比增長 21%。因為歐美新能源走勢放緩,世界新能源 1-3 月相對前幾年的走勢放緩較多。

今年歐洲 1-3 月新能源乘用車銷量 65 萬輛,增速 4%,北美新能源乘用車銷量 35 萬輛,增速 8%。歐美新能源的銷量增速放緩,目前早期嘗試者和環保主義者都已經購買了電動汽車,主流消費者對充電基礎設施、電池壽命、保險成本仍有較大擔憂,在較高利率下即使放開自動駕駛的使用,但銷量滲透率提升沒有達到預期,S 曲線的滲透特徵尚不明顯。

近期中國新能源乘用車的增速強於世界平均增長速度,2023 年的中國佔世界份額 64%,2024 年 1-3 月份額是 62.5%,表現仍較強。

乘聯會還指出,一季度油電混動的佔比在提升:

2024 年 1-3 月份汽車銷量初步統計達到 2105 萬輛,新能源汽車達到 324 萬輛,其中純電動車的世界汽車佔比達到 10.2%,插電混動佔比達 5.2%,而混合動力佔到 6.4%,油電混動的佔比在提升。

利潤率方面,車企利潤總體稍有改善,但部分企業生存壓力在加大:

2024 年 1-3 月汽車行業收入 22,483 億元,同比增長 6%;成本 19,642 億元,同比增長 6%;利潤 1,040 億元,同比增長 32%;汽車行業利潤率 4.6%,仍低於整個工業企業利潤率 4.9% 的平均水平。隨着車市生產規模擴大,PPI 下行,上游碳酸鋰成本下降,車企利潤總體稍有改善。

2024 年 1-3 月汽車行業在低基數下的產銷狀況較好,但競爭壓力大,利潤主要靠出口和高端豪華兩端,其它大部分企業盈利下滑劇烈,部分企業生存壓力在加大。由於燃油車仍有盈利,但市場萎縮較快;新能源車雖高增長,卻虧損較大,矛盾壓力突出,