CICC Strategy: Prosperity is the core criterion for testing the technology market

近期市場波動加劇,但科技成長股表現突出。科創 50 逆市上漲 1.69%,行業層面上,電子、國防軍工和汽車等為代表的成長行業表現佔優。市場風格 “高切低”,投資者開始尋找低位、有足夠 “安全邊際” 的行業。科技成長股表現佔優主要源於市場資金 “高切低” 與產業和政策的催化。近期科技成長股的擁擠度和股價均處於低位,也吸引了北上資金的加倉。總結而言,近期科技成長股表現突出的原因在於市場資金 “高切低”、產業和政策的催化以及科技行業具備較高的性價比。

一、近期科技成長股為何表現突出?

近期市場波動加劇,但科技成長股表現突出。5 月 24 日至 6 月 12 日期間,科創 50 逆市上漲 1.69%,領漲主要寬基指數;行業層面上,電子、國防軍工和汽車等為代表的成長行業表現佔優。

我們認為其背後的核心原因在於行業輪動加速、缺乏明確主線的背景下,市場風格 “高切低”。我們通過一級行業近五日漲跌幅排名變動絕對值加總,構建了行業輪動強度指數。5 月以來,輪動強度快速上行,市場進入到一個較為混沌、缺乏清晰主線的時間。疊加前期市場擁擠度較高,成交量與情緒高位回落,投資者開始尋找處於低位、有足夠 “安全邊際” 的行業。

一方面,5 月中下旬科技成長的擁擠度、股價均處於低位。從擁擠度來看,截至 5 月 24 日,半導體、消費電子、光模塊、計算機設備、軍工電子和辦公軟件等多數細分成長行業的擁擠度處於較低水平;從股價位置來看,截至 5 月 24 日,成長風格年初至今表現靠後,計算機、電子、傳媒、軍工等跌幅靠前;從成長/價值比價來看,5 月下旬時成長/價值相對位置也回落至歷史低位。

另一方面,放眼全球,A 股一些科技行業也具備較高的性價比。例如 A 股半導體與費城半導體指數和估值比價均處於歷史低位,也因此吸引北上資金自 5 月中下旬以來持續加倉半導體和消費電子等行業,進而強化了成長股佔優的風格。

與此同時,產業和政策端的催化也為科技股 “添了一把火”。一方面,國家大基金三期於 5 月 24 日正式成立,註冊資本達 3440 億元人民幣,超過前兩期總和,將持續支撐國內半導體產業發展。另一方面,蘋果於 6 月 10 日召開的 WWAC 上推出 Apple Intelligence,AI 應用端有望加速落地,美股 AI 加速上漲,對國內產業形成映射。

總結而言,近期科技成長股表現佔優主要源於市場資金 “高切低” 與產業政策的催化。

二、本輪科技股反彈依舊是龍頭佔優、高景氣佔優

近期科技股表現亮眼,尤其是 “科特估” 概念火熱,不少投資者關心市場是否會重新回到 “題材”、“小票” 的模式中去。但值得注意的是,本輪科技股反彈並非普漲,內部分化劇烈,依舊是龍頭風格佔優、高景氣佔優。

本輪科技股反彈依舊是龍頭佔優。興證策略團隊年初以來多次提出隨着資金面核心資產統一戰線的重塑和龍頭盈利優勢的凸顯,龍頭將成為今年以來重要的超額收益來源。而我們統計了軍工、電子等成長板塊一級行業 5 月 24 日至 6 月 12 日的漲跌幅中位數,發現各行業中的市值前 5 大龍頭股表現出明顯的超額收益。以近期表現最優的電子和國防軍工為例,二者龍頭平均漲幅為 4.9%、4.8%,而板塊內非龍頭個股的漲跌幅中位數僅為-0.1%、-3.8%。

並且,景氣也是導致行情分化的重要原因。行業層面上,本輪成長股反彈中,基本面預期改善的半導體、消費電子、光模塊和軍工領漲,景氣度仍處於低位和預期未明顯改善的傳媒和新能源表現靠後。個股層面上,5 月 24 日以來,各成長行業/板塊中,盈利預期上修個股漲跌幅的中位數顯著優於盈利預期下修個股漲跌幅的中位數。

因此,本輪科技成長股的反彈,龍頭佔優、高景氣佔優,仍是高勝率投資模式,市場的審美偏好並未發生變化。

三、高勝率投資時代,景氣是檢驗科技行情的核心標準

今年以來,興證策略提出市場將進入高勝率投資模式,並將其歸納為高景氣、高 ROE、高股息三大主線。當市場有確定性景氣方向或產業趨勢的時候,高景氣就是最高勝率的選擇,進攻就是最好的防守。典型代表就是高景氣驅動的美股 AI、以及 A 股光模塊行情。因此,高勝率投資時代,景氣是檢驗科技行情的核心標準。

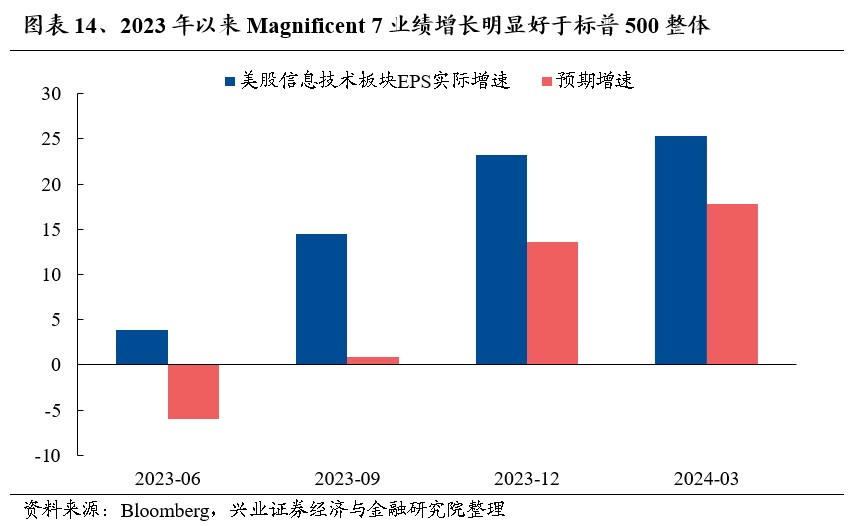

美股持續走牛的核心在於 AI 產業革命浪潮加持下科技股的支撐。2023 年以來,截至 2024 年 6 月 12 日,標普 500 指數和納斯達克指數分別上漲 41.2%、68.2%。而細究其上漲的原因,我們發現主要來自於 AI 相關個股的驅動:如微軟、谷歌、英偉達、AMD、臉書等權重個股在 AI 浪潮推動下,均實現顯著上漲。而當我們剔除其中的 AI 相關個股後,可以看到標普 500 指數剩餘成分股市值加權收益水平僅為 14.7%,顯著低於 AI 板塊 124.9% 的市值加權收益率水平。

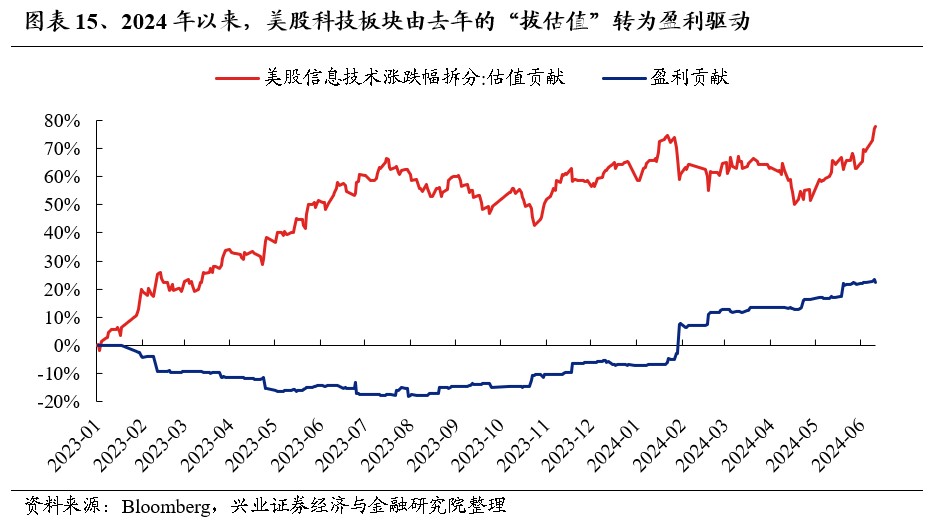

而美股 AI 板塊超額收益的背後,則是其持續兑現的高景氣預期。儘管拆分納指漲跌幅的驅動力來看,2023 年主要由估值驅動,但其估值的提升也離不開基本面的支撐。受益於 AI 產業浪潮,市場預期美股科技板塊業績將實現快速增長,22 年底以來信息技術和通信的盈利預期持續快速增長,也催化初期的 “拔估值” 行情。但隨着行情持續演繹,美股 AI 板塊估值能夠持續且穩定上漲則主要得益於其能夠持續兑現市場的業績預期,例如信息技術行業 2024Q1 EPS 增速錄得 25.35%,再度好於市場預期。並且,值得注意的是,2024 年以來,美股科技板塊的漲幅由去年的 “拔估值” 轉為盈利驅動,進一步強化了基本面的重要性。

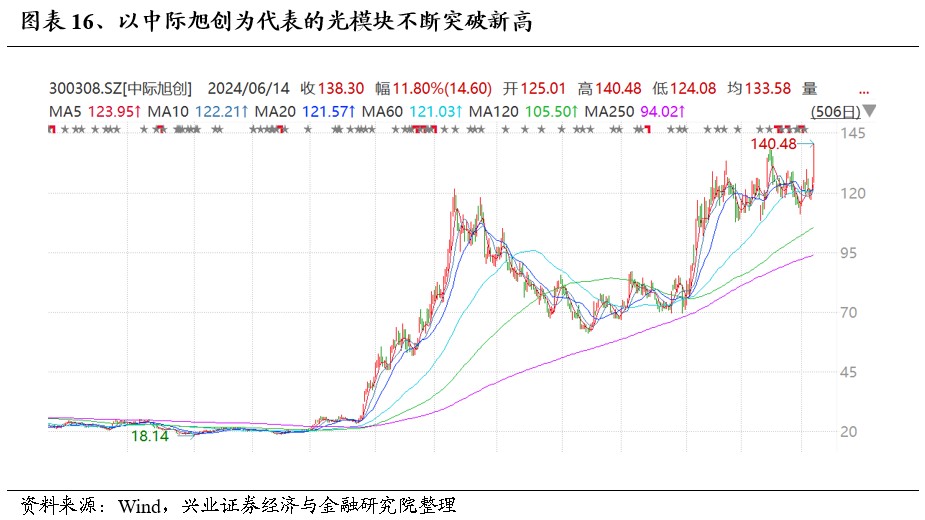

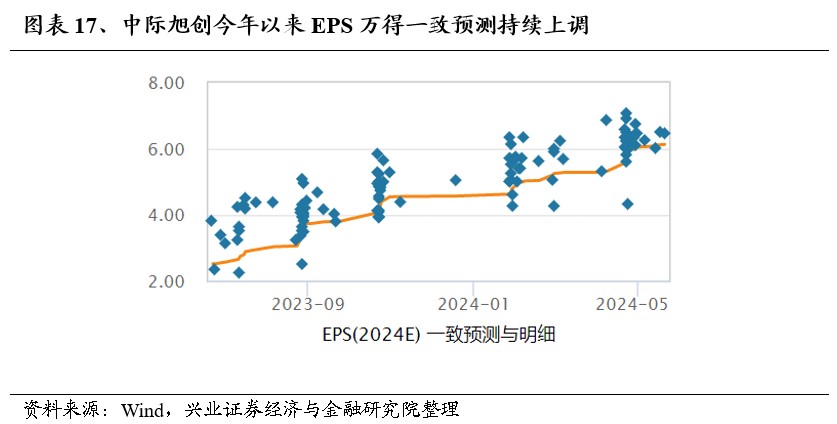

A 股亦是如此,以中際旭創為代表的光模塊不斷突破新高,也源自背後持續兑現的高景氣。中際旭創 23 年、24Q1 淨利潤增速分別是 77.6%、303.8%,24 年一致預期增速 126.6%,高景氣持續兑現,且去年以來預期 EPS 持續上修。

因此,高勝率投資時代,景氣是檢驗科技行情的核心標準,更應當耐心做多科技真成長,而非板塊、主題性的炒作。

風險提示

關注經濟數據波動,政策超預期收緊,美聯儲超預期加息等。

本文轉載自"堯望後勢",智通財經編輯:葉志遠。