MORIMATSU INTL, a potential player in the Hong Kong Stock Connect in September

森松國際是一家壓力容器設備製造商,具有成長性且背景特殊。公司營收最大地區為中國,計劃納入港股通並加大股東回報力度。森松國際的優勢在於創新能力強,長期合作客户羣體穩定,業務遍佈海外。公司實施了內部創業機制,鼓勵員工團隊註冊公司,避免人才流失。若公司成功納入港股通,估值重修確定性將進一步加強。

在往期的港股困境反轉系列後,港股還有不少被市場低估,價值未被發現的好公司,例如森松國際(2155.HK)。

在複雜的地緣政治背景下,具有成長性的跨國企業是稀有的,而森松國際恰好就是公司背景特殊,出海業務發展成熟,被市場過度錯殺,還有較大修復空間的一家公司。

不足的點是股東回報不夠給力,若今年公司成功納入港股通,公司順勢加大股東回報力度,估值重修的確定性將進一步加強。

一、特殊背景的森松國際

森松國際是一家壓力容器設備製造商,指在大容積設備內實現理論上可達到的傳染和傳質效果的核心設備。例如,用於生物製藥領域的生物反應器,用於化工行業的氧化反應器,以及用於油氣行業的加氫反應器等。

公司創始人來自日本,森松國際是一家在中國發展的日資公司。由於工廠設立在中國,營收最大地區也是中國,公司順應在港股上市。

在運營模式和企業文化上,森松國際類似於日本製造業龍頭基恩士。同樣是幫助客户設計創新能力很強,這種模式有利於客户與公司長期合作,以及加深護城河。

例如,當客户在生產環節中遇到效率低的問題,或是有新需求時,這就需要設備商與客户合作研發,這就很考驗設備製造商的設計能力,而大多數傳統制造商只能生產設備,在設備創新方面的技術薄弱。

森松國際的優勢是創新能力強,這使得客户羣體較為穩定,客户都是各行業的頭部公司,業務遍佈海外。截止 2023 年,國內和海外的營收各佔一半。

為保證公司的創新能力,森松國際的作法是實施了一套公司內部創業機制,若員工能找到新的領域,可以在公司內結成團隊嘗試發展。當業務規模到一定程度時,公司會鼓勵團隊註冊公司,森松國際持股 75%,核心員工持股 25%,這也能避免公司人才被挖走。

簡單來説,森松國際是一家制造業鏟子股,在下游客户有擴產能需求時,就需要用到森松國際的設備。可借鑑基恩士的例子,創新能力是最好的護城河,也是最直接與客户保持長期合作關係的方式。

由於傳統壓力設備的門檻不高,並不是所有壓力設備都需要極高的技術水平,所以行業的集中度非常分散。森松國際僅佔市場份額的 1.5%,排在第四名。而對壓力設備有較高要求的行業,主要是醫藥、化工、油氣、新能源行業。

今年對這 4 個行業有設備更新需求的,主要都是海外公司,所以今年森松國際的主要看點是海外收入。今年業務出海也是資本市場熱炒的邏輯之一,森松國際是最正宗的出海股之一,目前市場還沒完全反應。

二、市場錯殺的產生

自去年 2 月高位以來,森松國際已跌去 50%,目前估值為 6.5 倍 PE。近兩年,公司估值高位時為 18 倍 PE,2022 年平均 PE 為 14 倍左右,參考歷史估值起碼有 1 倍的修復空間。

回顧大跌的原因,一是受加息週期影響,佔營收最大的生物製藥行業投資支出減少,行業景氣度下降,市場擔心設備收入增速下降。而其他油氣、化工行業的設備具有周期性,市場沒有預期到去年其他行業的收入會增長。

另外,由於藥明生物是森松國際的大客户,有部分資金把森松國際當做是醫藥設備股炒,森松國際和藥明系的股價相關性很強,以致於今年初藥明系海外業務受制裁風波影響時,也牽連森松國際跌出歷史新低。

但股價相關性在 4 月底森松國際披露 23 年報後已經解除。

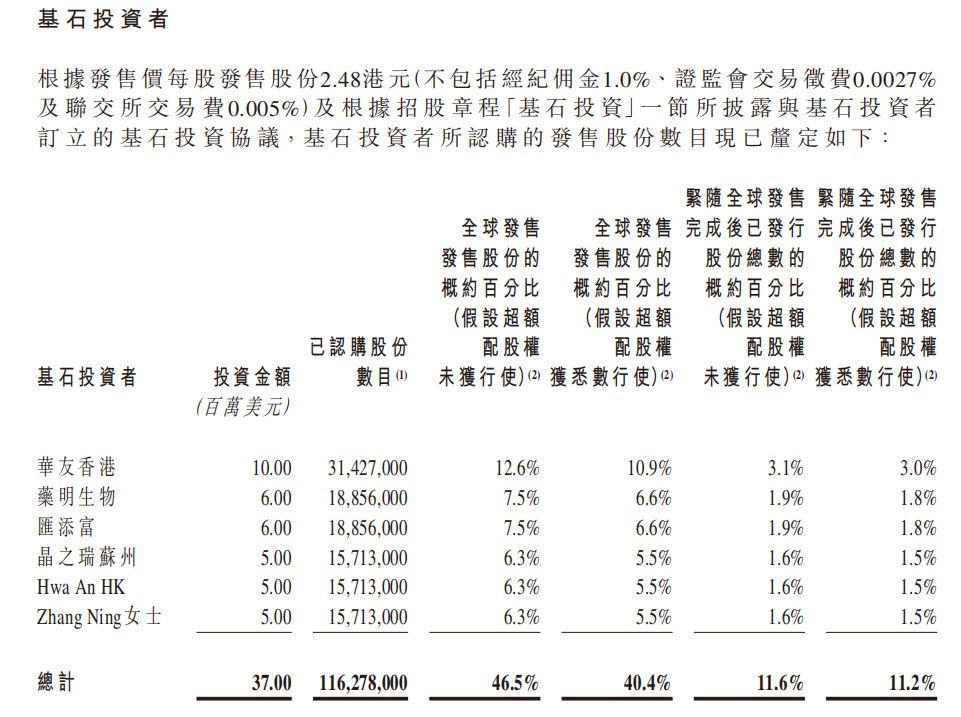

第二點,基石投資者在過去 3 年裏不斷減持森松國際,目前已接近清倉完畢。在目前公司業績轉好時,基石投資人的離場可以説是給投資者砸出一個黃金坑的機會。

基石投資者是華友鈷業、藥明生物、匯添富、半導體的晶之瑞,以及兩位個人投資者,這幾位共持有 IPO 發行後總股本的 11.2%(假設算上公司股權激勵授予增發),共 1.16 億股。

由於森松國際流動性過差,長期單日成交額在幾百萬港元左右,導致基石投資者清倉都花了 2-3 年的時間。上市時,森松國際大股東 “森松株式會社” 持有 75%,加上基石投資者持有 11.2%,市面流通股剩下 13.8% 左右。

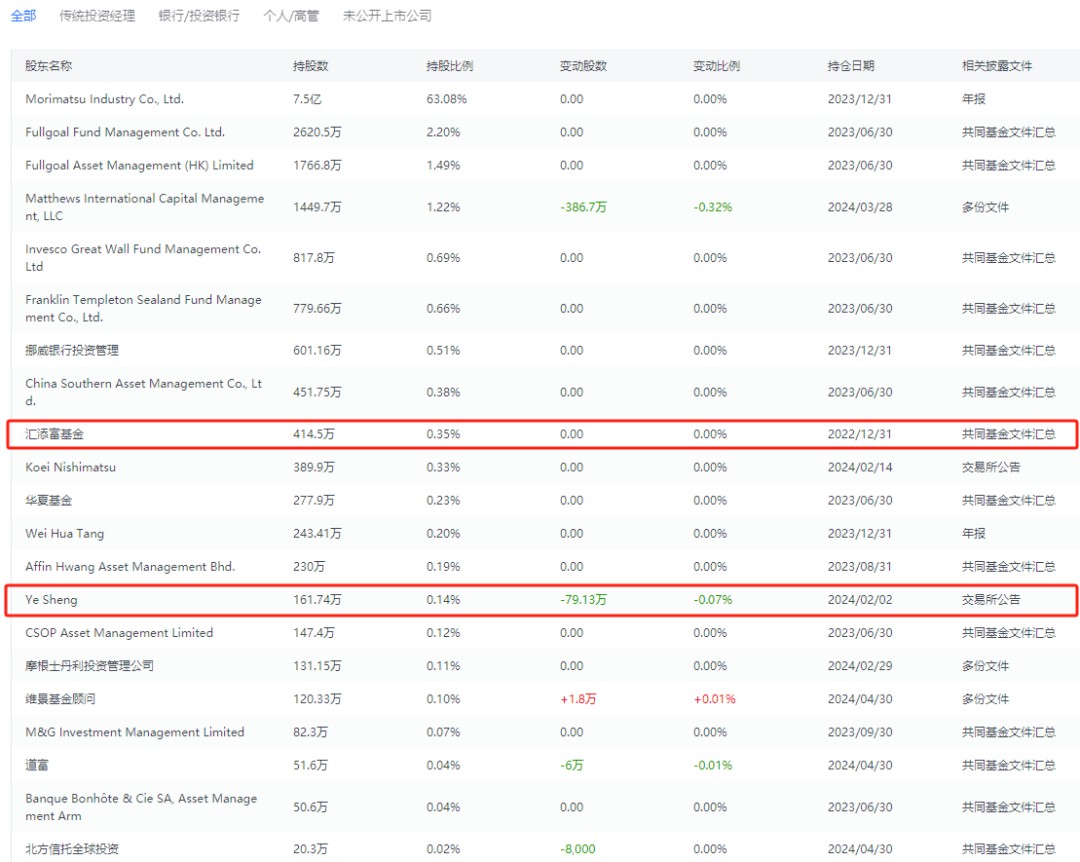

根據富途數據顯示,華友香港、藥明生物、晶之瑞、Hwa AN HK、Zhang Ning 女士,五位基石投資人已清倉。只剩下匯添富持有 414.5 萬股,持有約 0.35%,較認購時的 1885 萬股賣了 1400 多萬股。即使匯添富後續清倉,剩下幾百萬股對股價影響也不大。

值得注意的是,基石投資人減持的股票,主要都是外資接手了,目前絕大多數都是外資機構持股,以及有挪威央行的身影。

基石投資人減持完畢後,藥明系的下跌也不該對森松國際產生那麼大影響,市場反應明顯過度悲觀了。

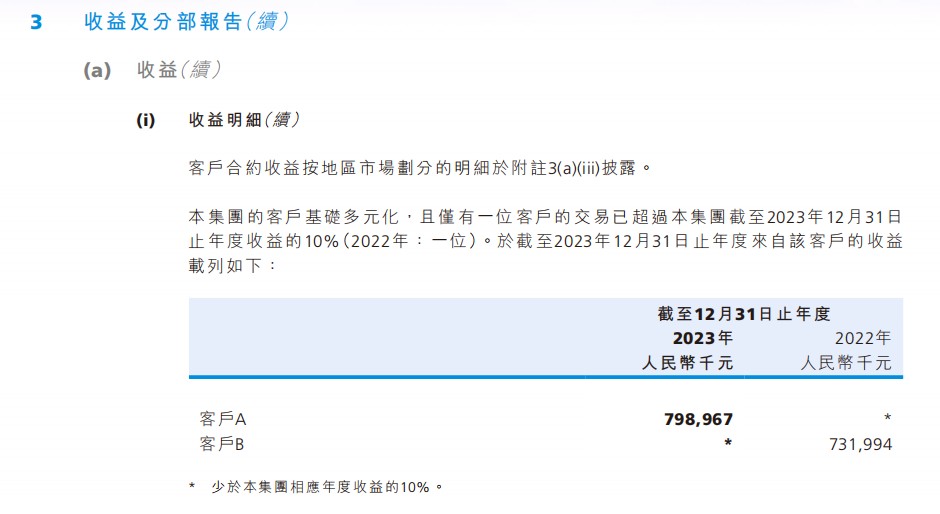

1、森松國際的客户足夠分散,不存在依賴單一大客户的情況,都是來自多個行業的頭部公司。根據 2023 年報披露,只有一位客户收入佔公司營收的 10%,最大客户的收入為 7.98 億元。整體收入足夠分散,即使藥明生物的投資額下滑,對森松國際的影響也有限。

2、業績與股價大跌的走勢背離。

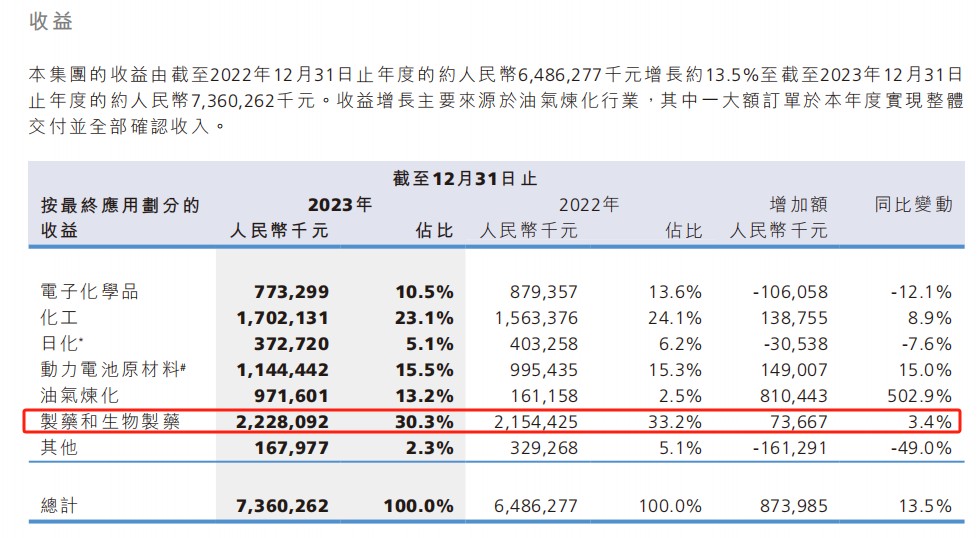

從收入來看,2023 年森松國際營收 73.6 億元,較 22 年增長 13.5%。歸母淨利潤為 8.45 億元,同比增長 26%,營收利潤實現雙位數增長。過去 3 年,森松國際也是保持着高增長。

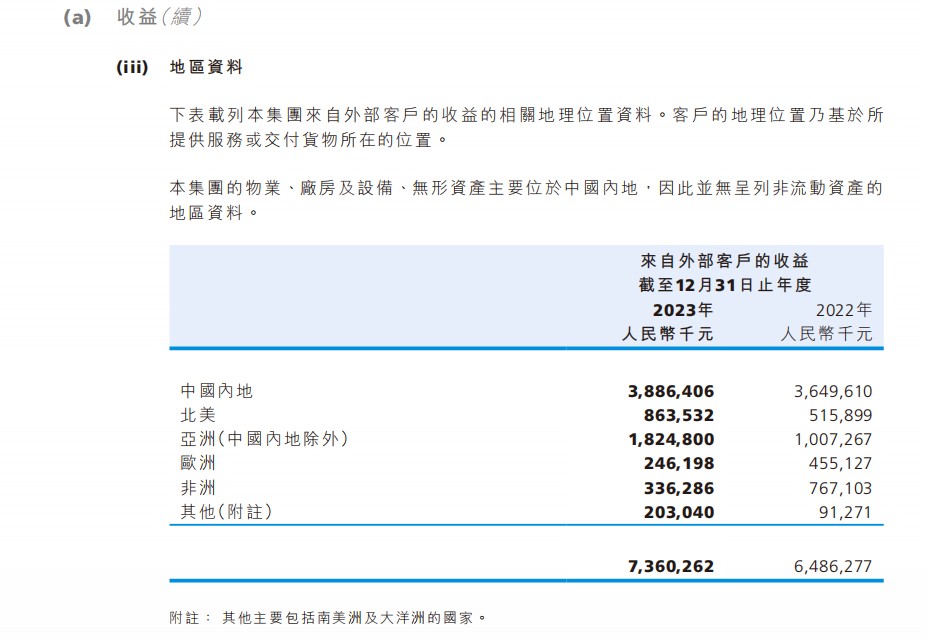

貢獻增長的地區主要是海外,海外各地區總營收從 22 年的 29 億元增長至 35 億元,國內營收從 36 億元增長至 39 億元。

其中,生物製藥收入為 22.28 億元,同比增長 3.4%。在生物醫藥融資逆風的加息週期裏,這已是不錯的表現。而佔比第二的化工行業,收入同比增 8.9%,收入佔比第三的動力電池原材料行業,收入同比增長 15%。這兩個行業使得森松國際在市場的低預期裏實現了高增長。

雖然電子化學品、日化、其他行業有所下滑,但收入基數不大,也沒有多大影響。

樂觀來看,若今年美元順利降息,明年醫藥投資逐步回暖,有利於海外醫藥大廠擴張設備投資額。退一步來講,從利率端考慮,至少能確認 2023 年醫藥行業最差的週期已經過去了,降息只是時間問題。

通過美股的 XBI Biotech ETF 來看,資本市場已在提前反應,美股醫藥板塊受加息延遲的影響在逐漸減少,市場是搶跑的,因為遲早都得降。同樣,降息也有利於油氣和化工行業加大投資。

森松國際的客户覆蓋 85% 全球 TOP 20 藥企和兩大頭部 CDMO,而其他國產製藥裝備廠商仍以國內的傳統藥企為主。一方面是技術優勢,另一方面是國外廠商比較少選擇與中資廠商合作,尤其是這個行業是要長期合作的。

石油化工行業方面,森松國際與巴斯夫、科思創、萬華化學和殼牌公司等長期合作。以及日化行業巨頭的寶潔等。

據財報披露,2023 年新簽訂單金額為 77.84 億元,較 22 年下滑 16.8%。新增訂單裏,海外佔 71.2%,在手海外訂單佔 63%,海外營收佔比有希望較去年的 50% 繼續提升。

海外 CXO 領域的 lonza 等藥廠今年都有不錯的訂單增長和資本支出規劃,而這些單由於生物法案,都不便於流向中資企業。

3、森松國際的特殊點在於,日資企業背景尤為重要,很大程度上消除了地緣政治風險。所以即使是在港股上市,也能吸引眾多外資機構買。

其次是技術優勢,國內製藥設備行業裏,價格優勢是每個國產廠家均具備的優勢。以森松國際為例,同規格的不鏽鋼生物反應器比國外廠家價格低約 30%。其中的核心點並不是技術比國外廠家強很多,而是在中國建廠後,後期的運營成本比國際同行要低不少,所以森松有能力與國際同行競爭。

簡單來説,與國內同行相比,森松有技術優勢,還是日資背景,能做出海業務。與國際同行相比,森松有中國的成本優勢。海外的訂單毛利率更加高,國內訂單的毛利率較低。

例如今年 Q1,市場此前將森松國際對標 A 股的東富龍和楚天科技,這兩家主要做國內藥廠的製藥設備。而做國內業務的東富龍、楚天科技的 24Q1 表現很差,創 2020 年以來的最差一季度表現,與出海訂單爆滿的森松國際相差巨大。

雖然業務不完全相同,但東富龍市值 106 億,預期 24 年淨利潤 7.5 億元,都有 14 倍 PE 左右。相比之下,今年預計賺 10.2 億的森松國際才 6.7 倍 PE,市值 70 億出頭。美股的同行丹納赫長期 PE 維持在 30 倍左右。

三、為何被受低估?

上述提到的基石投資者減持壓制股價之外,由於股權過於集中導致未被納入過港股通也是長期被詬病的問題。於 2021 年 11 月,香港證監會對公司發佈了股權高度集中通知,表示 “森松株式會社” 持股 72.29%,另有 17 名股東持股 21.14%,共持股約 93.43%,只有 6.57% 由其他股東持有。

實際上,近幾年森松國際的罵聲不少,先是基石投資者減持打壓股價,股價下跌時公司還在陸續增發股權激勵,由於股權過於集中,一直進不去港股通,難以解開流動性的問題,這些因素的確讓大多數投資人對公司的印象不太好,導致業績雖好,但股價慘不忍睹,公司不跟外界交流,也未能回購支撐股價,更多的現金流都用於擴產能,收併購去了。

不過,以上因素都有所改善,值得重新看待當下的森松國際:

1、在公司 IPO 前,員工購股權計劃而發行的股數數目為 2647 萬股。在 2021 年上市時,公司總股本為 10 億股,目前為 12.14 億股,還剩下約 500 萬股的增發,未來對股價影響實際不大。

公司管理層過去幾年基本沒有減持過,近幾年也穩健增長,公司成立幾十年,用增發授予的方式回饋員工也很合理,即使像美股科技 7 姐妹也是同樣的方式激勵員工。

2、在 2021 年 IPO 時,大股東 “森松株式會社” 持股 75%,在過去 3 年增發 2100 萬股後,大股東的持股比例已降低至 65%,這股權比例已有所優化,符合入港股通的條件。

3、公司開始重視股東回報。

2023 年末,公司首次派發現金紅利 1.22 億港元,分紅比例為 14.4%,每股派 0.1 港元。並開啓回購計劃,近 3 個月已回購 116 萬股,約佔總股本的 0.1%。

在管理層高比例持股,不減持的基礎下,後續管理層獲得獎勵的方法就是派息。

根據公司的經營能力,往後是有能力擴大分紅比例和回購計劃的。

公司賬上現金為 21.68 億元,計息銀行貸款為 3.65 億元,管理層表示借款在今年內還完,扣除負債後賬面現金是 18 億元,足夠今年內的資本開支。今年新增的淨利潤可以成為可支配現金,公司有能力繼續擴大分紅比例,根據 wind 預測中位數,今年森松淨利潤為 10.2 億元。

四、結語

森松國際在業務上是穩健發展的好學生,過去幾年的負面因素夾雜,還在港股上市,才形成這樣被低估價值未被發現的機會。若今年先進恒指,再納入港股通,加上公司擴大分紅回購,兩者合力有望形成戴維斯雙擊。

現在可以説是用上市以來最低估值的價位,買了發展階段最好的森松國際。