JP Morgan Fund continues to be optimistic about Asian semiconductor stocks: valuations are much lower than their American counterparts, with room for catching up

摩根大通知名基金经理称,亚洲芯片公司预期市盈率约为 17 倍,远远低于美国同行,且两者估值之差为 2009 年来最大,亚洲芯片股仍有上涨空间。

在英伟达剧烈回调之际,摩根大通亚太股票基金继续看好亚洲芯片股,认为它们较低的估值意味着还有上涨空间。

6 月 25 日,管理 12 亿美元规模摩根大通亚太股票基金(JPM Asia Pacific Equity Fund)的联席经理 Oliver Cox 预计,随着人工智能热潮有增无减,中国台湾、日本和韩国芯片供应链中的公司销售增长将加速。

数据显示,该基金在过去五年里对亚洲芯片股的投资帮助其跑赢了 97% 的同行。Cox 表示,“我们已经看到美国主要芯片公司的估值大幅重估,但相比之下,我们并没有看到许多亚洲供应链中的公司出现如此大幅度的估值重估,因此我认为(亚洲芯片股)仍有追赶的空间。”

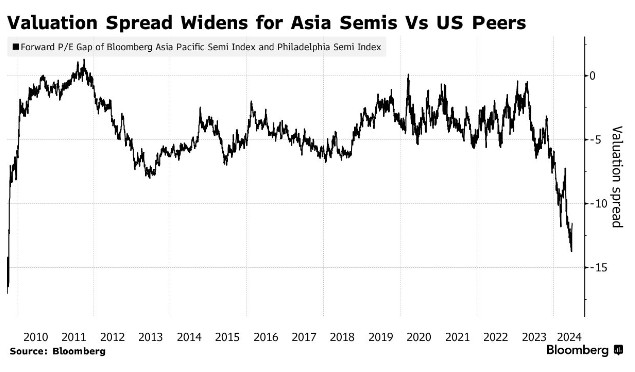

尽管英伟达在创下股价纪录之后连续三天大跌,但费城证券交易所半导体指数预期市盈率仍约为 28 倍,高于 20 倍的五年平均水平。跟踪亚洲主要芯片公司市盈率的彭博指数预期市盈率约为 17 倍。两者估值差距接近 2009 年以来最大。

同时,亚洲在全球芯片产业供应链中是极为关键的一环,Cox 表示,芯片行业 “前沿” 生产基地几乎全部位于亚洲,随着人工智能的加速发展,这些生产基地将是实现该行业雄心勃勃目标的关键。

根据 4 月的情况说明书,台积电是 Cox 所管理基金的最大持仓股,占比 9.6%。韩国芯片制造商三星电子和 SK 海力士也在持仓前六大股票之列。台积电台股今年已上涨逾 58%,而其主要客户英伟达的股价则上涨了 138%。

尽管跟随英伟达的步伐,不少亚洲芯片公司股价已经有了不错的表现。但 Cox 仍认为亚洲芯片公司还有上涨空间,他说,“我们认为仍有增长空间。这个行业周期看起来还相对较早。”

2023 年,摩根大通 Cox 就已经是亚洲芯片股的鉴定唱多者。当时 Cox 预计,AI 有望成为亚洲企业盈利增长更大的推动力,亚洲企业的 AI 订单热潮可能延续到 2024 年全年。除了估值比美国芯片股低,韩国供应商还可能受益于 DRAM 内存短缺。投资者的定价将开始体现亚洲企业得到更多的 AI 订单,推动这些企业的估值上涨。

日前,摩根士丹利也上调了对中国和日本的芯片行业评级。其分析师认为,科技业的通缩、即价格弹性,加之 AI 带来的长期半导体行业需求,料将共同催生下一个逻辑性的半导体行业上升周期。