Société Générale Société anonyme: The third quarter is a turning point for Asian stock markets, "China trade" returns

法興銀行亞洲股票策略主管 Frank Benzimra 表示,自今年 1 月 22 日觸底以來,MSCI 中國指數已上漲 24%,演繹了一場” 無聲牛市”。Benzimra 認為,中國股市正步入戰術性反彈的第三階段,企業盈利開始出現積極信號,在全球其他市場估值日益昂貴的背景下,中國公司估值具有較強吸引力。

法興銀行近日報告指出,三季度或將成為亞洲股市的關鍵轉折點,"中國交易"正重新成為投資者關注焦點。

自今年 1 月 22 日觸底以來,MSCI 中國指數已上漲 24%,演繹了一場"無聲牛市"。法興銀行亞洲股票策略主管 Frank Benzimra 表示,中國股市正步入戰術性反彈的第三階段,企業盈利開始出現積極信號。報告提及,在全球其他市場估值日益昂貴的背景下,中國公司估值具有較強吸引力。

日本股市方面,法興銀行更加看好日本金融板塊和價值投資風格股票。對於印度市場,該行持相對謹慎態度,認為高估值等因素可能制約上漲空間。

1. “中國交易” 歸來,中國股市正步入戰術性反彈的第三階段

自今年 1 月 22 日觸底以來,MSCI 中國指數已悄然上漲 24%,演繹了一場"無聲牛市"。

法興銀行亞洲股票策略主管 Frank Benzimra 認為,中國股市正步入戰術性反彈的第三階段。其中,第一階段國家隊和金融監管機構發揮了關鍵作用。第二階段始於房地產市場新政,標誌着更為有力的政策支持。當前,市場可能正在進入第三階段,企業盈利出現積極信號。

看完中國公司一季度的財報,Benzimra 表示:

"我們看到,企業盈利正在環比走強,下調預期的速度放緩,盈利廣度也從低位開始改善。"

值得一提的是,在全球其他市場估值日益昂貴的背景下,Benzimra 還在報告中強調了中國公司估值的 “吸引力”:“三個月前觀察到的估值吸引力依然存在”。進一步,Benzimra 補充稱:

“我們的模型顯示,如果長期利潤增長率上升 1 個百分點,MSCI 中國指數將有望上漲 80%。

反之,如果下降 1 個百分點,股價僅會下跌 18%。"

基於這一判斷,法興銀行建議投資者關注三類股票:離岸市場股票、大盤股與盈利韌性強、能穩定派息的股票。

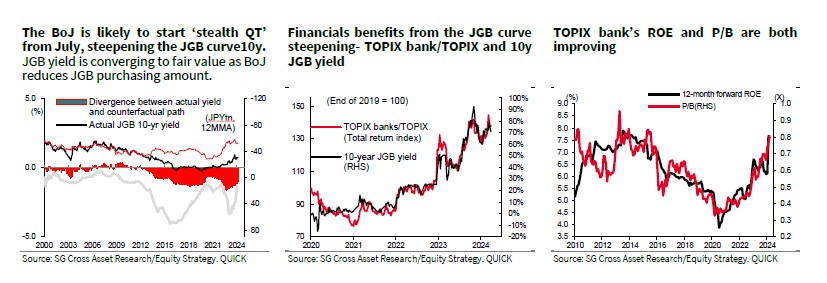

2. 日本:關注金融板塊和價值股

轉向日本市場,Benzimra 表示,支撐近 12 年牛市的基本面仍然穩固。"公司治理改革成效顯著,貨幣政策收緊步伐漸進温和,這些都是利好因素,"他説,"但投資者需要警惕日元匯率波動帶來的風險。"

在當前環境下,法興銀行更加看好日本金融板塊和價值投資風格股票。金融股方面,Benzimra 認為:

過去四年,東證銀行和保險股的表現明顯優於市場,分別高出東證指數 128% 和 149%。它們一直是、並將繼續是公司治理改革的受益者......

他們還繼續受益於日本央行的政策。日本央行預計今年夏天將削減日本國債購買規模,預計這將進一步加劇日本國債收益率曲線的陡峭化。

價值股方面,Benzimra 表示:

"陡峭的收益率曲線和治理改革正在支持整個價值投資風格。

自日本交易所推動上市公司提高資本效率(2023 年 3 月)以來,治理改革一直處於實施階段......估值最低的公司回購股票的積極性最高,東證指數中市淨率低於 1 的公司比例已從 2023 年初的 60% 左右縮減至目前的 40%。"

3. 印度:高估值或制約上漲空間

對於印度市場,法興銀行持相對謹慎態度。Benzimra 解釋説:

"雖然大選後政治不確定性已經消退,但市場面臨多重挑戰:估值處於高位,盈利增長放緩,外國投資者興趣不足,而國內投資者持倉已經較重......

這些因素可能會制約市場的上漲空間。"

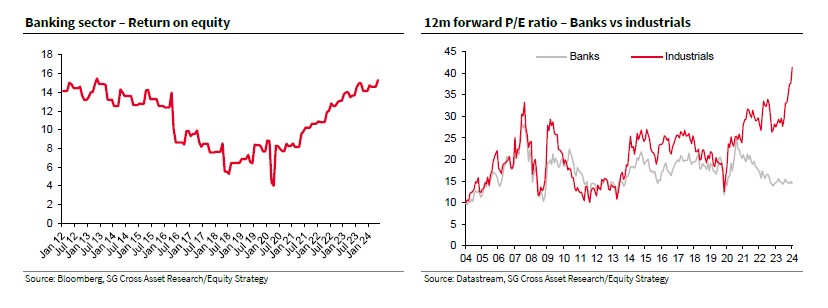

短期內,法興銀行 Benzimra 團隊建議投資者減持估值較高的工業板塊,轉而增持銀行股:

目前,隨着莫迪第三次連任,政治和政策的不確定性已經消退。儘管如此,我們預計高估值工業股的優異表現將會暫停。過去三年來,工業是政府推動資本支出的最大受益者。儘管市場普遍預計盈利增長將從去年的 60% 大幅放緩至 2024 年的不到 20%,但該行業的往績市盈率仍超過 40 倍(20 年平均水平的兩倍)。

與此形成鮮明對比的是,銀行由於其自身的特殊原因而錯過了資本支出行業的反彈,這些原因包括大型銀行的企業行動和淨息差收縮。然而,信貸增長、股本回報率和資產質量均處於八年來的最高水平。我們認為,隨着存款利率壓力隨着貨幣政策寬鬆預期的下降,銀行是為數不多的提供價值的行業之一。

本文主要內容來自於法興銀行報告:《Asia Equity Strategy:3Q24 Outlook – Inflection points》