"Fade trade" overheated? Interest rate pricing does not show that the Federal Reserve is "behind the curve"

美聯儲尚未落後於形勢,市場對其降息預期迅速升温。波動性飆升,市場競相對美聯儲未來幾個月的大幅降息進行定價,預計降息幅度約為 115 個基點。摩根大通預計,美聯儲將在 9 月和 11 月分別降息 50 個基點,12 月將降息 25 個基點。收益率曲線顯示投資者對未來寬鬆週期的預期。終端利率未低於 2.85%,高於政策中值利率。美聯儲將於下月開始降息,但降息幅度尚不明確。

美股市場過去一週出現了劇烈的波動和瘋狂的衰退交易,市場有一種不祥的感覺,即美聯儲已經落後於形勢。資深金融市場專家 Mike Dolan 指出,雖然美聯儲降息可能有點晚,但在阻止美國經濟衰退方面,它還沒有落後於曲線。而且利率市場尚未消化美聯儲可能挽救市場而實施緊急寬鬆貨幣政策立場——即在未來兩年寬鬆週期內任何時候的激進寬鬆政策。

市場降息預期迅速升温,但中性利率預期未反映深度衰退

上個月美國失業率出人意料的急劇上升顯然嚇壞了市場,而大型科技股的震盪進一步加劇了市場的恐慌。隨着波動性的飆升,市場已競相對美聯儲未來幾個月的一系列大幅降息進行定價。

美股越來越擔心美聯儲已經落後於曲線了,應該已經開始降息了。美聯儲沒有計劃在 8 月或 10 月召開利率制定會議,這降低了其在正常會議上進行政策調整的靈活性,這加劇了這些擔憂。會議計劃外的政策調整是可能的,但很少發生,通常是為了緊急情況。

就在一個月前,期貨價格顯示,預計在今年剩餘時間裏,美聯儲只會降息兩次 25 個基點,但現在的押注大幅上升——週二的最新統計顯示,市場預計美聯儲今年降息幅度約為 115 個基點。在一系列匆忙的預期修正中,最值得注意的是,摩根大通目前預計,美聯儲 9 月和 11 月將分別降息 50 個基點,12 月將降息 25 個基點。

現在毫無疑問,美聯儲將於下月開始降息:在上週的會議上,它發出了非常明確的信號。但降息幅度就不那麼明顯了。

但在收益率曲線更遠端的情況,或許更能説明投資者對未來整個寬鬆週期的預期。週一的期貨和貨幣市場價格顯示,未來 18 個月的所謂終端利率從未低於 2.85%,即使是在週一市場動盪最嚴重的時候。這與目前 5.38% 的政策中值利率相差甚遠。

但這仍高於美聯儲政策制定者所認為的長期 “中性” 利率水平——被廣泛視為既不刺激也不抑制經濟活動的利率水平 R*。在今年被美聯儲官員推高 30 個基點之後,被視為中性利率的美聯儲長期利率預測中值為 2.8%。

利率市場甚至可能根本沒有反映出深度衰退的影響。因此,如果焦慮的貨幣市場不認為美聯儲將被迫降息至低於這一水平,那麼未來的美國經濟放緩應該就不會那麼糟糕——儘管最近幾天出現了衰退擔憂。至少,這表明市場對經濟衰退仍持模稜兩可的態度,認為取消 “限制性” 政策本身可能就足以守住底線。

雖然這可能突顯出投資者對粘性通脹的擔憂揮之不去,但更可能反映出他們對某種深度衰退實際上正在醖釀的懷疑。數據表明,市場認為美聯儲只需把腳從剎車上移開,就能保持擴張勢頭。美國勞動力市場確實正在走弱,但是經濟並沒有陷入困境——美國第二季度 GDP 摺合成年率增長 2.8%。

即使按市場目前預期降息,實際利率也未低至緊急救濟的 “負水平”

另一種看該問題的方式是考慮經通脹調整後的美聯儲 “實際” 政策利率,目前為 2.5%。這是 17 年來的最高水平。自 2023 年 4 月以來,隨着反通脹進程的開始,實際政策利率從零穩步上升。

如果美聯儲的整個寬鬆週期被證明是如本週市場所暗示的降息 250 個基點,而消費者價格通脹在此期間將保持在 3% 的高位,那麼實際政策利率會回到零水平。而過去 15 年的平均實際政策利率為-1.4%,因此迴歸到零並不意味着美聯儲正走向緊急模式。

美聯儲官員本週的講話暗示,他們還不太擔心經濟衰退,但在政策方面,一切仍在討論之中。他們還堅稱,他們將繼續逐個會議進行評估,一個月的數據或市場動盪不會過度改變他們的想法。舊金山聯儲主席戴利表示,美聯儲 “準備在明確經濟需要的情況下,採取經濟需要的措施。”

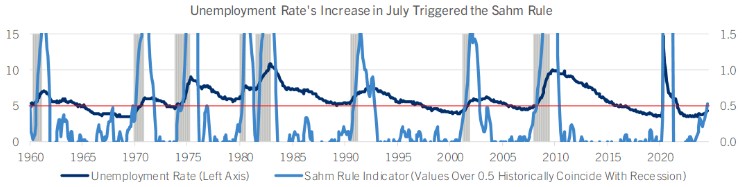

引發衰退言論的部分原因是上週非農數據中失業率觸發了所謂的 “薩姆規則”(Sahm Rule),該規則假定,3 個月平均失業率比 12 個月低點上升 0.5 個百分點,通常預示着衰退。但即使是該規則的作者、前美聯儲經濟學家克勞迪婭•薩姆 (Claudia Sahm) 也淡化了最新的觸發因素,因為疫情和天氣相關的季節性因素仍困擾着就業數據。

美國經濟目前正在放緩至更可持續的水平,近期經濟衰退並不是最可能的道路。然而,隨着勞動力市場的疲軟,美聯儲似乎仍將在 9 月份降息——這一舉措也將伴隨着政策制定者公佈最新季度預測,包括長期中性利率。

景順策略師 Kristina Cooper 認為:"美聯儲上週沒有降息是個錯誤,但我不認為這將對經濟造成無法彌補的損害。股市的拋售是一種非常情緒化的市場反應,高估了經濟衰退的可能性。”