AI enters the "liquid cooling era," the market underestimates the "degree of transformation," and the domestic supply chain is accelerating its entry

Institutional views point out that AI has spawned a liquid cooling super cycle worth 220 billion yuan, and the market has generally underestimated the speed and scale of this transformation. Technically, cold plates and microchannel lids (MCL) will divide the market; in terms of structure, NVIDIA's supply chain strategy of "delegation" is opening a historical window for domestic manufacturers to enter the global core supply chain. According to estimates, by 2026, the demand for liquid cooling systems on the NVIDIA platform will reach 69.7 billion yuan, and the demand for ASICs will reach 35.3 billion yuan, with the domestic supply chain accelerating to seize this trillion-yuan cake

As AI chip power consumption enters the "kilowatt era," a revolution surrounding cooling is quietly accelerating, with liquid cooling rapidly transforming from an "optional" choice to a "necessary" option for data centers.

According to a comprehensive in-depth report recently released by UBS and Soochow Securities, the market seems to have yet to fully digest the disruptive nature of this transformation. The report clearly points out that the market generally underestimates the speed and scale of the transition to liquid cooling, which is not just an ordinary hardware upgrade but a "timely and strategically necessary move" driven by fierce competition in AI chips.

This structural shift will not only give rise to a super cycle worth up to $31.191 billion (approximately RMB 220.523 billion) but will also reshape the global supply chain landscape, particularly opening the door for domestic manufacturers to enter the core system.

"Thermal Wall" Approaches: As Air Cooling Reaches Its Limits, Liquid Cooling is Set to Explode

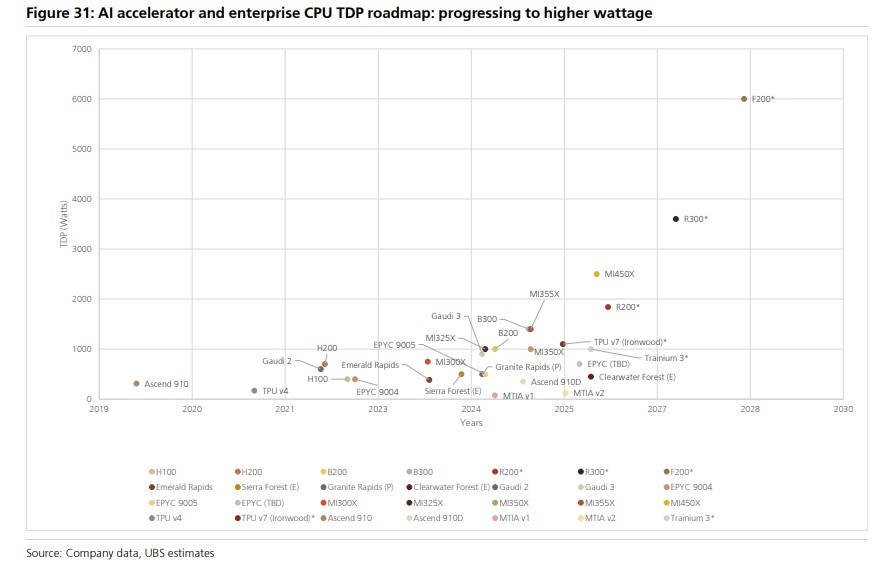

The explosive growth of AI computing power is pushing chips toward a "thermal wall." According to the reports from UBS and Soochow Securities, the thermal design power (TDP) of AI accelerators is rising at an astonishing rate.

NVIDIA's GPU product roadmap clearly illustrates this trend: from 700W for the H100, to 1200W for the Blackwell B200, to an expected 1800W-2300W for the VR200 launching next year, and potentially exceeding 3600W for the VR300 by 2027, with future Feynman platforms possibly reaching 5000W-7000W in power consumption.

The surge in chip power consumption directly leads to a dramatic increase in cabinet power density. A GB200 NVL72 cabinet's power has reached 120-140kW, while the future VR300 NVL576 cabinet's power consumption may exceed 600kW, even approaching 1MW.

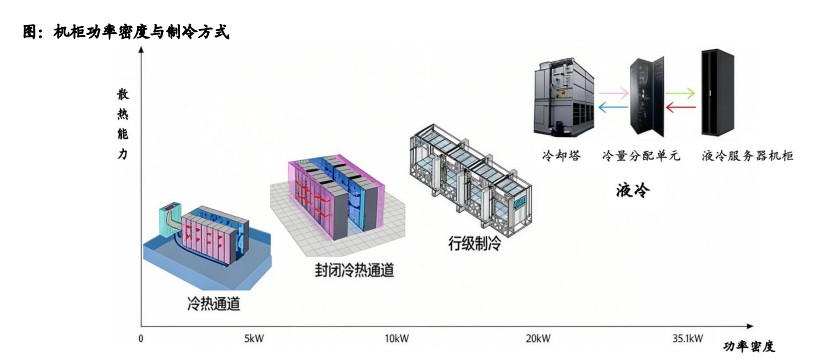

Traditional air cooling technology, which consists of computer room air conditioning (CRACs/CRAHs) systems made up of fans and heat sinks, has been the standard configuration for data centers for decades. However, when cabinet power density exceeds 30-40kW, air cooling reaches its limits due to the physical characteristics of low thermal conductivity of air.

The UBS report also points out that the efficiency and economy of traditional air cooling become unsustainable when cabinet power density exceeds 30-40kW.

At the same time, policies are also "pushing the wave." The Soochow Securities report mentions that countries like China are increasingly stringent on the PUE (Power Usage Effectiveness) requirements for data centers, aiming to reduce PUE to below 1.3 by 2025. Liquid cooling technology, with its excellent energy-saving effects (capable of reducing PUE to below 1.2) and lower total cost of ownership (TCO), has become an inevitable choice to meet policy requirements and achieve economic benefits Liquid cooling technology refers to the use of a liquid's specific heat capacity and thermal conductivity, which are far superior to that of air, to transfer heat. A report from Soochow Securities indicates that under the same unit conditions, the cooling capacity of liquid cooling is 4-9 times that of air cooling.

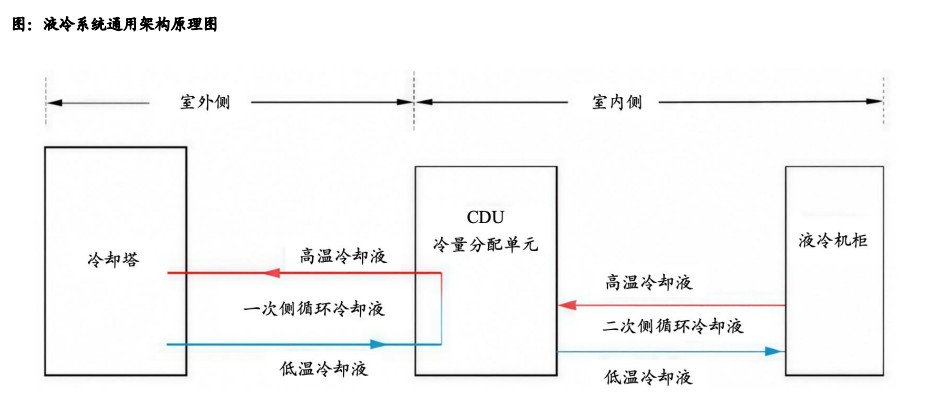

Cold Plate Liquid Cooling (DLC) is currently the most mature and widely applied solution. The coolant flows within a sealed cold plate (a metal plate with microchannels inside), which is in direct contact with heat-generating chips such as CPUs and GPUs, removing heat through indirect contact. Its advantages include strong compatibility with existing data center architectures and relatively low retrofitting costs.

Technological Route Differentiation: Cold Plate Maintains Mainstream, MCL Aims for the Future

In response to varying cooling demands based on power consumption, the liquid cooling market is clearly differentiating into two major technological camps. A UBS report points out that the future liquid cooling market will exhibit a distinct "bifurcating" pattern, with 3500W TDP as the dividing line.

For applications with power consumption below 3500W, Cold Plate technology will remain the backbone.

The UBS report believes that market concerns over the "commoditization" of cold plates and price wars are overstated. Although NVIDIA's standardization efforts may lead to a price drop of about 50% for GPU/CPU cold plates, this decline will be offset by the new liquid cooling demands from other components within the cabinet (such as NICs and DPUs). UBS analysis indicates that the overall value of cold plates in a fully liquid-cooled VR200 cabinet will only decrease by 1% compared to the GB300. The report predicts that by 2030, the cold plate market (excluding MCL) will reach $8.9 billion.

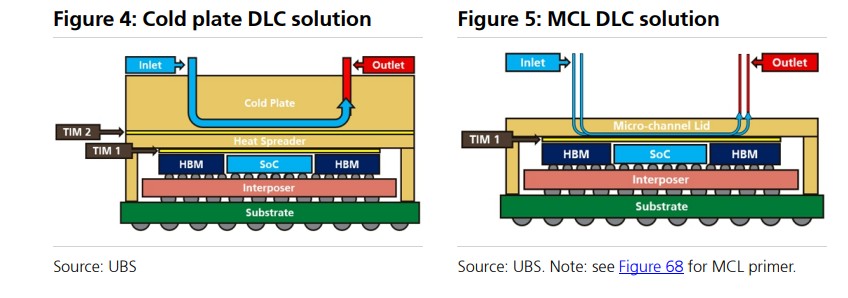

For future high-performance chips with power consumption exceeding 3500W, Micro-Channel Lid (MCL) will become the new standard.

This technology integrates coolant channels directly into the protective lid of the chip, eliminating the critical thermal resistance layer (TIM2) found in traditional solutions, achieving "in-package cooling." UBS boldly predicts that MCL technology may see limited adoption in the fourth quarter of 2026 with the overclocked version of the VR200 (2300W) and will become mainstream in the VR300 with a power consumption of 3600W. The report from Soochow Securities also believes that for the Rubin architecture, the MCL solution is more forward-looking than phase change cold plates and is better suited for the higher power consumption of future Rubin Ultra (4000W+). UBS expects the MCL market size to reach $1.25 billion by 2027 and grow to $2.7 billion by 2030.

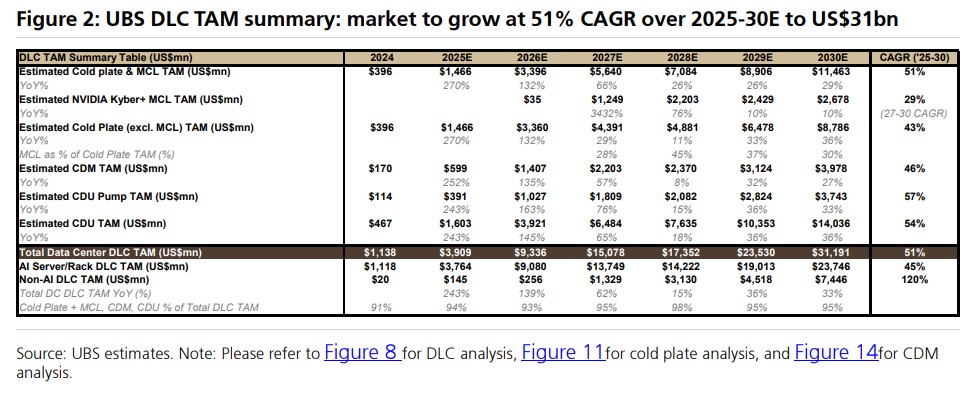

220 Billion Yuan Super Cycle: Market Size and Value Rise Together

UBS provided a stunning forecast in its report: The global direct liquid cooling (DLC) market for data centers is expected to soar from USD 1.138 billion in 2024 to USD 31.191 billion by 2030, with a compound annual growth rate (CAGR) of 51% (approximately RMB 220.523 billion).

The core driver of this growth is the doubling of the liquid cooling value per rack. UBS's calculations show that the liquid cooling value of an NVIDIA GB200 NVL72 rack is approximately USD 74,000, and by 2030, this figure is expected to quadruple to nearly USD 400,000.

Soochow Securities' calculations also confirm the trend of increasing value, pointing out that the value increase of the liquid cooling module exceeds 20% when upgrading from GB200 to GB300.

UBS further broke down the market composition, predicting that by 2030, the AI server liquid cooling market will reach USD 23.7 billion, while the non-AI server liquid cooling market will also grow to USD 7.4 billion. This indicates that the liquid cooling revolution is spreading from the AI sector to the entire data center industry.

NVIDIA's "Empowerment": Domestic Supply Chain Welcomes Historic Opportunities

In addition to the evolution of technology and markets, investors are also paying attention to the reshaping of the supply chain landscape. Soochow Securities' report keenly captured a key change: NVIDIA's supply chain strategy is shifting from "exclusive delivery" to "open ecosystem."

The report analyzes that during the A50/H100 era, NVIDIA adopted a "designated sole supplier" model for key components such as CDU (Cooling Distribution Unit) to ensure rapid delivery, with Vertiv being the only certified CDU supplier for GB200. However, as we enter the GB300 and future Rubin era, NVIDIA has begun to "empower," providing only reference designs and interface specifications, allowing ODMs (Original Design Manufacturers) like Quanta and Foxconn to independently choose suppliers in the external cabinet segment.

This shift is significant. It breaks the original closed supply system, opening the door for more manufacturers with technological and cost advantages to enter the NVIDIA ecosystem. Soochow Securities points out that domestic supply chain manufacturers are expected to seize this opportunity to indirectly enter as secondary suppliers or, with progressively mature products and cost-performance advantages, directly become primary suppliers within the NVIDIA system.

Specifically, this "empowerment" behavior breaks the monopoly of a single supplier. Soochow Securities analyzes that this provides two key entry paths for the domestic supply chain:

-

Secondary supply indirect entry: Domestic manufacturers can indirectly enter NVIDIA's supply chain system by supplying goods to ODM manufacturers such as Quanta and Foxconn.

-

Primary supply direct entry: With the maturity of domestic liquid cooling system technology and the improvement of cost-performance advantages, it is expected to directly enter NVIDIA's supplier list as a primary supplier in the future.

According to estimates from Soochow Securities Co., Ltd., the scale of liquid cooling systems required for ASIC chips will reach 35.3 billion yuan in 2026, while the scale required for NVIDIA's platform will be as high as 69.7 billion yuan. This huge market opportunity is becoming accessible due to the openness of the supply chain.

Currently, Taiwanese ODM manufacturers dominate the assembly of AI servers (according to Morgan Stanley data, Foxconn accounts for about 60% of GB200 shipments), and their influence in supply chain selection has consequently increased.

Domestic liquid cooling-related companies, such as those already laid out in areas like piping, precision structural components, and temperature control modules, are facing an unprecedented historic opportunity and are expected to share a piece of the pie in this billion-level liquid cooling wave