Wall Street comments on Oracle's earnings report: Appears to exceed expectations, but profits are "inflated"; investment logic has shifted from "looking at orders" to "looking at fulfillment"

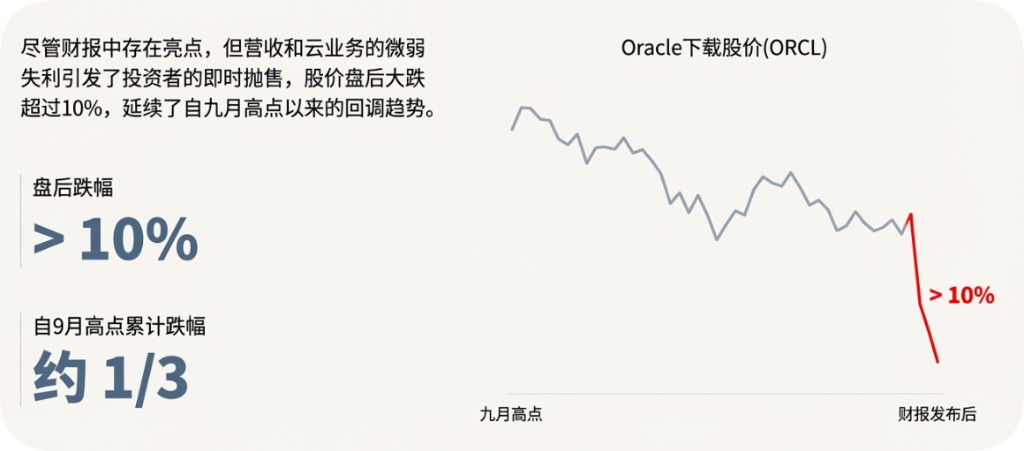

甲骨文財報引發華爾街熱議:儘管非 GAAP EPS 大幅超預期、5230 億美元訂單積壓創新高,但真實利潤被 27 億美元一次性收益 “拔高”,核心盈利與現金流承壓。訂單增長難掩轉化焦慮,雲業務增速不及預期,資本開支暴漲導致自由現金流轉負。財報後股價急跌 10%,瑞銀、美銀下調目標價,大摩將評級置於審查,市場關注點已轉向盈利質量與訂單兑現度。

甲骨文 2026 財年第二季度財報引發華爾街熱議:表面上非 GAAP 每股收益超預期、5230 億美元訂單積壓(RPO)再創新高,實則利潤依賴非經常性收益 “虛胖”。投資者已不再滿足於單純的 “訂單故事”。

財報發佈後,甲骨文盤後重挫超 10%。據追風交易台消息,這導致包括瑞銀、摩根士丹利和美銀在內的多家投行紛紛下調目標價或重新審視其評級。

大摩 Keith Weiss 團隊在 11 日的報告中表示,鑑於積壓訂單轉化為利潤的確定性下降,市場擔憂加劇,該行已將甲骨文的目標價和模型置於審查之中。甲骨文目前的股價缺乏明確催化劑,投資者需要更多證據證明其新興的 GPUaaS 業務能夠促進盈利和自由現金流增長。

瑞銀 Karl Keirstead 團隊認為,儘管甲骨文第二財季業績略遜於投資者預期,且融資槓桿前景的信息傳遞不夠明確,但鑑於其鉅額交易積壓訂單在下半年及 2027 財年的轉化潛力極具吸引力,瑞銀仍維持對該公司的 “買入” 評級。

美銀 Brad Sills 團隊則較為樂觀地表示,儘管甲骨文正處於 AI 基礎設施建設最繁重的階段,且面臨支出擴增與收入轉化的時間錯配,但這屬於投資曲線問題而非基本面變化,因此重申對該公司的 “買入” 評級。

訂單神話下的隱憂:5230 億 RPO 難掩轉化焦慮

甲骨文本季度交出了史上最強訂單成績單:RPO 新增 677 億美元至 5230 億美元,隱含訂單額同比激增 583% 至 838 億美元,核心驅動力來自 Meta、英偉達等巨頭的 AI 算力採購。其中,當前可確認的 cRPO 達 531 億美元,同比增長 40%,顯示短期訂單落地具備一定支撐。

但華爾街的關注點已從 “訂單增長” 轉向 “轉化效率”。

大摩指出,儘管訂單規模持續膨脹,但投資者正失去對其轉化為 “可持續盈利收入” 的信心。數據顯示,本季度總營收同比增長 13%(固定匯率),略低於市場預期;雲基礎設施(OCI)收入 40.79 億美元,同比增長 66%,低於瑞銀 68% 的預測與市場共識的 41.68 億美元;軟件業務收入同比下滑 3%,成為拖累整體增長的短板。

瑞銀則認為,訂單轉化滯後是行業共性,甲骨文 Abilene 數據中心建設按計劃推進,預計第三季度 OCI 增速將加速至 80% 以上。

但大摩警示,銷售團隊全球重組可能引發執行風險,而 “客户自供芯片”(BYOC)等靈活合約模式,雖能降低甲骨文資本開支壓力,卻可能削弱其 GPU 銷售環節的利潤空間,進一步加劇轉化盈利性的不確定性。

利潤 “虛胖” 真相:非經常性收益掩蓋核心承壓

本季度甲骨文財報最顯著的矛盾,在於 “超預期 EPS” 與 “疲軟盈利能力” 的背離。

財報顯示,非 GAAP 每股收益達 2.26 美元,大幅超出市場預期的 1.65 美元,但這一亮眼表現並非來自核心業務改善。

大摩拆解發現,EPS 超預期主要得益於 27 億美元的税前非經常性收益——甲骨文出售其在 Ampere 的股權所得。剔除該因素後,其核心盈利能力實則全面承壓:非 GAAP 毛利率同比大幅下滑 470 個基點至 41.9%,遠低於市場預期的 68.7%;非 GAAP 運營利潤率同比下滑 150 個基點,同樣不及 42.2% 的 consensus 預期。

盈利能力弱化的核心原因是資本開支的激增。本季度甲骨文資本開支達 120 億美元,同比暴漲 200% 以上,遠超瑞銀 92 億美元、大摩 84 億美元的預測,直接導致自由現金流轉負至-100 億美元。管理層將 2026 財年資本開支目標上調 150 億美元至 500 億美元,相當於全年預期營收的 75%,高投入與慢轉化的時間差,進一步擠壓了短期利潤空間。

美銀將此定性為 “投資週期錯配”,而非基本面惡化,強調資本開支是為匹配 AI 算力需求的必要投入。

但大摩擔憂,隨着 AI 產業 “軍備競賽” 加劇,頭部企業資本開支持續高增,若甲骨文無法快速實現規模效應,毛利率可能進一步承壓,進而影響長期盈利模型。

估值邏輯重構:目標價集體下調,催化劑轉向盈利驗證

財報發佈後,華爾街對甲骨文的估值邏輯發生根本性轉變,從 “溢價反映訂單潛力” 轉向 “折價應對兑現風險”。三家投行均下調目標價,反映對其增長確定性與盈利質量的重估。

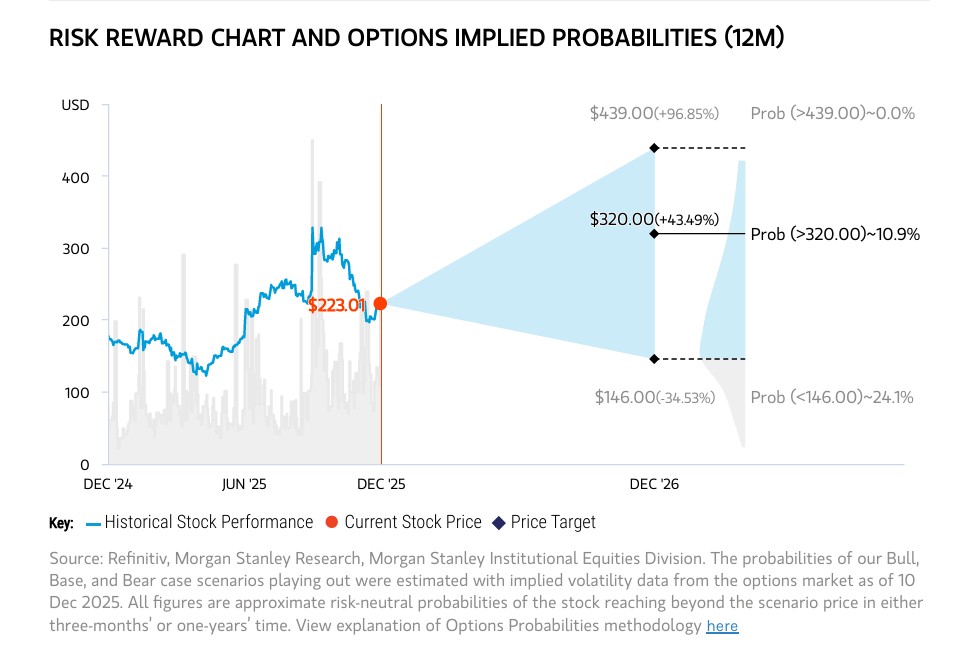

瑞銀維持 “買入” 評級,但將目標價從 380 美元下調至 325 美元,估值基礎從 2027 財年 44 倍 PE 降至 37 倍,理由是短期業績不及預期與融資前景的不確定性。美銀同樣保留 “買入” 評級,目標價從 368 美元下調至 300 美元,估值錨從 12.4 倍 2027 財年 EV/銷售額,調整為 10 倍,契合當前 AI 板塊整體估值收縮的趨勢。

大摩則採取更謹慎態度,宣佈將其評級與目標價納入 “重審”,成為三家投行中唯一未維持原有評級的機構。其核心顧慮在於,投資者對訂單轉化、毛利率走勢、現金流改善的信心持續弱化,而這些不確定性在高利率環境下可能被進一步放大,若缺乏明確的盈利改善催化劑,當前 28 倍 2026 財年 PE(與微軟、亞馬遜持平)的估值水平可能缺乏支撐。

估值分歧的本質,是對甲骨文 “AI 轉型成色” 的判斷差異。

瑞銀、美銀仍看好其 5230 億 RPO 的長期兑現潛力,認為當前估值已反映短期壓力,隨着第三季度 OCI 增速加速、訂單轉化落地,股價仍有修復空間。

但大摩強調,市場需要更明確的信號:無論是加速的營收增長、企穩的毛利率,還是轉正的自由現金流,只有核心指標出現實質性改善,才能重建對其 AI 算力業務盈利性的信心。