Fu Peng: High attention! How does the significant rise in global long-term bond yields affect the trading of major asset classes?

Fu Peng analyzed the significant rise in long-term bond yields in major developed countries globally in Season 6 of "Fu Peng Says," particularly focusing on the 10-year and 30-year government bonds. The increase in long bond yields is notably evident in countries such as the UK, Germany, Australia, and Japan, while the rise in the United States is relatively slower. The expansion of fiscal deficits in European countries, Japan, and Australia is the core reason for the increase in long bond yields, leading to a substantial rise in term premiums

"Looking at the world from the trading desk, Eric Wu discusses finance"

"Eric Wu Discusses - Season 6" has been fully upgraded! Subscribe now

This year marks the tenth anniversary of Wall Street Insights' annual column "Eric Wu Discusses"!

"Eric Wu Discusses - Season 6" has been fully upgraded. In addition to the daily videos, a new column group chat has been added to update Eric Wu's latest market insights & chart data interpretations (community updates in real-time).

In addition to the daily content of Eric Wu Discusses, an online reading document for the column has been added, providing daily trading focus morning reports, noteworthy research reports, recommended electronic reading lists, and extended reading materials. Everyone is also encouraged to ask questions and communicate in the community for mutual improvement. Users who join the column can scan the QR code below to add the assistant and enter the exclusive group chat for "Eric Wu Discusses".

Highly Concerned! How does the significant rise in global long-term bond yields affect major asset trading?

Looking at the world from the trading desk, Eric Wu discusses finance.

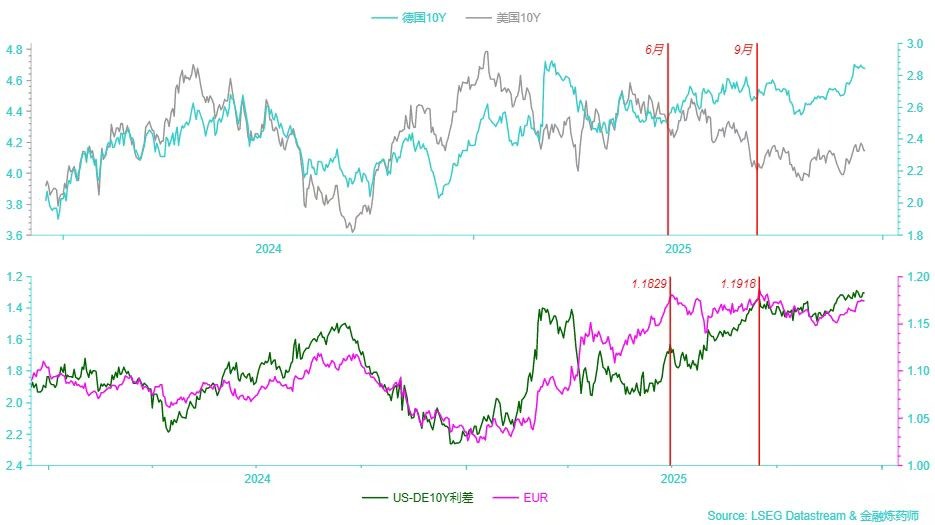

Long-term bond yields in major developed countries have seen a significant rise, especially in 10-year and 30-year government bonds. The increase in long-term bond yields in countries like the UK, Germany, Australia, and Japan is particularly notable, while the rise in U.S. long-term yields has been relatively slower. For example, after June, the spread between U.S. and German 10-year bonds has further narrowed, while the euro has remained oscillating around the upper limit of 1.18-1.19, with a range of about 1.15-1.19. The acceleration of German long-term bond yields compared to U.S. 10-year bonds is a major factor recently, and the differences in long-term rates between the U.S. and Germany reflect two distinct reasons.

The continuous expansion of fiscal deficits in European countries, Japan, and Australia is the core driver of rising long-term bond yields. Following the recent budget proposal, market concerns about the sustainability of the UK's debt have intensified, leading to a rapid rise in gilt yields; although Germany maintains relatively strict fiscal discipline, significant increases in defense, infrastructure, and energy transition spending have broken the traditional "debt brake" constraints; as a major commodity exporter, Australia's fiscal space is affected by fluctuations in global demand, resulting in rising deficit pressures; Japan has launched a new round of stimulus plans, directly pushing the 30-year government bond yield to multi-year highs. These countries share the common characteristic of increased debt supply, while demand has not kept pace, leading to a substantial rise in term premium. The term premium essentially compensates investors for the additional risks of holding long-term bonds, and when the fiscal path deteriorates, this premium quickly manifests as rising yields The market's skepticism about the actual effects of fiscal stimulus has further amplified this pressure. Many analysts believe that the current stage of fiscal expansion has limited pull on the real economy—diminishing marginal returns, structural bottlenecks, and a high interest rate environment have weakened the multiplier effect. However, even if the stimulus fails to significantly boost growth, the debt/GDP ratio continues to rise. This situation of "spending money without effect, yet leaving behind greater debt" has triggered dual concerns among investors: on one hand, worries about weakening growth prospects, and on the other, greater concerns about debt sustainability. As a result, risk pricing has dominated the bond market, with term premiums replacing economic growth expectations as the main driver of yields. Particularly in countries like the UK and Japan, where existing debt levels are already very high, the market is extremely sensitive to rating downgrades or fiscal mismanagement, with any slight disturbance triggering sell-offs.

In contrast, for the United States, with the current explosion in productivity, investor confidence in its debt sustainability is significantly higher than in other countries. The market pricing of U.S. fiscal risk is relatively mild, with the rise in term premiums being smaller than that in Europe and Japan. Additionally, the U.S. economy shows greater resilience, inflation, while sticky, has not spiraled out of control, and the Federal Reserve has more policy space. These factors collectively suppress a sharp rise in U.S. Treasury yields, leading to a clear divergence in yield trends compared to countries like the UK and Germany.

This explains why we see currencies like the euro, yen, and Australian dollar, which, despite seemingly narrowing interest rate differentials (with long-term rates rising faster than in the U.S.), can only oscillate sideways (yen, euro, Australian dollar) and do not strengthen against the dollar as interest differentials improve.

In short, fiscal policy can lead to increased productivity that generates real profits, which means an upward shift in the overall interest rate center and a stronger currency; otherwise, it leads to fiscal concerns, putting pressure on stocks, bonds, and currencies, and at this time, interest differentials will not drive currency appreciation.

Risk Warning and Disclaimer

The market has risks, and investment requires caution. This article does not constitute personal investment advice and does not take into account the specific investment goals, financial conditions, or needs of individual users. Users should consider whether any opinions, views, or conclusions in this article align with their specific circumstances. Investing based on this carries responsibility