Bullish to $150 in the coming weeks! Citigroup shouts that silver is "gold on steroids," led by China with India following suit

Citi believes that silver is not the "shadow" of gold, but rather the "square term" of gold. During this round of increases, the premium of Shanghai silver over London has significantly risen and remains at historically high levels, while the premium of Indian silver has also seen a rare rebound recently. Assuming that the gold price operates within a range of USD 5,100–5,400 per ounce, Citi has raised its silver price target for the next 0–3 months to USD 150 per ounce

As the precious metals market is in a frenzy, Citigroup is set to "max out" its short-term judgment on silver.

According to the Chase Trading Desk, on January 27, Citigroup Research significantly raised its silver price target for the next 0-3 months from $100 per ounce to $150 per ounce in its latest report, "MetalMatters." This $100 target was only given two weeks ago, and the current silver price has quickly surpassed the $110 mark.

Citigroup bluntly stated that at this stage, silver's performance is no longer "following gold," but rather resembles "gold on steroids."

From "precious metal" to "capital allocation asset," silver is replicating gold's pricing logic

Citigroup believes that the core driving force behind the current silver market rally is not traditional industrial demand or supply contraction, but rather the full activation of capital allocation logic.

Similar to gold, silver is being viewed by global funds as an asset to hedge against macroeconomic uncertainty, a tool to hedge against geopolitical risks, and a pricing vehicle for the risk of "damaged Federal Reserve independence."

However, unlike gold, silver possesses greater elasticity and stronger price acceleration.

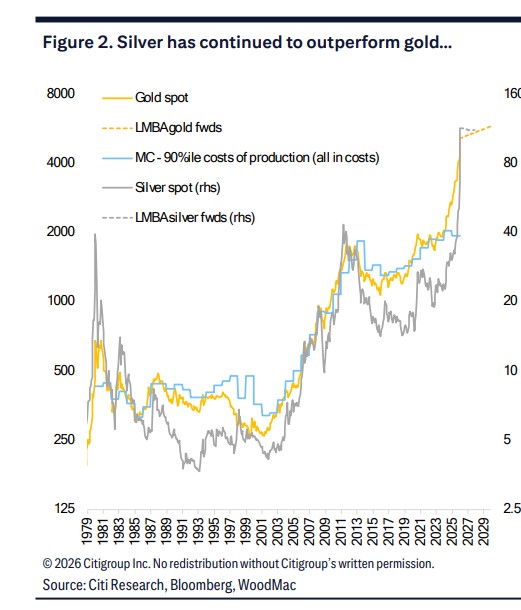

In the past two weeks, gold prices have risen about 10%, while silver has surged over 30%. Citigroup vividly describes it as: silver is not a "shadow" of gold, but rather the "square term" of gold.

The "engine" of this silver bull market: China leads, India follows

Citigroup clearly points out that the current "doubling" of silver prices since December shows a highly distinct regional characteristic: China is the leading force, with India and global retail demand following.

Several key signals are particularly noteworthy:

- The premium of Shanghai silver over London has significantly risen and remains at historically high levels, clearly reflecting the strong physical and investment demand in China;

- The premium for silver in India has also recently shown a rare rebound—historically, India usually buys heavily only at low prices and remains restrained at high prices;

Citigroup notes that the simultaneous emergence of "chasing demand" in both China and India, against the backdrop of significantly rising prices, is an important feature of this silver bull market.

Policy cooling cannot stop the trend: Retail investors resemble CTAs rather than "fearful funds"

In response to market concerns about "regulatory intervention," Citigroup's judgment is quite clear: the trend is unlikely to change in the short term.

Recently, several "cooling measures" have emerged in the Chinese market, including: the suspension of new subscriptions for China's only silver ETF and the previous increase in silver futures margin ratios by the Shanghai Futures Exchange.

However, Citigroup believes that these measures affect trading rhythm more than trend direction.

The reason is that the behavior pattern of Chinese retail investors is more akin to trend-following CTAs rather than value-reversion investors.

In a strong momentum and strong trend market environment, as long as silver is not considered "outrageously expensive" relative to gold, funds tend to continue to increase positions in line with the trend, further tightening the supply-demand balance in the physical and circulation layers

The Market Where Fundamentals Have "Failed": ETF Outflows and Decreased Holdings Cannot Stop the Rise

An intuitive yet highly significant phenomenon is that the surge in silver prices has occurred against the backdrop of multiple traditional "bearish indicators," including:

COMEX silver inventories have seen outflows of about 100 million ounces since October last year.

Global (excluding China) silver ETF holdings have net outflows of about 270 million ounces since December.

CFTC data shows that some managed funds have taken profits during the price increase.

Under traditional frameworks, these signals should suppress prices. However, the reality is that macro risk premiums + Chinese retail demand have completely overshadowed these effects. Citigroup bluntly states that many traditional supply-demand and holding models have "failed" at this stage.

How High Can Silver Go? It Depends on the "Gold-Silver Ratio" as a Measure

In a highly speculative market, Citigroup chooses to use the gold-silver ratio as an important reference for determining the upper limit.

Assuming the gold price operates within the range of $5,100–$5,400 per ounce:

If the gold-silver ratio falls back to the 2011 low of about 32 times, the silver price could reach $160–$170 per ounce.

In an extreme case, if it returns to the post-Bretton Woods low of about 14 times in 1979, the theoretical price range would point to over $300.

Citigroup emphasizes that the latter scenario is "extremely unlikely," but it clearly indicates that from a historical relative pricing perspective, the "imagination space" for silver has not yet reached its ceiling.

Conclusion: This is a Silver Revaluation Driven by Capital and Behavior

Overall, Citigroup's judgment on the silver trend in the coming weeks is highly clear: maintain a tactical bullish stance, with the 0–3 month target price raised to $150 per ounce.

The core drivers come from: macro and geopolitical risk premiums, China-led retail and physical demand, which relative to silver's historical pricing are still not "overly expensive."

However, Citigroup also warns that the period before the Chinese New Year may become a risk window for short-term profit-taking in silver, with about two weeks remaining until the festival at the time of the report's release. The macro and capital factors supporting the rise in silver are still expected to continue in the short term.

In Citigroup's view, this is not a market of "precise calculations of supply-demand balance," but rather a re-pricing process of precious metals shaped by capital preferences, risk pricing, and collective behavior