At least nine Chinese AI chip companies have shipments exceeding 10,000 units

在严格的芯片出口管制下,中国 AI 芯片的自主化进程加速,至少九家公司的出货量或订单量已超过 1 万卡,包括华为、百度等大厂及多家创业公司。国产 AI 芯片的市场份额迅速攀升,预计到 2025 年上半年市场规模将达 160 亿美元,国产芯片占 35% 市场份额。随着代工产能提升,出货量将迎来爆发式增长,但竞争仍在继续,进入规模化交付验证阶段。

在严格的芯片出口管制的倒逼下,国产数据中心 AI 芯片的自主化进程正在加速。目前,国产 AI 芯片包括华为昇腾、百度昆仑芯、阿里平头哥、寒武纪等十余个品牌。

《财经》多方调研获悉,至少有九家中国 AI 芯片公司的出货量或订单量已超过 1 万卡。其中包括华为昇腾、百度昆仑芯等背靠科技大厂的企业,还包括寒武纪、沐曦、天数智芯、燧原科技等 AI 芯片上市和将上市企业,甚至包括曦望(Sunrise)、清微智能等仍在创业阶段的非上市公司。

其中出货规模大的 AI 芯片公司,累计出货量已在 10 万卡级别。出货量相对较小的 AI 芯片公司,如曦望、清微智能等 2025 年出货量或订单规模在 1 万卡以上。

国产推理 AI 芯片单价目前单卡价格约在 3 万-20 万元不等。出货量或订单量达到万卡规模,意味着国产 AI 芯片的性能、稳定性和总拥有成本具备一定市场认可度。它开启的不只是规模竞争,更是围绕稳定性、软件生态和商业化服务的更深层次、更全方位的竞争。

一批大大小小的 AI 芯片公司出货规模快速增长,国产 AI 芯片的市场份额因此迅速攀升。

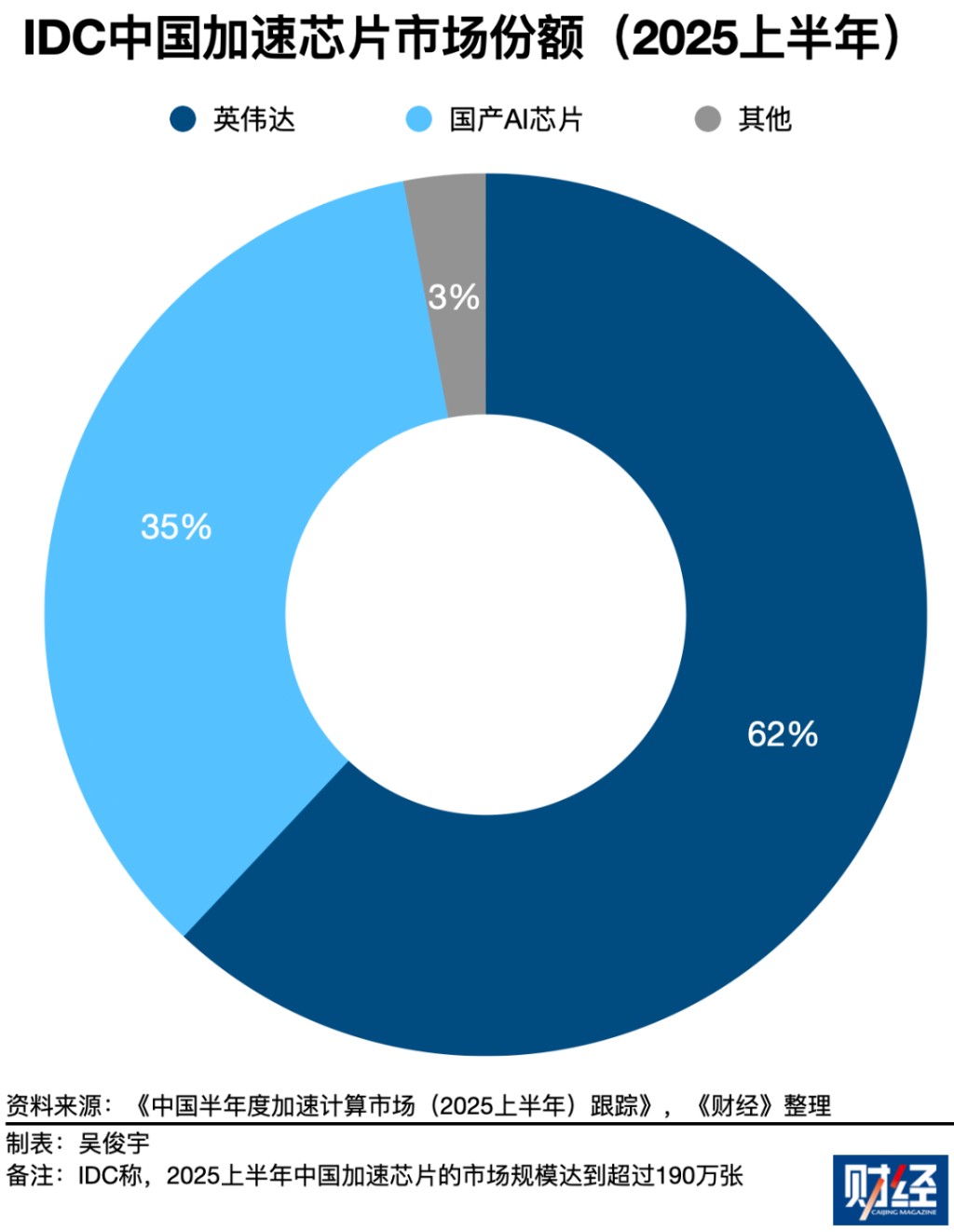

国际市场调研机构 IDC 2025 年 10 月数据显示,2025 年上半年中国加速(即 AI 芯片)服务器市场规模达到 160 亿美元,出货超过 190 万张。其中英伟达约占 62% 市场份额,国产 AI 芯片约占 35% 市场份额。国产 AI 芯片需求持续增长,增长速度远超英伟达。

多位半导体产业人士对《财经》表示,2026 年随着国产 AI 芯片的代工产能逐渐提升,国产 AI 推理芯片的出货量还将迎来一轮爆发式增长。

不过,万卡级出货量企业的批量出现,并不意味着国产 AI 芯片的竞争已经分出胜负,而意味着这一轮产业试错开始进入 “规模化交付验证” 阶段。

万卡出货量的中国 AI 芯片公司涌现

万卡级别出货量的国产 AI 芯片公司正在批量涌现。

华为昇腾、百度昆仑芯是出货规模最大的国产 AI 芯片。它们背靠大型科技公司,有稳定的客户。华为昇腾、百度昆仑芯性能表现突出,甚至已被用于部分模型训练场景。

国际市场调研机构 IDC 数据显示,2025 下半年国产 AI 芯片中,华为昇腾市场份额位居国内第一,百度昆仑芯市场份额位居国内第三。

华为昇腾已经被用于电信运营商、科技公司的多个国产万卡集群。百度 2025 年 2 月点亮了昆仑芯 P800 万卡集群,并计划未来点亮三万卡集群。除了百度,一批金融、能源、制造等领域的大型企业都在采购百度昆仑芯。

寒武纪也是国内出货量最大的国产 AI 芯片之一。其主要客户包括国内大型互联网公司、电信运营商和金融机构等。

2025 下半年-2026 年初,沐曦、摩尔线程、天数智芯、燧原科技等 AI 芯片创业公司先后发布招股书。招股书显示,沐曦、天数智芯、燧原科技的累积出货量均已超过万卡。

沐曦招股书披露,截至 2025 年 8 月末,沐曦 AI 芯片累计销量超过 2.5 万卡,已在多个国家人工智能公共算力平台、电信运营商智算平台和商业化智算中心实现规模化应用。

天数智芯招股书披露,截至 2025 年 6 月 30 日,天数智芯已向金融、医疗、交通等行业的 290 名客户交付 5.2 万枚 AI 芯片。

燧原科技招股书披露,截至 2025 年 9 月,燧原科技 AI 加速卡及模组出货情况。经《财经》计算,燧原科技的 AI 加速卡及模组合计销量为 9.72 万张。

《财经》了解到,包括曦望、清微智能等仍未上市的国产 AI 芯片公司出货量或订单量也已经超过万卡。不过,它们和头部国产 AI 芯片公司的出货量仍存在明显差距。

曦望前身是商汤科技的大芯片部门,2024 年底分拆独立运营,该公司目前专注 AI 推理芯片的研发与商业化。曦望的投资方包括三一集团旗下华胥基金、范式智能、杭州数据集团,IDG 资本、高榕创投、无极资本等知名机构,以及诚通混改基金、杭州金投、杭州高新金投等国资相关基金。

曦望已经销售启望 S1、启望 S2 等 AI 推理芯片,2026 年将量产启望 S3 芯片。客户包括商汤科技、第四范式等企业。在 1 月 28 日产品发布会上,曦望方面披露 2025 年 AI 芯片交付破万卡,收入大幅增长。

清微智能是一家 “清华系” 的芯片创业公司。获得了国家集成电路产业投资基金(大基金)投资,且是首批国家级专精特新 “小巨人”。《财经》了解到,截至 2026 年 1 月,清微智能的 AI 推理芯片订单量累计超过至少 2 万卡,客户包括部分地方城市的智算中心。

一些国产 AI 芯片创业公司目前更关注能用、可控以及出货规模,并非追求极致的峰值性能。

部分国产 AI 芯片创业公司并未像英伟达和头部国产 AI 芯片公司使用 7nm(纳米)及以下的先进制程以及 HBM(高带宽内存)内存。目前国产 7nm(纳米)及以下的先进制程、国产 HBM 内存产能极其有限。因此,它们直接采用了更成熟且中国大陆本土产业链能够更快量产的 12nm 工艺制程和 LPDDR(低功耗双倍数据率内存)系列内存。这类国产 AI 芯片的价格甚至可低至 3 万元/卡。

2025 年 12 月,AI 基础设施创业公司新智惠想创始人吴健对《财经》表示,他和十家以上的国产 AI 芯片企业都有接触。他预计 2026 年-2027 年中国市场还会有多款国产 AI 推理芯片上市,2026 年-2027 年会迎来爆发。

部分国产 AI 芯片推理性能已超英伟达 H20

目前,国产 AI 芯片的峰值性能和英伟达存在巨大差距。中国市场的 AI 芯片数量和美国市场也存在巨大差距。

降低国产 AI 芯片的推理成本,正在成为中国产业界的共同努力方向。因为当算力规模无法正面比拼时,决定差距的不是有多少芯片,而是每张芯片能吐出多少 Token(词元)。

数据中心 AI 芯片的主要使用场景包括训练和推理。推理 AI 芯片的设计、使用门槛相对较低,这里是国产 AI 芯片突围的重要机会。IDC 数据显示,2025 年中国生成式 AI IaaS(基础设施)市场,训练占比 49.6%、推理占比 50.4%。IDC 预测,到 2029 年,训练占比将降至 23.3%,推理占比将提升至 76.8%。

因此,国产 AI 芯片公司普遍注重提升推理性能,“榨干” 每一枚芯片的 Token。Token 是模型推理的基本单位。当算力规模受限时,每秒能生成多少 Token(Token/s),直接决定了 AI 服务的响应速度、吞吐量和成本。这是衡量芯片实际推理效率的核心指标。

吴健表示,做好硬件适配、调度优化等工作,有可能将同样的芯片、同样的模型发挥出数倍甚至数十倍的 Token 吞吐性能。

曦望 CEO(首席执行官)徐冰 1 月 28 日在产品发布会表示,2025 年中国市场百万 Tokens 的推理成本已经降至 1 元。曦望的目标是在这个基础上用专用的推理芯片和系统架构,把百万 Tokens 的降低至 1 分级别。曦望相关人士对《财经》表示,目前曦望主打 AI 推理性能,下一代启望 S3 目标是,相比上一代产品 AI 推理性能提升十倍以上。

在门槛更低、使用更广泛的推理场景,部分国产 AI 芯片性能表现已接近或超过英伟达 H20。H20 是一款为了符合美国出口管制政策,性能被大幅阉割的 “中国特供” AI 芯片。

一位地方国企智算技术人士 2025 年 12 月曾对《财经》表示,他测试了华为昇腾 910B、百度昆仑芯 P800、阿里 PPU 等国产 AI 芯片的推理性能。百度昆仑芯 P800、阿里 PPU 跑 DeepSeek-R1 和阿里千问等经过适配优化的模型,Token 吞吐效率优于英伟达 H20。

不过,在软件生态层面,国产 AI 芯片目前普遍面临适配慢、适配难的问题。不像英伟达的芯片一样,能被开发者快速适配市面上大部分模型。

一位国产 AI 芯片创业公司人士对《财经》表示,他们目前主要适配 DeepSeek、阿里千问、Meta 的 Llama 系列等主流模型,其他模型无法及时、全面兼顾。上述地方国企智算技术人士对《财经》表示,他所在的企业为国产 AI 芯片适配新模型,通常要一两个月。因此,往往无法第一时间用上最新的模型。

一位人工智能解决方案公司 CEO 甚至提到,Hugging Face(全球 AI 和大模型开源社区)上拥有超过 200 万款模型,而某国产 AI 芯片适配的模型数量只有几十款。

多位半导体产业人士对《财经》表示,万卡级出货量企业的出现,意味着这一轮产业试错正在进入 “规模化交付验证” 阶段。部分半导体产业人士的看法是,国产 AI 推理芯片市场正在出现与光伏产业早期相似的路径——在产业政策,以及产业引导基金、二级资本市场的推动下,多家厂商出货量迅速攀升。

一种乐观预期是,中国的 AI 推理芯片市场未来几年,将像中国的光伏产业一样,通过激烈的市场竞争跑出若干个具备国际竞争力的企业。

不过,另一种观点是,光伏是高度标准化的制造业产品,胜负最终由成本曲线与产能效率出清决定。AI 芯片的产业发展逻辑由软件、硬件和生态共同决定,它的竞争节奏与淘汰机制和光伏产业存在本质差异。

国产 AI 芯片上游受限于芯片代工企业的产能,下游受限于软件生态。它的交付稳定性、软件栈成熟度与生态迁移成本,决定了 “万卡之后” 的复购与生存。中国 AI 芯片市场残酷的竞争甚至尚未真正开始。

风险提示及免责条款

市场有风险,投资需谨慎。本文不构成个人投资建议,也未考虑到个别用户特殊的投资目标、财务状况或需要。用户应考虑本文中的任何意见、观点或结论是否符合其特定状况。据此投资,责任自负。