Microsoft's cloud business growth slows, record high capital expenditures raise concerns, stock price falls about 5% after hours | Earnings Report Insights

微软第二财季业绩整体超出市场预期,营收、利润与每股收益均实现强劲增长,但公司资本支出同比大增 66%、创历史新高,叠加云业务增速较前一季度放缓,引发投资者对 AI 投入回报周期拉长的担忧,股价盘后下跌约 5%。

微软周三盘后公布第二财季财报显示,该公司季度资本支出飙升至历史新高,同时云业务销售增速放缓,引发投资者担忧其在人工智能领域的大规模投入可能需要比预期更长的时间才能见效,导致公司盘后股价下跌约 5%。

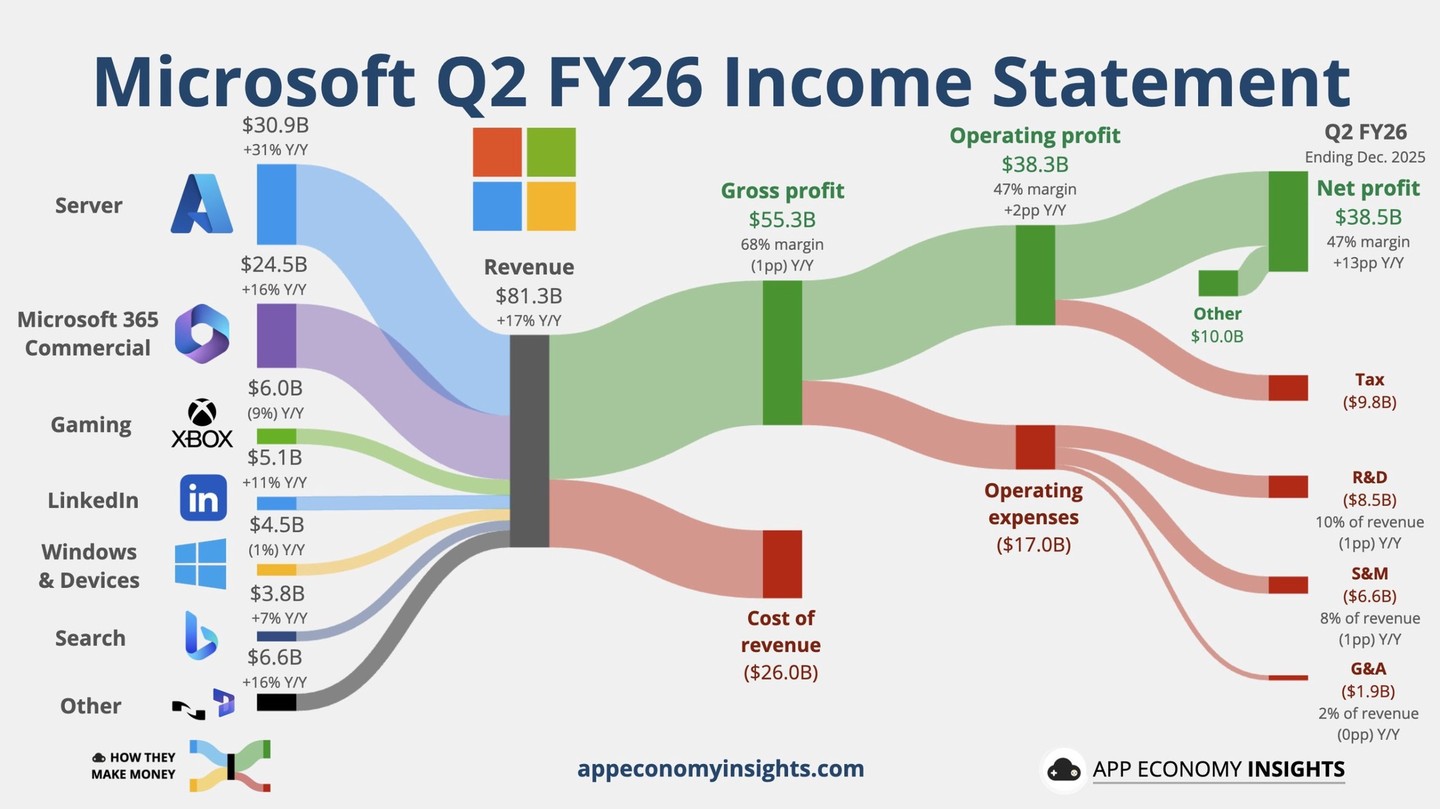

微软第二财季营收 812.7 亿美元,分析师预期 803.1 亿美元。 智能云营收 329.1 亿美元,预期 323.9 亿美元。

以下是微软财报要点:

主要财务数据:

营收:第二财季营收为 813 亿美元,同比增长 17%,高于分析师预期 803.1 亿美元。

营业利润:营业利润为 383 亿美元,同比增长 21%,同样高于分析师预期。

净利润:按 GAAP 口径计算,净利润为 385 亿美元,同比增长 60%;按非 GAAP 口径计算,净利润为 309 亿美元,同比增长 23%;按固定汇率计算,同比增长 21%。

每股收益:按 GAAP 口径计算,稀释后每股收益为 5.16 美元,同比增长 60%,高于分析师预期的 3.92 美元;按非 GAAP 口径计算,稀释后每股收益为 4.14 美元,同比增长 24%;按固定汇率计算,同比增长 21%。

资本支出:微软第二财季资本支出达到 375 亿美元,同比增长 66%,不仅创下纪录,也高于分析师预期的 362 亿美元。

分业务数据:

云业务:云业务营收为 515 亿美元,同比增长 26%;按固定汇率计算,同比增长 24%。商业剩余履约义务同比增长 110%,达到 6250 亿美元。

生产力与业务流程部门:营收为 341 亿美元,同比增长 16%;按固定汇率计算,同比增长 14%

- Microsoft 365 商业云收入同比增长 17%;按固定汇率计算,同比增长 14%。

- Microsoft 365 消费者云收入同比增长 29%;按固定汇率计算,同比增长 27%。

- LinkedIn 营收同比增长 11%;按固定汇率计算,同比增长 10%。

- Dynamics 365 营收同比增长 19%;按固定汇率计算,同比增长 17%。

智能云部门:营收为 329 亿美元,同比增长 29%,高于分析师预期的 323.9 亿美元;按固定汇率计算,同比增长 28%

- Azure 及其他云服务收入同比增长 39%;按固定汇率计算,同比增长 38%,符合分析师预期。

更多个人计算业务部门:营收为 143 亿美元,同比下降 3%。

- Windows OEM 及设备收入同比增长 1%;按固定汇率计算基本持平。

- Xbox 内容与服务收入同比下降 5%;按固定汇率计算下降 6%。

剔除流量获取成本后的搜索与新闻广告收入:同比增长 10%;按固定汇率计算,同比增长 9%。

微软董事长兼首席执行官萨提亚·纳德拉(Satya Nadella)表示:

“我们仍处在 AI 扩散的早期阶段,但微软已经打造出一个规模超过我们部分最大传统业务的 AI 业务。我们正在整个 AI 技术栈上持续推进前沿创新,为客户和合作伙伴创造新的价值。”

微软执行副总裁兼首席财务官艾米·胡德(Amy Hood)表示:

“本季度微软云业务营收突破 500 亿美元,反映出市场对我们服务组合的强劲需求。我们的营收、营业利润和每股收益均超出预期。”

由于公司披露的基础设施支出高于预期(包括数据中心建设),同时游戏业务相关销售表现不及预期,微软股价盘后下跌约 5%。

云业务增速不如人意

根据财报在剔除汇率因素影响后,Azure 云计算业务当季营收同比增长 38%,刚好符合分析师的预测。

不过,这一增速较上一季度放缓了 1 个百分点。DA Davidson 分析师吉尔·卢里亚(Gil Luria)表示,这样的放缓,或许已经足以让原本押注云业务表现更强劲的投资者感到失望。

分析师和投资者指出,微软 Azure 云业务的增长,仍主要由其核心的非 AI 云工作负载驱动。这些业务为企业提供数据和应用的存储、管理与处理服务。微软在相关建设上的资本支出达到 375 亿美元,高于分析师预期。

微软投资者关系主管詹姆斯·安布罗斯(James Ambrose)周三表示,基础设施支出的增加,反映出微软在 AI 相关和非 AI 工作负载方面,持续看到强劲的云需求。

Stifel 投资公司的分析师布拉德·里巴克(Brad Reback)表示,投资者非常关注 Azure 的增长速度是否能够跑赢支出增速,从而证明微软当前投入水平的合理性。

资本支出超预期引起不安

媒体称,部分投资者对微软及其他大型科技公司正在投入的巨额资金感到不安,因为企业正在大规模建设数据中心,但尚未充分证明 AI 需求能否持续,或最终是否具备盈利能力。过去六个月里,微软股价已下跌超过 6%。

微软正在建设大型、互联的数据中心网络,并将其称为 AI“超级工厂”,专门用于 AI 训练和相关工作负载。周一,微软还发布了一款新的 AI 推理芯片 Maia 200,公司称其在某些任务上的成本更低、速度更快,优于竞争对手的同类产品。

纳德拉上月在一篇博客文章中写道,目前 AI 能力的发展速度,已经快于其在现实世界中的实际影响。他上周在瑞士达沃斯举行的世界经济论坛期间也表达了类似观点,指出如果 AI 应用不能走出科技行业、实现更广泛落地,可能会引发金融泡沫风险。

微软正在推动其 Copilot AI 聊天机器人获得更广泛的使用,但在竞争中仍落后于谷歌和 OpenAI 等领先对手。微软此前大量依赖 OpenAI 模型来驱动 Copilot 工具,而近期则开始进行多元化布局,在编程以及 Microsoft 365 生产力产品中,引入了初创公司 Anthropic 的模型。微软在财报电话会上表示,企业客户已采购 1500 万份 Copilot 许可。

去年 11 月,微软表示将向 Anthropic 投资至多 50 亿美元,而 Anthropic 则承诺从微软 Azure 购买价值 300 亿美元的云计算服务。

分析师表示:

“所有公司都在试图为新增的 AI 功能寻找最优定价方式,这不仅仅是微软面临的问题。”

被质疑过度依赖 OpenAI

微软的超预期业绩,主要得益于其与 OpenAI 达成的新协议。该协议于去年 10 月签署,是 OpenAI 完成重组、设立营利性实体的一部分。微软目前持有该营利性实体约 27% 的股份,其价值已体现在微软的财报收益中。

微软表示,当季净利润中有 76 亿美元来自 OpenAI 相关收益。即便剔除这部分来自 OpenAI 的提振,微软的盈利表现仍然超过市场预期。

微软正加快步伐,将包括由 OpenAI 提供支持的 AI 工具嵌入其产品中,押注聊天机器人和自动化技术将推动公司生产力软件和云服务的销售增长。

微软在周三发布的声明中表示,当季总营收同比增长 17%,达到 813 亿美元;每股收益为 5.16 美元。微软表示,净利润数据受到微软对 OpenAI 投资收益的提振,使每股收益增加了 1.02 美元。

微软预计将在未来几年转化为实际销售的客户承诺金额较去年同期增长了一倍以上,主要原因是一项与 OpenAI 签署的、规模达 2500 亿美元的新协议。

微软表示,其云业务的合同积压金额同比翻倍以上,达到 6250 亿美元。这一规模高于云计算竞争对手甲骨文在 12 月公布的 5230 亿美元。

但其中约 45% 的剩余履约义务仅由 OpenAI 一家公司贡献,凸显出微软对这家初创公司的高度依赖。OpenAI 此前承诺在 AI 领域总投入约 1.4 万亿美元,但尚未披露具体的融资计划。

Gabelli Funds 研究分析师牧野龙太(Ryuta Makino)表示:

“微软股价的市场情绪,在很大程度上已经高度绑定在 OpenAI 的表现上。我认为,从微软的角度来看,至少在当前 ChatGPT 与 Gemini 的竞争格局下,这是一个难以掌控的因素。”

微软正在加速建设用于训练和运行 AI 模型的云计算基础设施。市场需求极其旺盛。微软去年 10 月曾表示,计划在未来两年内将数据中心容量翻倍,并在包括数据中心在内的 AI 基础设施方面投入超过此前预期的资金。即便如此,微软仍表示,要满足不断增长的需求,还需要更多产能。