SanDisk conference call: "Data centers will become the largest market for NAND," CEO says "unable to meet demand" but refuses to blindly expand production

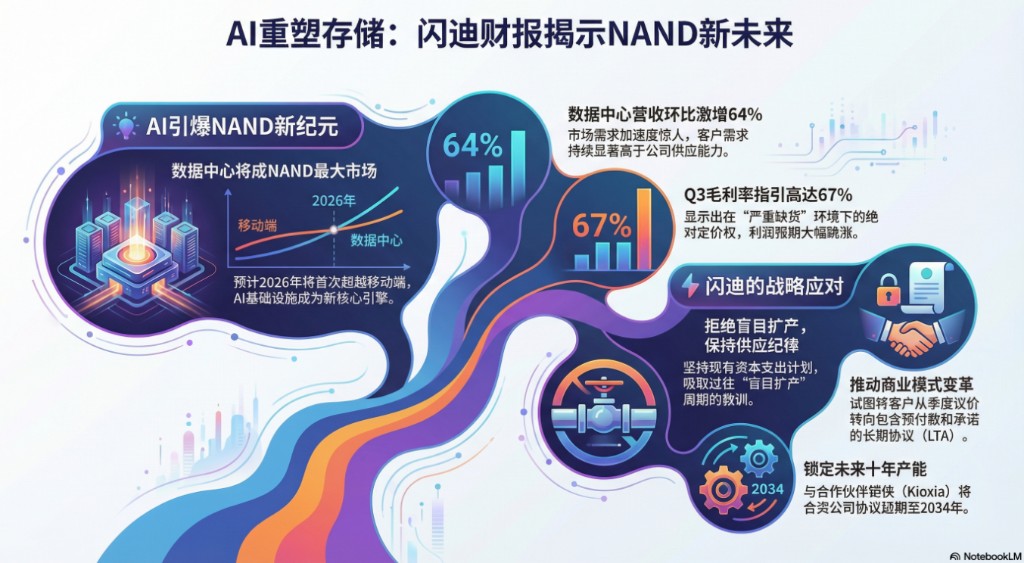

閃迪確立了 AI 對存儲行業的重塑,管理層直言 NAND 正擺脱週期品屬性成為 “AI 基礎設施的關鍵組件”。公司本季度數據中心營收環比激增 64%,預計 2026 年將首超移動端成為 NAND 最大市場。Q3 毛利率指引高達 67%,顯示其在 “嚴重缺貨” 環境下的強勁定價權。不過,閃迪仍然堅持現有資本支出計劃,拒絕盲目擴產。

美股周四盘后,存储巨头闪迪(SanDisk)召开2026财年第二季度财报电话会议。

面对盘后一度飙升15%的股价,公司管理层在电话会中不仅确认了全面超出预期的亮眼业绩,更向市场传递了一个明确信号:AI对存储的需求并非昙花一现,而是一场正在发生的结构性变革。

不仅是热度,更是真金白银:“数据中心2026年将成NAND最大市场”

市场最关心的问题在于:AI的热度是否已经转化为实际的营收?存储究竟是短期行情还是长期结构性变化?

对此,闪迪CEO戴维·戈克勒(David Goeckeler)在会上直言:“这是第一次,数据中心预计将在2026(日历)年首次成为NAND的最大市场。”

这或意味着,过去十几年由智能手机和PC主导存储周期的时代即将结束,AI基础设施建设成为了新的核心引擎。随着AI推理(Inference)场景的爆发,每个部署单元对NAND容量的需求显著提升。

数据显示,公司数据中心营收本季度环比激增64%。更令人震惊的是需求的加速度:

两个季度前,市场预期公司2026年数据中心位元(Exabyte)增长为20%+;

上个季度,这一预期上调至40%+;

本季度,闪迪将2026年数据中心位元需求增长预期直接上调至近70%(High-sixties)。

此外,戈克勒透露,公司的高性能TLC硬盘正在推动收入增长,而代号为“Stargate”的BiCS8 QLC存储级产品也将在未来几个季度开始产生收入。

AI重塑NAND行业:“NAND成为AI基础设施的关键组件”

电话会上,CEO戈克勒更是直接给出了对行业变化的判断。他表示:

“NAND现在被视为满足全球存储需求不可或缺的技术。”“这正在推动供应商与客户之间的商业关系发生根本性的变化。”

他进一步指出,随着AI在数据中心和边缘侧的部署不断扩大,存储的作用已经发生变化:

“人工智能正在推动需求发生阶跃式变化,数据中心和边缘工作负载的扩展,显著提高了系统对存储容量的需求。”

在他看来,这一变化意味着NAND正在摆脱传统的强周期属性:“我们认为,NAND正在成为一个更具韧性、在结构上更具吸引力、长期平均回报更高的行业。”

“NAND正日益成为AI基础设施的关键组件。”CFO路易斯·维索索(Luis Visoso)进一步说道。

在谈及近期存储价格快速上涨时,戈克勒给出了非常明确的判断:

“当前市场发生的一切,是一种完全由需求驱动的现象。”

CFO也表示:“在这个季度,我们无法满足客户的全部需求。”“客户需求持续显著高于我们的供给能力。”

供需博弈:保持资本支出,拒绝盲目扩产

尽管存储短期价格强劲,但CEO强调公司并不会因为短期价格强劲而贸然扩产:

“任何实质性的资本开支增加,都需要我们对多年期、具备吸引力价格水平的需求有高度信心。”

电话会上,管理层多次提到“无法满足客户需求”,目前市场处于严重的“分配环境”(Allocation Environment)。但闪迪当下显得十分克制。

尽管需求火爆,公司仍坚持资本支出计划不变,维持中高个位数的位元增长(Bit Growth),拒绝盲目扩产。这显示出存储巨头们吸取了过往“盲目扩产”周期的教训。

也有分析称,闪迪正利用短缺作为筹码,试图逼迫客户放弃传统的季度议价,转而签署包含预付款和供应承诺的长期协议(LTA)。CEO直言,如果不改变这种商业模式,公司就没有动力增加投资。

但客户显然对此仍有抵触。当被问及LTA的进展时,CFO透露了一个略显尴尬的事实:截至目前,仅签署并完成了一份协议。这表明,尽管买方急需产能,但对于在高位锁定长期价格仍持谨慎态度,双方的拉锯战仍在继续。

战略布局:锁定铠侠十年产能

电话会还宣布了一项重要战略动作:闪迪与合作伙伴铠侠(Kioxia)达成协议,将合资公司(JV)延期至2034年,确立了未来十年的产能底座。

为此,闪迪将在未来几年支付约11.65亿美元的制造服务费。

而这一举动无疑为那些担心长期供应稳定性的客户吃下了一颗定心丸。

指引炸裂:毛利率剑指67%,定价权完全反转

对于未来的业绩指引,公司也信心十足。

如果公司在Q2交出51.1%的毛利率(上季仅29.9%)已经足够惊艳,那么Q3的指引更是让分析师们感到惊讶。CFO路易斯·维索索(Luis Visoso)预计,第三财季非GAAP毛利率将达到65%至67%,EPS指引更是从本季的6.20美元跳涨至12-14美元。

这一超高指引的背后,是存储厂商对定价权的绝对掌控。维索索表示,NAND产能会自动流向利润最高的市场(即数据中心),这导致其他市场即使需求平平,也被迫接受涨价。

传统市场的阴影:PC与手机销量面临下滑

但值得注意的是,在AI的光环之外,传统消费电子市场的基本面并不稳固。

CEO戈克勒承认,进入2026年,PC和智能手机市场将面临单位销量(Units)下滑的基数压力(base effects)。

尽管单机容量的提升(Content growth)可以部分抵消这一影响,但“销量下降”的表述依然揭示了AI之外市场的疲态。

财务“注脚”:一次性收益美化利润,税率将抬头

同时,对于追求精准模型的投资者,本季度的利润成色或许需要打个折扣。

-

一次性收益: 本季度运营费用(OpEx)显著低于预期,主要得益于新产品导入(NPI)会计处理变更带来的约3500万美元一次性收益。CFO提示,这部分不可持续。

-

税率逆风: 随着公司从巨额亏损转向高额盈利,此前累积的税务亏损抵扣已消耗殆尽,预计未来有效税率将从低位回升至14%-15%。

闪迪财报电话会全文翻译如下:

演示环节

接线员:

大家好,欢迎参加闪迪2026财年第二季度财报电话会议。所有与会者将处于只听模式。(接线员说明)今天的演示结束后,将有提问机会。(接线员说明)请注意,本次活动正在录制中。

现在我将会议交给投资者关系主管Ivan Donaldson。请讲。Ivan Donaldson,投资者关系副总裁:

在我们开始之前,请注意,今天的讨论将包含基于管理层当前假设和预期的前瞻性陈述,这些陈述受各种风险和不确定性的影响。这些前瞻性陈述包括对我们的技术和产品组合、业务计划和业绩、市场趋势和机遇以及未来财务结果的预期。

我们不承担更新这些陈述的义务。请参阅我们提交给美国证券交易委员会(SEC)的10-K表格年度报告和其他文件,以此获取有关可能导致实际结果与预期存在重大差异的风险和不确定性的更多信息。今天我们还将引用非公认会计准则(non-GAAP)财务指标。非GAAP财务指标与可比GAAP财务指标之间的调节表已发布在我们网站的投资者关系部分的书面材料中。

接下来,我将把电话交给David。David V Goeckeler,董事长兼首席执行官:

谢谢,Ivan。下午好,感谢大家参加闪迪的第二财季财报电话会议。本季度,营收为30亿美元,环比增长31%,非GAAP每股收益为6.20美元。

人工智能继续推动需求的阶跃式变化,数据中心和边缘工作负载增加了系统的复杂性和存储内容需求。这一转变,加上严格的商业行动和战略性产能分配,加强了我们的业务成果。在讨论我们的终端市场之前,我想先阐述一下NAND行业的演变。NAND现在被公认为世界存储需求中不可或缺的一部分,推动了供应商与客户之间商业关系结构的根本性转变。

供应确定性、更长的规划周期和多年承诺正变得至关重要,以支持超出我们市场传统周期性模式的结构性需求。因此,我们正在与客户进行讨论,从季度谈判向具有更坚定供应和定价承诺的多年协议演变,从而实现更好的规划实践和更具吸引力的回报。这些变化将使我们的规划周期与客户的需求状况更好地保持一致,从而互惠互利。因此,我们的供应计划将继续围绕当前和预测市场价格下的可预测长期需求进行设计。这些动态揭示了我们NAND技术的真正价值,并加强了持续创新和严格执行的必要性。我们的产品得益于在NAND和系统解决方案方面数十年持续的研发和创新投资,并得到了在世界级前端和后端制造方面大量资本投资的支持。因此,我们相信NAND正成为一个更持久、结构上更具吸引力且平均回报率更高的行业。转向我们的终端市场亮点。

本季度,我们继续按照路线图执行,推进整个业务的下一代产品创新和认证,关键客户项目按计划进行。在数据中心方面,我们处于AI基础设施广泛扩张的中心。随着AI工作负载的扩展,企业级SSD需求在整个生态系统中加速增长,特别是推理(inference)推动了每次部署中NAND含量的显著增加。这一势头反映了我们与更广泛的大规模构建和部署AI的客户加深了接触,重塑了我们的数据中心业务,我们预计该业务在近期和长期都将显著增长。

我们要看到所有类型的AI基础设施建设者都在强劲采用我们的产品,包括云超大规模企业(hyperscalers)、边缘和企业数据中心、OEM厂商以及大规模部署AI的系统集成商。我们的技术已成为这些部署的关键推动力,提供了优化AI基础设施所需的性能特征。整个AI生态系统中客户的广泛采用突显了我们技术的实力和产品组合的深度。

在超大规模企业方面,我们已经在第二家超大规模企业完成了PCIe Gen 5高性能TLC驱动器的认证,并有望在未来几个季度在更多超大规模企业完成认证,BiCS8 TLC解决方案也将紧随其后。该产品正在推动我们数据中心产品组合的显著收入增长,该组合环比增长了64%。代号为“Stargate”的BiCS8 QLC存储级产品继续在两家主要超大规模企业进行认证,预计将在未来几个季度开始产生收入,为数据中心增长提供额外的推动力。在边缘计算方面,随着PC和移动设备的更换周期和AI采用推动了更丰富的配置和更高的单设备存储含量,需求显著超过了供应。

在这种分配环境下,我们正与关键边缘客户合作,优先考虑他们的关键任务需求,并在我们可用的供应范围内优化产品组合,确我们整个产品组合的最佳长期回报。在消费类产品方面,产品组合向高端产品和更高价值的配置转移,支持了存储容量、增长和盈利能力。我们推出了在USB外形尺寸上的突破性产品——Sandisk Extreme Fit,这是我们最小的大容量USB-C闪存盘。这一突破性的“即插即忘”(stay-put)产品为我们的客户提供了一种无缝且经济实惠的方式,以显著扩展其PC和智能手机的存储空间。

我们扩大了与全球知名品牌Crayola和FIFA的关键许可计划,全面落实了去年2月首次推出的多彩Sandisk Crayola USB-C闪存盘和官方授权的2026年FIFA世界杯产品所强调的承诺。这种强劲的势头在假期期间持续,受到针对性游戏主导计划的推动,包括我们的“不要删除你的游戏”活动。在2026年CES上,我们推出了Sandisk OptiNAND系列,重新命名了WD Black和WD Blue NVMe SSD,以强化品牌架构并巩固性能领先地位。这些行动共同反映了我们继续专注于通过品牌、创新和严格的市场进入执行来推动需求,巩固闪迪在游戏、创作者和日常消费者细分市场的领导地位。

我们在终端市场取得的这些胜利反映了我们运营的敏捷性和广泛产品组合的韧性。展望未来,我们继续看到2026日历年之后的客户需求远高于供应,这需要与客户保持一致的仔细分配计划。我们仍然专注于通过BiCS8过渡进行严格执行,支持中高个位数的平均长期位元增长(bit growth),同时维持我们的资本支出计划。我们正在努力支持客户需求,同时确保盈利能力能够支持提供世界上一些最先进半导体技术所需的巨额研发和资本投资。

接下来,我将把电话交给Luis,深入探讨我们的财务业绩和指引。Luis Visoso,执行副总裁兼首席财务官:

谢谢,David。在深入探讨财务数据之前,我将提供一个简短的市场概况。我们认为NAND市场正在经历由AI催化的结构性演变。这种演变在数据中心更为明显,随着数据温度的升高,数据增长正在加速,Token强度正在加速,存储是推理的关键推动力。因此,NAND正日益成为AI基础设施的关键组件。数据中心对NAND的更高需求影响了其他市场,随着NAND流向最具吸引力的市场,这些市场也在增长。我们认为这种结构性演变是可持续的,应该会减少我们NAND业务的周期性,创造更高的平均长期利润率和回报。在12月份的季度,我们经历了终端市场状况的明显且显著的改善,这导致了更高的定价。

本季度,由于对我们产品的需求持续超过供应,我们做出了战略性的分配决定。我们用于分配位元(bids)的框架是最大化价值创造。我们优先向我们的战略客户供应,即那些认可我们可以共同创造价值的客户。这些是我们打算与之建立有价值的合作伙伴关系的客户,从而建立可持续的多年商业实践,具有高度可预测的需求、回报和资本部署。

鉴于市场的强劲,本季度我们无法满足客户的需求。我们正在改进定义战略参与的方式,优先考虑那些拥有多年供应框架和共同规划承诺的客户,而不是交易性的短期需求信号。我们继续保持谨慎,不改变我们的资本支出计划,该计划支持通过BiCS8过渡实现中高个位数的位元增长。我们的投资姿态仍然专注于服务有吸引力的持续需求和健康的盈利水平。任何实质性的资本部署增加都需要确信在有财务承诺的数年范围内,具有吸引力价格水平的需求是持久的。在当前环境下,我们致力于供应我们的三个终端市场,因为我们相信多样化可以最大化价值创造。我们计划继续在这些市场中与多样化的客户组合建立战略关系,使我们能够更深入地了解他们的长期需求。本季度,我们继续与客户在建立共同承诺方面取得进展,这提高了业务的可预测性。

客户承诺和商定的商业条款是提供供应确定性和投资资本回报可预测性的最有效机制,使我们能够更审慎地管理各地区的资本密集型业务。在这个背景下,我将更深入地介绍季度业绩。第二季度营收为30.25亿美元,环比增长31%,同比增长61%。这一数据优于我们25.5亿美元至26.5亿美元的指引。

营收超预期来自于各细分市场价格的上涨,且在季度内走强。位元出货量同比增长22%,环比增长低个位数。在第二季度,我们看到了所有终端市场的强劲环比需求。边缘计算营收为16.78亿美元,环比增长21%。

消费类营收为9.07亿美元,环比增长39%。数据中心营收为4.4亿美元,环比增长64%。我们第二季度的非GAAP毛利率为51.1%,高于上一季度的29.9%。这一数据优于我们41%至43%的指引。

毛利率超预期来自于更高的定价。单位成本降低如期而至,加强了利润率的改善。在第二季度,我们产生了2400万美元的启动成本。不计此成本,非GAAP毛利率本应为51.9%。

第二季度的非GAAP运营费用为4.13亿美元,占营收的13.7%。这一数据优于我们4.5亿美元至4.75亿美元的指引范围,反映了改变新产品引入管理方式带来的一次性收益。因此,非GAAP营业利润率为37.5%,高于上一季度的10.6%。第二季度的非GAAP每股收益(EPS)为6.20美元,高于上一季度的1.22美元。

这一数据优于我们3美元至3.40美元的指引范围。非GAAP每股收益的超预期反映了高于预期的营收和更低的成本。主要的GAAP与非GAAP调节项目包括税后5200万美元的股票薪酬(占营收的1.7%),以及与某些法律事务相关的9300万美元。转向资产负债表。

我们在本季度结束时持有15.39亿美元的现金及现金等价物,债务为6.03亿美元。本季度,我们额外偿还了7.5亿美元的债务,并在季度末拥有9.36亿美元的净现金头寸。转向自由现金流,本季度我们产生了8.43亿美元的调整后自由现金流,代表27.9%的自由现金流利润率。这包括来自运营的10.19亿美元,部分被1.76亿美元的净现金资本支出所抵消。

我们的总资本支出总计2.55亿美元,占营收的8.4%。今天早些时候,我们宣布已与铠侠(Kioxia)达成协议,将四日市(Yokkaichi)合资企业延长至2034年12月31日。通过这次延期,四日市和北上(Kitakami)合资企业将拥有相同的到期日。基于超过25年的合作伙伴关系,我们相信合资企业反映了我们的运营规模和随着时间推移创造的巨大共同价值。

该合资企业使两家公司能够设计和制造性能最高、成本最低的NAND技术,为世界基础设施提供动力。作为此次延期的一部分,闪迪同意为铠侠将提供的制造服务(确保持续的产品供应)支付总计11.65亿美元。这笔金额将在2026日历年和2029日历年之间支付。该成本将在未来九年内计入我们的销售成本。

转向指引。对于第三季度,我们预计营收在44亿美元至48亿美元之间。我们预计市场将比第二季度更加供不应求。我们预计由于我们将受益于数据中心的加速走强,导致季节性低于历史水平,位元出货量将出现中个位数的下降。

我们对第三季度非GAAP毛利率的预测是在65%至67%之间。对于第三季度,我们预计非GAAP运营费用在4.5亿美元至4.7亿美元之间。我们预计非GAAP利息和其他费用在2500万美元至3000万美元之间,非GAAP税务费用在3.25亿美元至3.75亿美元之间。假设完全稀释股数为1.57亿股,我们预测第三季度的非GAAP每股收益在12美元至14美元之间。

接下来,我把电话交还给David。David V Goeckeler,董事长兼首席执行官:

谢谢,Luis。总之,我们将继续成功地驾驭我们业务深远演变的早期阶段。除了在我们在PC、智能手机、平板电脑、云、汽车、游戏设备、机器人等日常使用的技术中发挥核心作用外,NAND还是支持人工智能发展和扩散的关键技术。

在世界上一些最大和资本最雄厚的科技公司的推动下,预计数据中心将在2026年首次成为NAND的最大市场。受我们要技术所提供的性能推动,我们所有终端市场的客户正越来越多地寻求基于共同承诺和商定的、与我们要现有供应计划一致的财务上有吸引力的条款的商业实践。我们的供应计划将继续与这种有吸引力、真实且可持续的长期需求保持一致。在这种背景下,利润率预计将在结构性更高的水平上重置,为所需的实质性创新和投资提供公平的回报。

我们的技术和产品组合在完美的时刻与这些不断变化的市场动态相交汇,使我们能够管理平衡的投资组合并交付行业领先的财务业绩。现在,让我们开始提问。问答环节

接线员:

提问与回答接线员:

谢谢。我们现在开始问答环节。(接线员说明)第一个问题来自Bernstein的Mark Newman。请讲。Mark Newman:

嗨,非常感谢,祝贺今天取得了极好的数字。真的,真的非常棒的数字,特别是第三季度的指引。

所以,很明显正在发生的是价格正在以空前的速度扩张。我想我的问题是针对Dave开场的评论。你们是如何考虑长期协议(LTA)的?当然,长期协议有利有弊,因为长期协议锁定了价格,而在价格上涨如此之快的时候,我想你们实际上并不想要那么多长期协议。但是我想了解一下你们是如何考虑这一点的,我们应该如何看待这一点,就你们达成长期协议的比例而言,以及这对未来的影响。

那太好了。如果您能简要谈谈长期的供需平衡,如果在这个非常、非常巨大的,目前看起来相当严重的供应不足的情况下,是否有增加供应的计划,或者你们是如何考虑这一点的,那也太好了。非常感谢。David V Goeckeler,董事长兼首席执行官:

谢谢,Mark。

感谢你的评论。关于业务动态发生的一系列事情促成了你们看到的结果,我说几句。首先,这源于产品组合和创新。你知道,我们的BiCS8节点,我们已经开始量产并继续量产,这只是一个极好的节点。

性能,QLC性能,2Tb的裸片(die),很多东西让我们处于非常有利的位置。顺便说一句,我要指出我们延长了合资企业(JV),我们对此非常高兴,这将再持续十年。这正在支持非常强大的企业级SSD产品组合。

这是我们推动了一段时间的事情。上个季度我说过,我们将看到整个财年的增长。我们在第一财季看到了,我想是29%的环比增长。现在我们在第二财季看到了64%的环比增长,我想你们会看到下半财年从这里开始加速。

所以,主要业务创新的第三个支柱坦率地说是发生在消费类业务中。很多新产品推出。我们今年宣布的这款Extreme Fit产品确实是一个突破性的产品。它允许我们的客户非常无缝和经济地增加设备的存储容量。

这在USB领域算是一种创新。你可能认为这种事不会再发生了,但这并不是一个可移除的产品。它设计成插上就一直留在那。你可以看到我们要像FIFA那样的合作伙伴达成的协议,这可能是今年最大的事件。我们在那里有很棒的联名产品。我们看看我们的消费类业务,我们看到了50%的同比增长,所以那里的表现真的很强劲。这种产品组合创新的卓越性使我们能够拥有更好的投资组合组合,如果我们回顾过去几个季度,我们实际上能够将利润最低的业务换成现在利润最高的业务,这也为业务提供了显著的顺风。除此之外,还有供需动态,这正在推动整个市场向前发展。

所以真的是所有这些因素的结合推动了业务向前发展。这不仅仅是价格问题,尽管显然处于强劲的定价环境中很棒。谈到长期协议(LTA),我会谈一点,我知道Luis也会有一些很好的评论。所以,当我们达到我们认为我们的技术获得了更公平的回报,且坦率地说,客户正在寻求更多的供应保证时。

我的意思是,我想指出当前市场的一点,这完全是一个需求驱动的现象,关于市场上正在发生的事情。我们在一年多的时间里对我们的供应计划非常透明。我们在这个市场上投入了大量资金。我们要投入数亿美元的研发资金来推动路线图。

我们投入数十亿美元的资本支出,我们已经非常明确我们将持续推动中位到高位数的位元增长,我们认为这是一个很好的市场。现在发生的情况是,我们只是没有获得足够的可见性来了解需求端到底是什么。我的意思是,如果我们看数据中心,我们现在已经经历了三个预测周期。上个季度,我们从该市场的中段20%增长调到了中段40%增长。现在我们看到的是2026年该市场的高段60%的艾字节(Exabyte)增长。我想我们的客户意识到了这一点,特别是在数据中心市场。他们的数字很大,他们在26、27、28年需要什么,我们甚至在和其中一些人谈论29和30年。他们在做自己的规划。他们将需要的艾字节数量是巨大的。因此,长期协议是关于提出一个模型,使我们有信心在持续的基础上供应那种水平的需求。对我们来说,这不是关于下个季度或下下个季度的需求是什么。考虑到我们业务的动态,我们对此无能为力。但我们希望将长期增长率与长期持续需求相一致,正如你所说,以有吸引力的财务状况。让我把这个问题交给Luis。Luis,对此有什么看法?分析师(Luis Visoso):

是的,我的意思是,David涵盖了大部分内容。我想说的是,Mark,我们看到跨终端市场和跨地区的客户都在联系我们。所以这不仅仅是少数几个。我们确实看到了广泛的基础,这对我们来说非常有趣。我们正在取得重大进展。我们与几位非常、真的希望我们优先考虑或保证供应的客户取得了重大进展,正如David所指出的,他们将其视为业务的关键推动力,这正是他们所寻找的。

现在,就你的一点,我们在如何定义几个指标方面非常深思熟虑。一个是协议的长度,我们将交易的价格,数量,我们投入其中的业务量,以及其中的任何预付款部分。所以我们非常深思熟虑,这应该是价值增值的,而不是相反。分析师(Mark Newman):

太好了,非常感谢,能不能快速评论一下你们如何看待长期的供需以及增加供应的任何灵活性?David V Goeckeler,董事长兼首席执行官:

不,我的意思是,Mark,我们有我们的供应计划。

再一次,我们已经非常明确了我们的资本支出计划是什么,我们的位元增长计划是什么,就是这样。关键是在那个供应水平上满足我们的客户,并了解我们如何分配,然后,正如我们所说,是关于我们所有人都抬起头来看看地平线更远的地方,这个市场的需求到底会是什么,持续的需求会是什么,我们真的需要摆脱这只是一个交易市场的想法,在这个市场我们只能一次获得一个季度的强劲信号。我的意思是,公平地说,我们确实每年都会从客户那里获得需求信号,但我们实际上只交易那个。我们每个季度都在谈判价格,这使得增加任何形式的支出都非常、非常困难,因为我们只是对经济性没有可见性,而且,再一次,特别是随着市场向数据中心转型,我认为数据中心客户更愿意。

正如Luis所说,这是跨越所有客户的,但我认为数据中心客户,鉴于他们的需求概况以及他们坦率地说增长有多大,在参与这种对话方面更加积极主动,真的想了解几年后的供应保证,以及我们如何提出一个——我们可以围绕它制定什么样的商业实践?而且,那是一个,正如我在准备好的发言中所说,我说我们处于这个转型的早期,那就是早期的部分。我认为商业实践将会改变,我认为这一切都是为了更好。我们在接下来的几个季度里必须完成这些对话。非常感谢Himanshu。Mark Newman:

非常感谢。

再次祝贺,伙计们。David V Goeckeler,董事长兼首席执行官:

谢谢,Mark。我们很感激。接线员:

下一个问题来自摩根士丹利的Joe Moore。请讲。Joseph Moore:

太好了。谢谢。在消费电子展(CES)上,Jensen(黄仁勋)谈到了这个键值缓存(Key-Value Cache),并给出了一些关于每GPU太字节数的数字,看起来像是一个相当大的市场。

你们有收到相关的迹象吗?你认为那里——我们应该把这当作直接的数学计算吗?每个人都有不同的实现方式吗?以及这对数据中心和NAND会产生什么影响?David V Goeckeler,董事长兼首席执行官:

是的,Joe。我们现在正在研究这个问题。我们正在与NVIDIA合作研究这个问题,以及他们是如何考虑的。

当然,然后我们会与我们的客户一起研究他们将在部署中如何配置它。所以还有点早。关于这点我会说几件事。首先,这些需求目前都没有包含在我们讨论的需求数字中。

我认为这只是一个完美的例子,说明我们在未来需求将是什么方面都需要更多的合作。其次,我们对此的初步看法,当我们看,比如说,27年的需求时,我们认为那大约是额外的75到100艾字节(exabytes)。然后在那之后的一年,你可以把那个数字翻倍。所以这是一个巨大的需求量。

我认为这,再一次,只是NAND在AI架构中处于中心地位的另一个例子。在这一点上非常、非常清楚。如果以前不是,AI架构正在改变,对吧?这并不奇怪。任何如此深刻且正在如此大规模部署的技术,我们都将继续看到架构的创新和演变。

所以我们将非常密切地关注这一点。NAND将成为该架构的重要组成部分。它是最具扩展性的半导体存储技术,或者可能是最具扩展性的半导体技术。所以我们在看那些配置。

这是非常真实的需求。我们只是试图弄清楚它。然后我们可能会在今年下半年将其纳入数字中,进入27和28年。Joseph Moore:

太好了。

谢谢。太好了。谢谢。作为一个后续问题,企业级SSD的机会,目前在TLC和QLC之间是如何细分的,未来又是如何变化的?David V Goeckeler,董事长兼首席执行官:

我认为我们目前大致跟踪市场。

主要是TLC。我会说它偏向于TLC,特别是对我们而言。然后,我们还没有推出基于存储的QLC的Stargate产品。它正在认证中。所以我们将在接下来的几个季度开始为该产品发货以获取收入,这让我们很兴奋,为我们的数据中心产品组合提供了另一个增长顺风。那将提升QLC的混合比例。但在目前,我认为整个市场和我们的产品组合,是偏向于TLC的。分析师:

太好了。

谢谢。很棒的数字。David V Goeckeler,董事长兼首席执行官:

谢谢,Joe。很感激。

下一个问题来自Cantor Fitzgerald的CJ Muse。请讲。C J Muse:

是的。下午好。

谢谢接受提问。我想第一个问题,有没有办法量化与AI基础设施建设相关的NAND增量需求?我不包括KvCache,但是,我们之前是中高个位数,我很好奇现在,基于你们与客户的对话以及你们看到的趋势,看26、27、28年,新的需求年复合增长率(CAGR)大概是多少?David V Goeckeler,董事长兼首席执行官:

我认为我们目前对此最好的代理指标,CJ,就是我们在数据中心看到的艾字节需求。正如我之前所说,我的意思是,两个周期前我们在看,比如26年数据中心的艾字节增长是20%的中段。

上个季度我们在谈论,考虑到发生的资本支出周期,我们将其提高到了40%的中段。我们现在的预测是数据中心有高段60%的艾字节增长,这还不包括在这个财报周期内的任何资本支出提升。所以,仅仅是季度环比的需求就有显著增加,我们认为这几乎都是由AI驱动的,显而易见。C J Muse:

完美。

谢谢。然后我想你们在本季度偿还了相当数量的债务。你们只有6亿美元未偿还,可能本季度就能还清。所以好奇的是,当你们完全处于现金状态时,我们应该如何考虑资本回报,特别是关于未来几个季度的股票回购?Luis Visoso,执行副总裁兼首席财务官:

是的,我们感到,我们对在减少债务方面取得的进展感到非常自豪。

记得我们是从20亿美元开始的,它下降得非常、非常快,本季度减少了6亿美元,我们将继续将其降低。CJ,我们的首要任务是继续像我们一直做的那样投资于业务,并建立审慎的现金资源,这是一个手头有现金会有所帮助的业务。我们不会浪费你们的现金,别担心,但我们要建立审慎的现金资源,我们将继续减少我们的债务,在适当的时候,我们将继续扩展并给你更新。但到目前为止,这些是我们的优先事项。C J Muse:

谢谢。David V Goeckeler,董事长兼首席执行官:

谢谢,CJ接线员:

下一个问题来自高盛的Jim Schneider。请讲。James Schneider:

晚上好。

谢谢接受我的提问。首先,在供应方面,我想知道你们能否简要介绍一下四日市和北上的工厂网络概况,以及目前的状况,我假设利用率基本上是满负荷的,但是,当你们更战术性地思考今年之后的高双位数大增长前景时,你们预计如何在未来,比如说,18个月左右提升你们整体的合资工厂网络,然后也许给我们任何一种看法——你们对目前鉴于你们的一些竞争对手最近宣布的一些行业绿地产能扩张的看法?David V Goeckeler,董事长兼首席执行官:

所以,首先,我们有——正如你所说,我们有两个主要基地,四日市和北上。我认为本季度迈出的一大步是我们宣布延长围绕四日市的合资协议,使其与北上的协议一致,所以它们现在都运行到2034年,这给了我们未来九年非常好的供应保证,我们将继续讨论那之后会发生什么,但这与铠侠的关系已经持续了几十年,这简直令人难以置信,并且将持续很长一段时间。所以,我们觉得我们在那里处于非常好的位置。

听着,我们在工厂里已经有几个季度没有利用率不足的情况了。我们在几个季度前就克服了那一点。可能还有一点点成本流转的记忆。我想那些都是上个季度的事了。

我们结束了。所以,它们正在满负荷运转。北上是我们正在扩张的地方。我们刚刚开设了K2 FAB,所以我们在那里有额外的空间。我认为我们只是,由铠侠领导的合资企业在这部分刚刚做了非常好的产能规划,并且对于我们如何在未来许多年内根据需要扩展到北上基地有很好的计划。所以,我们对在那里的定位感觉真的很好。至于行业的其他部分,它是——正如你所知,它的交付周期很长。我们最近看到了一些公告。

我会认为那些是正常的进程。我们都在不断建设洁净室空间。正如我之前所说,这是一个我们在供应方面非常一致的市场。我们将以中高个位数的比率增长位元。

我们将通过创新来做到这一点。我们将通过——这种创新将需要额外的洁净室空间。这都在计划之中。我预计会看到持续的支出来达到那个数字,但我们没有看到任何不寻常的事情。

而且我认为正如我们要知道的那样,如果你想开始建造一个新的FAB,你需要数年时间才能建成并投入运营并从中产出产品。所以这就是我们如何看待市场的一点点。最后评论,当我们谈论供需时,所有这些都已计入我们的数字中。James Schneider:

谢谢。

然后也许作为一个后续,能不能也许谈谈,很明显你提到了在这个日历年结束时与另一个企业级SSD超大规模客户的认证,例如,你预计你们的企业级SSD敞口占总收入的百分比会有多大?谢谢。David V Goeckeler,董事长兼首席执行官:

是的,我们现在还不会给出一个确切的数字,但我只想说敬请期待。我想我们说过这个,我们的业务将在这个市场上继续增长。我们已经看到了29%的环比增长,随后是64%的环比增长,不涉及太多细节。我想下个季度你们也会看到一个显著的提升。所以我们对产品组合的位置感觉真的很好。就像我说的,客户的反响,不仅仅是超大规模企业,而是整个正在建设AI基础设施的生态系统。我们在市场上的计算聚焦型TLC产品确实在推动这种增长。我们将在接下来的几个季度看到我们的BiCS8 QLC产品开始发货以获取收入,这将是增长的另一个顺风。正如我们讨论的那样,BiCS8 QLC的性能受到了极好的欢迎。所以我们继续看到对这些产品的非常高的兴趣,并正在进行认证。我们期待持续增长,这将是我们一直谈论的平衡产品组合的一部分,关于我们将如何将我们的供应分配到市场的那个部分。但我们对我们所处的位置和我们要去的地方感到兴奋。James Schneider:

谢谢。David V Goeckeler,董事长兼首席执行官:

谢谢,Jim。接线员:

下一个问题来自SIG的Mehdi Hosseini。请讲。Mehdi Hosseini:

是的,谢谢接受我的提问。我有两个后续问题,这是给团队的。当我看你们对3月Q3财季的指引时,假设低个位数的位元增长,ASP和混合价格有很大的跳跃。我想问的是,我们应该如何考虑影响ASP的混合因素?很明显,随着你们扩展SSD,会有更高的溢价。

比起位元,你们捕捉到了更多的溢价或经济价值。有没有什么方法可以帮助我理解?因为仅仅考虑ASP的绝对值可能会给我们错误的印象。所以任何你能提供的帮助都太好了。我没有后续问题。Luis Visoso,执行副总裁兼首席财务官:

是的,所以我们拥有的混合影响与我们要端市场的变化关系不大,更多的是与客户有关,对吧?以及我们如何服务市场。我在准备好的发言中谈了一点这个问题。你看到的是我们正在推动更好的混合。我们正在与那些重视我们关系、重视我们产品的客户合作。

因此,我们从中获得了更好的毛利率。所以这其中有一个混合的成分,就你的一点而言。Mehdi和Wilco,还有一些定价因素。现在,我们相信市场会。

继续,抱歉。Mehdi Hosseini:

哦,我只是想说,只是一个快速的后续。你们能不能提供任何混合的细分,这样我们就不会太过于关注ASP的趋势?David V Goeckeler,董事长兼首席执行官:

是的,我们会在下个季度报告时提供给你。Mehdi,关于指引,目前我没有任何东西可以分享给你。Mehdi Hosseini:

好的,太好了。还有一个给David的问题。看,我们要在这里,短缺在增加。它在加剧。

你和你的同行正在参与多年合同的讨论。正如你强调的,这些项目需要数年时间。建造晶圆厂和放置设备是一个非常漫长的过程。为什么没有更多的紧迫感?为什么你的客户不愿意承诺更多?他们在整个AI供应链中承诺投资。

但是当涉及到内存或NAND时,我没有感觉到紧迫感。如果这要等到今年下半年,那就意味着短缺将加剧,除非SSD 60%的艾字节增长可能只是一个短名单。但我怎么能调和这两者呢?David V Goeckeler,董事长兼首席执行官:

对此我有很多想法,Mehdi。我的意思是,首先——我会争辩说实际上有相当多的紧迫感,事情正在相当戏剧性地、相当迅速地变化。

对吧?我的意思是,你谈论的是一个按其运作方式运作了可以说几十年的市场。那个市场的运作方式是基本上每个季度都有一次NAND拍卖,这就设定了价格。所以,这就设定了价格。然后我们都要讨论每个季度的价格是多少。

然后在供应方面,我们试图搞对我们供应多少,但经常搞错。当你搞错的时候,经济状况就完全崩溃了。所以,我们正试图从那个世界中走出来。我们为什么要从那个世界中走出来有很多原因。有很多技术原因和我们过去谈过的各种东西,我们可以谈很多。但是,对于一件你已经做这种行为十年的事情,仅仅在一个季度内醒来并决定彻底改变一个行业的商业实践,几乎是真的很、很难做到的。所以,但我确实认为这正在发生。我确实认为客户开始看,就像我说的,他们开始看得更远,特别是在数据中心。

我认为这一点不容低估,即现在数据中心是NAND最大的市场这一想法。我的意思是,这是一个曾经由——或者不是由其主导,但是当主要客户是智能手机、PC时,我将其视为传统上的商品NAND市场。我讨厌那个词,但那是人们对此的看法。数据中心不是那个市场。就像数据中心不是商品NAND市场一样。

数据中心是——NAND是一个高度战略性的产品,是非常复杂的AI架构的一部分。我需要极高的性能,我需要创新,我需要适合我的配置的特定企业级SSD。这与“我只需要同样的产品,我可以插入来自五个不同供应商的任何一个”的想法大相径庭。那不是——所以那个市场现在成为主要市场,特别是主要的增长引擎,真的,我认为,正在开始挑战市场传统运作方式的商业实践。

再一次,实际上我对这发生得相当快感到相当乐观。现在我们看看有多快。我的意思是,我们要际上到了宣布合同的地步了吗?我们还没有完全到那里。我们有一些正在进行中。

但在我看来,相对而言,进展相当快。对于这么大的市场,这么多参与者,每个季度交易这么多业务,看到它像现在这样变化得这么快,实际上是相当了不起的。Mehdi Hosseini:

谢谢你的详细说明。David V Goeckeler,董事长兼首席执行官:

没问题。谢谢,Mehdi。接线员:

(接线员说明)下一个问题来自美国银行的Wamsi Mohan。请讲。分析师:

嗨。我是Ruplu代替Wamsi。我可以问Luis一个问题吗?本季度,运营费用(OpEx)降低了。你说你在管理新产品导入(NPI)方面获得了收益。能不能详细说明一下,那个收益是什么?能不能谈谈资本分配计划?你预计在HPF和数据中心扩张上花费多少,以及任何资本回报计划或并购计划?谢谢。Luis Visoso,执行副总裁兼首席财务官:

是的。所以,让我试着解开OpEx的问题,因为我以为有人会问。我们对销售产品的方式做了一个经常性的改变。基本上,我们现在开始对我们的认证单元收费。过去,我们习惯在成本发生时记录成本,对吧?它们是期间成本。这是一个非经常性因素,这是一个收益,一次性收益,因为我们从期间成本转入库存,因为我们现在正在销售这些认证单元。这有意义吗?分析师:

是的。这很清楚。

好的。所以,我们将获得持续的节省,因为我们对客户收取这些认证单元的费用,并且随着我们进行过渡并通过库存,会有一次性收益。关于资本分配问题,正如我之前所说,我们的资本分配策略没有改变。我们将继续投资于业务。

我们将建立审慎的现金储备,这对这个业务非常有帮助,特别是考虑到我们要处的位置。我们认为我们需要继续建立现金储备,我们将继续减少债务。所以我们已经从20亿美元减少到了6.5亿美元,所以我们正在取得巨大进展,我们将继续在那方面取得进展。我们在为业务提供全额资金。

我们正在从BiCS8过渡中为业务提供资金。我们正在为我们的OpEx提供资金,我们觉得我们正在适当地为业务本身提供资金。Mehdi Hosseini:

指引中有任何未充分利用的费用吗?Luis Visoso,执行副总裁兼首席财务官:

不,指引中没有,实际数据中也没有。Mehdi Hosseini:

好的,非常感谢。接线员:

下一个问题来自瑞穗的Vijay Rakesh。请讲。Joseph Moore:

嗨,Dave和Luis。很棒的季度,非常惊人的数字。只是想知道关于2026-27年,你们在看什么样的位元增长?很明显ASP定价一直在飙升,但只是想知道不同细分市场的价格趋势如何,从数据中心到零售到消费类SSD,如果你能给我们一些颜色,谢谢。David V Goeckeler,董事长兼首席执行官:

是的,所以我们在27、28年看到的位元增长,与我们在2月初谈到的一致。我们仍然在谈论每年中高个位数的位元增长。除非我们看到这种需求是存在的、可持续的和有利可图的,否则我们不会改变我们的假设。

所以我们的计划仍然是——我们的记录计划是那种高个位数的年度位元增长。关于我们要称为终端市场的定价,这非常有趣,对吧?你看到的是价格并没有完全相同地变动,但基本上是以相同的速度变动。现在我们看到发生的情况是NAND最终可以流向任何市场。所以NAND会自然流向最有吸引力的市场。

所以当数据中心价格上涨时,它们确实会对其他市场产生影响,举个例子,对吧?所以这就是我们在各个市场看到的。价格基本上全线上涨。接线员:

下一个问题来自法国巴黎银行的Karl Ackerman。请讲。Karl Ackerman:

嗨,谢谢接受我的提问。我想祝贺你们取得非常好的季度。产品路线图是什么?我想有——现在你们的数据中心占比已经达到15%,NAND闪存现在越来越多地被附加到AI计算上。所以我认为这正在对性能创造新的要求,所以你们在,能不能跟我们更新一下你们的产品路线图来满足这些新要求?比如,我想有高IOPS的SSD,你们在HPF上有接触,所以那些新产品看起来怎么样?David V Goeckeler,董事长兼首席执行官:

是的,所以我认为这是正在进行的、由数据中心驱动的大量创新的一个很好的例子,就像我之前提到的那样。

所以,你是对的,我们要称为计算聚焦的、TLC高性能驱动器正是目前推动产品组合的因素。正如我所说,我们刚刚看到了64%的环比增长,所以我们继续看到对那些高性能产品的非常强劲的拉动。正如我所说,当我们开始将这些迁移到BiCS8时,我们觉得我们处于非常有利的位置,但是正如你所说,还有一大堆新的创新正在进行,我认为,我认为创新引擎在整个行业中依然活跃且良好,这也就是,我们将如何满足AI存储的需求?模型变得更大,生成的Token更多,缓存变得更大,这自然是一件你开始考虑NAND及其巨大扩展特性的事情,你是对的,那里有很多创新。有高IOPS企业级SSD,这当然是你可以想象我们正在做的事情。你知道,两年前我们对此有自己的想法,我们在投资者日谈到了它,我们相信,有机会重新架构NAND以将其引入AI。我们将其注册为高带宽闪存(High Bandwidth Flash,HBF)。我认为在过去的一年里,这已成为一条更受认可的前进道路,现在有很多人在做这个,顺便说一句,我们继续在做这个。我们对进展非常、非常高兴。我们就用例与客户进行了深入的对话。

我们正在设计NAND裸片。我们正在构建控制器,所以那继续向前推进。显然,随着我们前进和计划的确定,我们会对此有更多要说的,但是,我认为所有这些只是一个例子,即随着AI架构继续扩展,存在巨大的创新机会,这是非常令人兴奋的,我们仅仅处于推动这项技术并在全球范围内扩展它的非常早期的阶段,而且我们拥有,也许整个技术行业,处于非常有利的位置来做到这一点。它们是历史上一些最大、最有能力的科技公司。

显然,它们正在投入大量——大量资源来推动这项技术并以非常快的速度在全球范围内扩展它,我认为这是令人难以置信的兴奋。我认为这将会继续下去。我认为我们在这方面还超级早,我认为这将会持续很长一段时间。接线员:

下一个问题来自富国银行的Aaron Rakers。请讲。Michael Stadnoff:

嗨,伙计们。谢谢。我是代表Aaron的Michael Stadnoff。

我想回到LTA(长期协议)的讨论。你们最终确定了这些协议中的任何一个了吗?如果是这样,部分或全部预付款是否属于,我想,任何已最终确定的协议的一部分?这是我们应该期待向前发展的事情吗?我知道你有点暗示了。Luis Visoso,执行副总裁兼首席财务官:

是的。到目前为止,我们已经签署并完成了一项协议。

我们不披露条款。其中有一个预付款部分,我们认为在这类协议中很重要,但这就是我要说的,Michael。所以我们有一个已完成,还有几个在排队。接线员:

下一个问题来自花旗集团的Asiya Merchant。请讲。Asiya Merchant:

太好了。谢谢接受我的提问,这里的结果很棒。David,上个季度,我想你分享了一些关于你如何看待边缘市场、PC、智能手机,也许还有消费市场的想法。

仅仅考虑到内存处于分配状态这一事实,人们在谈论PC和智能手机销量下降,只是你是如何考虑这一点的,以及你的OEM客户向你提供了什么关于这些市场的信号,以及这对你大概在26年下半年和进入27年的需求前景有何改变。如果我可以给Luis插一个问题。在结构上,NAND正在经历这种动态,这显然是一个高度战略性的产品。你们是如何考虑你们的真实周期毛利率的?看起来你们达到那个水平已经是相当长一段时间以前的事了,但你们在这里是如何从结构上考虑毛利率的?谢谢。David V Goeckeler,董事长兼首席执行官:

好的。谢谢,Asiya。所以看,关于这个有几个想法。所以首先,在消费市场方面,我认为我们对消费类产品组合的位置非常满意。

正如我所说,我们刚刚实现了超过50%的同比增长。我认为我们在那里所做的关于我们如何考虑品牌、创新、产品组合的工作,那对我们来说是一个长期市场。它将继续是我们的一个长期市场。我们认为我们能够通过Sandisk品牌的价值在那里驱动价值。

所以我们认为那是一个伟大的业务,并将继续如此,我们将继续投资于它。在其他一些市场,比如,看,我认为这就是原因之一。显然,我们在准备时看数字,如果你只看26年,我们的PC销量是2.85亿台。我不认为我们会——任何人在年初会选那个数字。

所以它只是——在这些市场的单位增长、内容增长方面继续非常强劲的结果。所以看,当我们进入26年,或者我们现在在26年,我们将看到那方面的一些基数效应,单位的一些下降。我认为我们仍然从那些市场的客户那里得到非常强劲的信号,想要供应。我的意思是,在持续的基础上非常强劲的信号。

我们正在尽可能紧密地与他们合作。我认为在这个市场时期,与我们的客户保持密切联系极其重要,我们正在这样做。但是你会在单位上得到一些基数效应。我的意思是,关于市场上的混合有很多讨论。

我只是认为这通常就是这个市场的运作方式。当然,随着组件的变化,配置也会发生变化。坦率地说,我们在23年看到了这一点。突然之间,组件混合比例大幅上升,因为价格大幅下降。突然之间,1TB的硬盘变得非常便宜。突然之间,它开始出现在任何地方。随着市场向另一个方向走一点,你会看到那种变化。我认为那只是这个市场运作的自然方式。

我不认为这是值得过度担心的事情。所以那些仍然是强劲的市场。客户关系非常好。我预计我们将继续深入参与这些市场。

我们在边缘拥有强大的影响力已经很长时间了,我们将继续保持。从大局来看,这就是为什么我认为这个业务如此有价值的原因之一,是因为我们涉足每一个单一的设备,每一个单一的技术,接触——我们接触它或向它出售NAND。现在随着云端的AI部署和那个市场成为NAND最大的市场,它正在改变整个行业运作的动态。正如我们在准备好的发言中所说,我们在——我们在过去25年里投入了大量的研发以达到我们现在的位置。

我们投入了大量的资本以达到我们现在的位置,我们可以制造所有这些,前端和后端。我认为我们终于开始达到这一点,即这种知识产权的价值,这种强度的价值正在我们自己的结果中得到认可。Luis Visoso,执行副总裁兼首席财务官:

是的,我认为回答你关于跨周期利润率的问题的方式类似于David留下的,即在一个高资本支出、高研发的行业或公司,坦率地说,35%不是我们想要的地方,对吧?所以我们今天不会给你一个新的数字,但很明显那不是我们想要的地方。我要告诉你的是这是第一个季度,对吧?我们高于35%,达到了51%,我们正在达到,称之为中点66%,所以我们正在取得进展,我们正在达到一个我们相信我们可以证明资本支出合理,我们可以证明业务所需的研发投资合理的地方。接线员:

下一个问题来自巴克莱的Tom O'Malley。请讲。分析师:

嗨,这是Matthew Panon代替Tom O'Malley。我只有一个简短的问题,如果你们提到过请见谅,只是在电话会议期间跳来跳去。

我想知道你们是否说了季度内企业级SSD占总位元出货量的百分比?Luis Visoso,执行副总裁兼首席财务官:

我不认为我们说过那个,但它大概是在那个高十位数(high teens,约16%-19%)的范围内。接线员:

下一个问题来自Jefferies的Blayne Curtis。请讲。Blayne Curtis:

嘿,伙计们。

祝贺,谢谢让我插进来。我只想谈谈模型,很明显,我的意思是两个季度的销售额翻倍。我想只是确定我理解你们将如何处理OpEx。我想占收入的百分比现在减半了,对吧?所以,你们会加速你们看待投资研发的方式吗,还有税率,随着这种显著提高的盈利能力,关于税率有什么要考虑的吗?我想你们在谈论它可能在某个时候达到20%,那是迟早的事吗?Luis Visoso,执行副总裁兼首席财务官:

是的。

所以在OpEx方面,首先你应该知道我们大约75%的OpEx是研发。那是我们投钱的地方,我们为什么要那样做?因为这是一家科技公司,创新是我们的命脉。那是我们相信的,那是我们投钱的地方。所以,你不应该把这个季度的OpEx看作是我们应该在哪里的指示,因为那,正如我之前提到的,有一个非经常性的收益。如果你想量化那个,那个数字大约是3500万美元,所以你可以用那个数字来做你的模型。

我们认为OpEx不应该从今天的水平显著升高。我们相信运行率是健康的。我们将始终关注我们需要投资的地方,并确保我们为创新提供资金,但在另一方面我们也一直在关注效率,以及我们如何确保系统中没有浪费。所以说了一大堆,也就是上季度的支出水平,我们这季度得到的,那些是目前更可持续的水平。

税率很有趣,因为我们有很多以前年度的亏损,特别是在马来西亚积累的,我们消耗得非常快。当你开始产生利润时就会发生这种情况,所以我认为你应该看到我们的税率会在比今天高一点的地方徘徊,也许在持续的基础上是14%-15%。那就是我现在会建模的。接线员:

我们的问答环节到此结束。

我想把会议交还给David做任何结束语。David V Goeckeler,董事长兼首席执行官:

好的。谢谢大家加入我们。我们将在整个季度保持沟通。

祝大家有愉快的一天。谢谢。接线员:

会议现已结束。感谢参加今天的演示。

您现在可以断开连接。活动已结束。