本周,“AI 颠覆一切” 的狼终于来了

大摩警告,市场对 AI 颠覆风险的定价呈多米诺效应:一个月内,欧洲指数面临风险的权重从 4% 飙升至 24%。GPT-5.2 已在 71% 专业任务上达到人类专家水平,五个月前这一数字仅为 24%。建议避开易被复制的软件与银行股,拥抱无法被 AI 复制的 “价值锚点”,如公用事业、国防及实物资产,同时关注算力短缺危机。

市场终于意识到,AI 颠覆不再是遥远的威胁。

2 月 14 日,据追风交易台消息,摩根士丹利在最新研报中称,随着 AI 模型以非线性、加速度推进,市场对颠覆风险的定价也开始呈现多米诺骨牌效应:

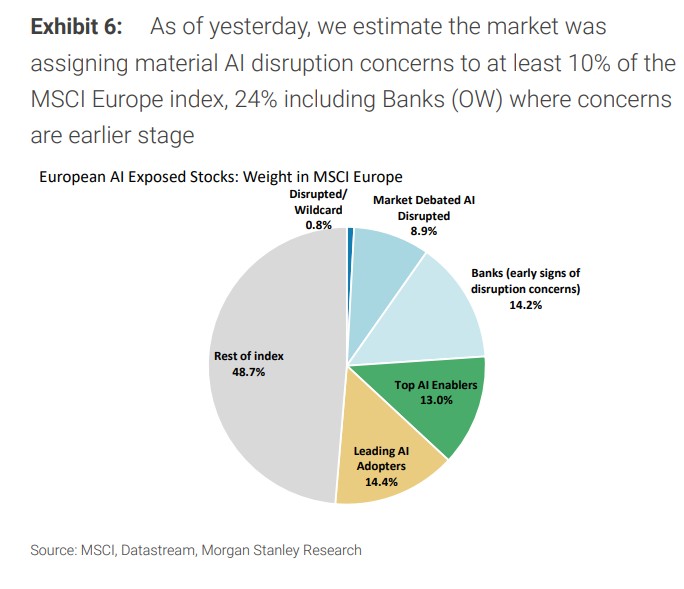

仅仅一个月前,市场认为约 4% 的 MSCI 欧洲指数权重面临 AI 颠覆风险;一周前这一比例升至 7%;而 2 月 13 日,这个数字已跃升至 24%(包含银行板块)。

研报指出,大摩认为,随着前沿 AI 模型能力突破临界点——GPT-5.2 在 71% 的专业任务上已达到或超越人类专家水平——投资者必须重新审视资产配置逻辑。

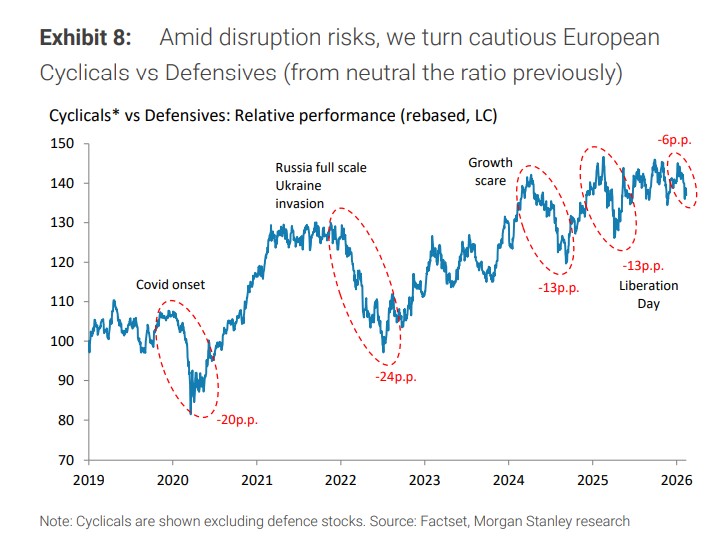

摩根士丹利已将立场从中性转向谨慎看待周期股相对防御股,并指出欧洲信贷市场提供了便宜的下行对冲机会,重点关注公用事业、半导体、国防和烟草等被视为最具韧性的避风港。

该行强调,需要重新审视哪些资产无法被 AI"复制"——这些将成为新时代的价值锚点。在一个智力和劳动力可以被无限复制的时代,真正的价值将回归那些无法复制的东西——物理资产、监管壁垒、网络效应、人类体验、专有数据。

AI 能力的惊人跃升:71% 的专业任务已被攻克

人类不擅长理解非线性变化,而 AI 模型的进步正是典型的非线性加速。

大摩表示,数据显示惊人的进展速度:2025 年 7 月推出的 Grok 4 在 GDPVal 测试中得分 24%,意味着该模型在 24% 的真实专业任务上能达到人类专家水平;而仅仅五个月后,2025 年 12 月 12 日发布的 GPT-5.2 得分已飙升至 71%。

GDPVal 是什么?这是衡量 AI 模型在真实世界知识工作中表现的指标,涵盖各行各业经验丰富专业人士的实际任务。OpenAI 的研究发现,前沿模型完成这些任务的速度比行业专家快约 100 倍,成本低约 100 倍。

研报强调,更令人震撼的是即将到来的突破。如果大语言模型(LLM)训练的规模定律在 2026 年继续有效——摩根士丹利认为这很可能——预计 2026 年上半年将推出多个美国前沿 LLM,其能力将远超当前模型。原因很简单:美国五大 LLM 开发商目前训练下一代模型所用的计算能力,是当前模型的约 10 倍。

颠覆风险的多米诺效应:从软件到银行

市场认知的变化速度同样惊人。

摩根士丹利的追踪显示,市场最初只是开始质疑软件行业未来几年的收入增长可能急剧放缓,但很快这种担忧就像多米诺骨牌一样扩散到更广泛的经济颠覆风险——竞争格局变化、就业影响、通缩压力等。

这让人想起 2020 年初新冠疫情的市场心理演变:1 月份还只是需求和供应链风险,2 月份扩大到旅游休闲、工业、银行等行业,到 3 月份就演变成全面市场抛售,最终触发重大政策行动。

目前,摩根士丹利估计约 10% 的 MSCI 欧洲指数权重(不含银行)被市场认为面临实质性 AI 颠覆担忧,如果包含银行则达到 24%。银行板块的担忧相对较新,主要集中在更广泛的经济通缩和就业问题,以及(程度较轻的)与 AI 相关的存款竞争担忧。

值得注意的是,这些"市场辩论中的颠覆股"已经从 2025 年初的峰值市盈率 24 倍,下跌到今天的 16.4 倍。但摩根士丹利警告,参照那些"无争议颠覆股"的估值走势(从 24.7 倍跌至 11.1 倍),估值可能还有进一步下行空间。

谁能在 AI 时代幸存?

面对这场颠覆风暴,摩根士丹利提供了一套评估框架,结合五个维度来判断板块和个股的抗风险能力:

AI 暴露程度:是被颠覆方、"市场辩论中的颠覆对象"、赋能者还是受保护方

业务性质:提供服务、实物资产、商品还是算力

周期性:周期股、防御股还是其他

投资者持仓:当前仓位水平

个股动量:基本面叠加因素

基于这一框架,摩根士丹利认为最具韧性的板块依次为:公用事业、半导体、国防、烟草和个人与家庭护理用品。

大摩称,欧洲公用事业公司几乎包揽了最抗颠覆榜单的前 20 名。这些公司的共同特点是:提供 AI 无法复制的实物基础设施,属于防御性行业,且在当前环境下相对低配。

相反,软件、商业服务、媒体娱乐、旅游休闲等服务密集型板块,以及运输、多元化金融、银行等板块,被认为面临最高的颠覆风险扩散压力。

无法被 AI 复制的八大资产类别

与此同时,摩根士丹利强调,一旦 AI 达到变革性水平,那些无法被 AI"复制"的资产类别价值将会上升。这是理解未来资产配置的关键框架:

A、物理稀缺性:房地产、能源和电力资产、交通基础设施、数据中心、矿产金属、水资源、有限司法管辖区的赌场牌照、主题公园土地、邮轮港口和码头权、频谱许可、光纤电缆网络等。

B、具有定价权的 AI 采用者:能够证明定价权的门槛正在提高。

C、独特的奢侈品、房产和服务。

D、网络效应:大型科技平台、在线市场、拥有患者关系的医疗保健业务。

E、真实独特的人类体验:拥有强大品牌的媒体业务、体育资产/球队、音乐和其他重视人类元素的表演。

F、监管稀缺性:拥有各种许可证、审批和受保护特许权的业务。

G、专有数据和品牌:拥有专有数据集和 IP 库的 AI 采用者。

H、一系列半导体资产:如领先制程、ASML 的 EUV 光刻、台积电的制造专长、芯片稀土加工。

信贷市场:便宜的下行保护

尽管 AI 颠覆担忧已开始影响部分信贷市场,尤其是杠杆贷款领域,但欧洲投资级利差仍徘徊在全球金融危机后的低位附近。即使股市隐含波动率一直在上升,信贷波动率也异常低迷。

但如果 AI 颠覆担忧扩散到更多板块(加上预期中的发行加速),可能开始挑战信贷市场的韧性。

摩根士丹利认为,信贷期权市场为投资者提供了很好的切入点,可以为利差扩大做准备。考虑到欧洲相对较低的科技暴露、整体收益率仍处高位、政策支持以及经济增长韧性,这些对冲工具的性价比尤其突出。

算力需求缺口:一场看不见的供应危机

在 AI 颠覆的另一面,是对算力基础设施的疯狂需求。多个数据点显示,算力需求的增长速度远超当前供应预测:

- 谷歌高管最近表示,公司可能需要每 6 个月将算力翻倍,"4-5 年内达到 1000 倍"。作为对比,摩根士丹利预测 2025-2028 年英伟达算力销售的年复合增长率约为 210%;推算 5 年期,累积算力约为 300 倍——远低于谷歌所需的 1000 倍以上。

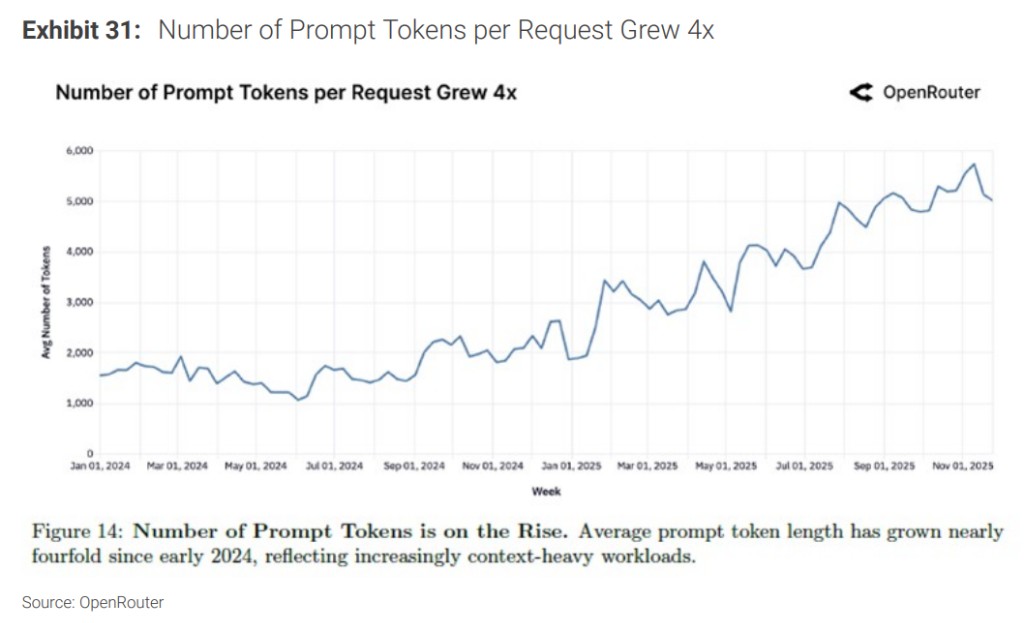

- OpenRouter 数据显示,从 2024 年 11 月底到 2025 年 11 月底,每周平均 token 需求增长超过 2200%。Token 使用是算力需求的直接代理指标。

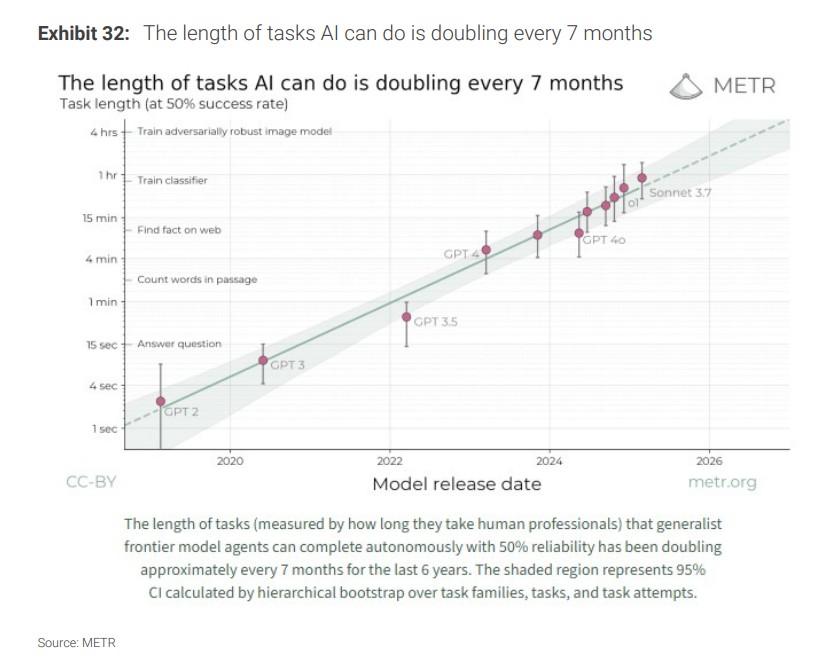

- 更关键的是,单个 LLM 查询的计算强度正在快速上升。研究机构 METR 指出,AI 每次客户查询所执行的"工作"平均时长每 7 个月翻一番。

据研报,即使客户数量不变,这种增长也意味着算力需求的增速将显著高于英伟达约 120% 的年复合增长率预测。

大摩称,这种供需失衡已经在市场上显现:

CoreWeave 能够以原价格 95% 的水平续租老一代英伟达 GPU(Hopper),远高于芯片随时间经济折旧所暗示的价格;

谷歌为 Anthropic 和 FluidStack 担保的"供电外壳"租赁交易,给比特币矿商 Hut8 带来约 18.5% 的无杠杆资本回报率,相当于电力接入溢价约 300%。