Why does gold react with such volatility in the face of a crisis?

美伊衝突加劇,黃金為何反常大跌?德銀最新研報打破 “危機必漲” 錯覺:黃金避險溢價極具不確定性與滯後性。當前做多黃金的真正硬邏輯,在於其在美元強勢走勢下展現出的價格韌性,反映出黃金存在獨立於美元的需求支撐。

3 月 3 日,美伊衝突加劇,市場避險情緒升温,股市下跌,油價大漲,但核心避險資產黃金卻一度 4.9%。

據追風交易台,德銀 2026 年 3 月 3 日發佈報告《黃金變化的危機溢價》,報告指出,黃金對地緣政治危機的反應存在高度不確定性,平均而言確實正向,但個體事件分散度極大,投資者切忌將"危機必推金價"視為鐵律。

更值得關注的是,黃金已展現出相對美元隱含水平的正向超越,這一結構性信號比危機溢價本身更具説服力,為投資者提供了更穩健的做多邏輯。當前黃金價格仍對本週美元的強勢走勢表現出一定的抗跌性。

危機中的黃金:平均正向,但價格反應需要 1 至 2 周

每當地緣政治緊張局勢升温,市場本能地將目光轉向黃金。然而,德意志銀行研究分析師 Michael Hsueh 指出,這種"危機避險=買黃金"的直覺邏輯,在統計層面遠比想象中脆弱。

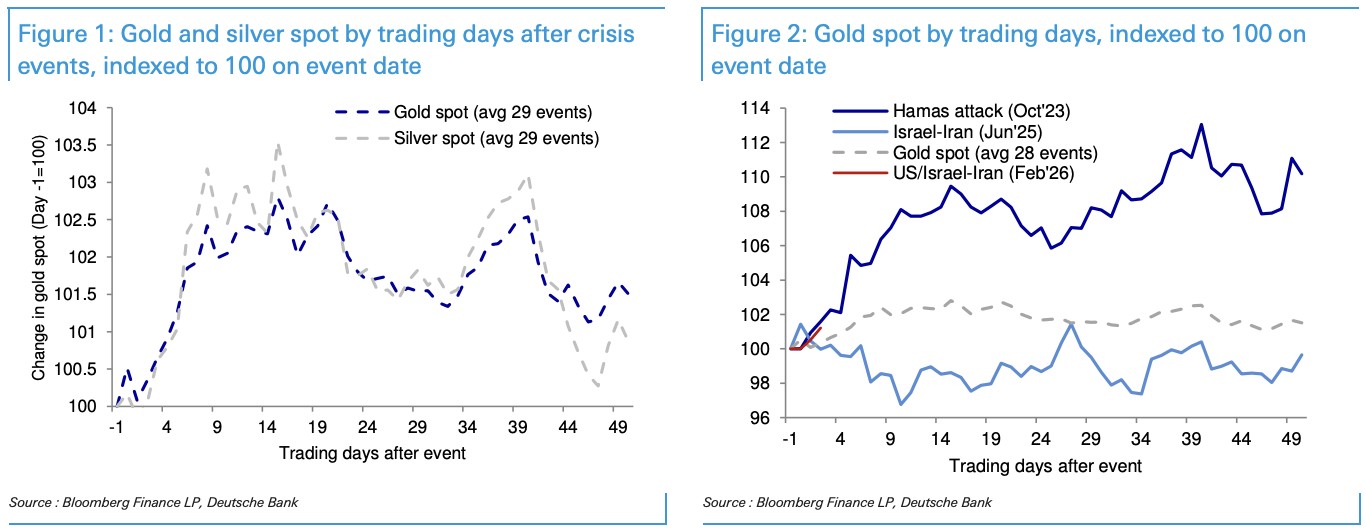

研究團隊梳理了自 1987 年以來 29 個危機事件後黃金的表現,得出以下核心結論:

-

黃金對危機的反應通常需要 1 至 2 周才能充分釋放,而非立竿見影;

-

黃金的危機響應可靠性較低,個體事件之間存在極大分散度,即便剔除傳統價值驅動因素後的殘差分析,同樣如此;

-

白銀雖傾向於跟隨黃金走勢,但超額表現有限,並非更優的危機交易載體。

事件分散度極大:平均值掩蓋了真相

29 個危機事件的平均線背後,隱藏着令人警醒的事實:在 29 個事件中,有 24 個事件裏,黃金在事件發生後的前 25 個交易日內,出現過低於事件當日初始價格的階段性回落。 換言之,即便危機爆發,持有黃金也絕非穩賺不賠的交易。

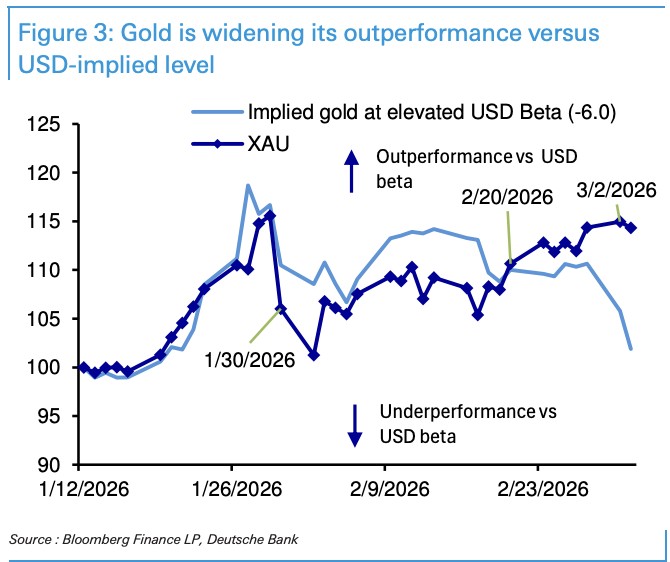

兩個近期事件的對比最為直觀地揭示了這種差異:

-

2023 年 10 月哈馬斯襲擊事件:黃金在事件後大幅走強;

-

2025 年 6 月以色列對伊朗的空襲:黃金反應則相對温和;

-

兩者之間在不同時間節點的最大價格差距高達10% 至 13%,遠遠超過歷史危機風險溢價的最高峰值——即在第 15 至 20 個交易日時約 2.7% 至 2.8% 的溢價幅度。

值得注意的是,黃金危機溢價的峯值往往並不出現在事件初期,而是在危機刺激後的數週內才逐漸顯現。這意味着投資者不宜因短期價格波動而過度解讀或倉促操作。

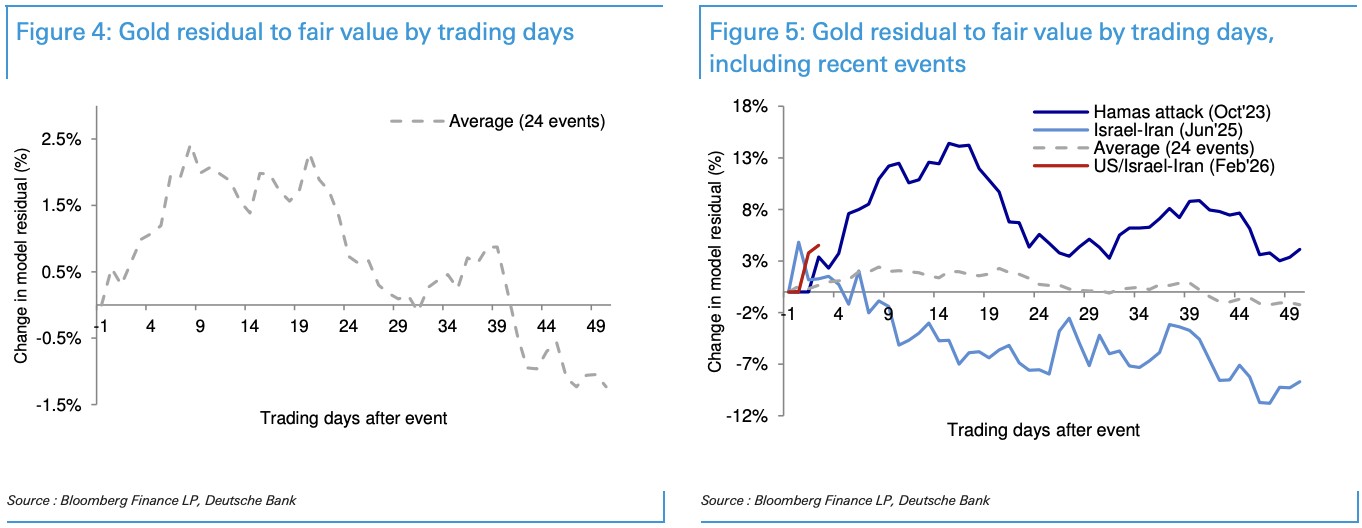

更具説服力的信號:黃金相對美元隱含水平的正向突破

相較於危機溢價這一不穩定變量,德意志銀行認為,當前黃金存在更為紮實的做多依據——上週出現的相對美元隱含金價的正向偏離,正在進一步擴大。

分析師通過黃金與美元滾動貝塔係數的比較模型,發現黃金自上週起開始持續跑贏美元貝塔所隱含的定價水平,且這一差距在本週隨着美元走強而進一步擴大。美元升值理論上應壓制金價,但黃金交易價格區間仍展現出相當的韌性。

這一"正向交叉"意味着:黃金已不僅僅依靠傳統的美元/利率邏輯維持價格,背後存在獨立於美元走勢之外的需求支撐。德銀認為,這是構建黃金多頭偏好更為堅實的基礎,而危機風險溢價的潛在疊加則將是額外的上行催化劑。

公允價值模型的進一步印證黃金危機溢價

為了剝離危機情緒對金價的直接衝擊,德銀研究團隊還對黃金相對公允價值模型的殘差進行了分析。即在排除美元、利率等傳統驅動因素後,單純評估危機帶來的額外溢價。

結論與現貨分析高度一致:黃金的公允價值殘差在危機事件後同樣傾向於擴張,且擴張最為明顯的階段集中於前 8 個交易日。此後,這一溢價趨於回落,甚至進入折價區間。

這再次表明:危機帶來的金價彈性是真實存在的,但時效性有限、個體差異懸殊。對於當前美國/以色列 - 伊朗局勢,關鍵觀察點在於:並非所有危機相關反應都在最初一兩天內兑現,後續演變路徑仍存在較大不確定性。

投資啓示:理性看待危機溢價,聚焦結構性信號

綜合以上分析,德銀對黃金維持近期正向偏好,但邏輯支撐有以下優先級排序:

-

首要依據:黃金相對美元隱含水平的正向超越,這是更具穩定性和可持續性的結構性信號;

-

次要催化劑:地緣政治危機溢價的潛在累積,其高峰通常出現在事件發生後 1 至 2 周;

-

需要警惕的風險:危機溢價的高度不確定性,歷史上超過八成的危機事件中,黃金曾在前 25 個交易日內出現階段性低於事件基準價的情況。

對於投資者而言,黃金在危機中"上躥下跳"的背後,是歷史規律的本質揭示:它是一個有效的危機對沖工具,但絕非每次危機都能給出穩定且可預測的回報。

在當前黃金展現出相對美元走勢獨立性的背景下,做多黃金的邏輯相對清晰,但倉位管理與時間維度的把握同樣至關重要。