The asymmetric cost! The Iran war "for every day it lasts," the damage to the global economy "is measured in months"

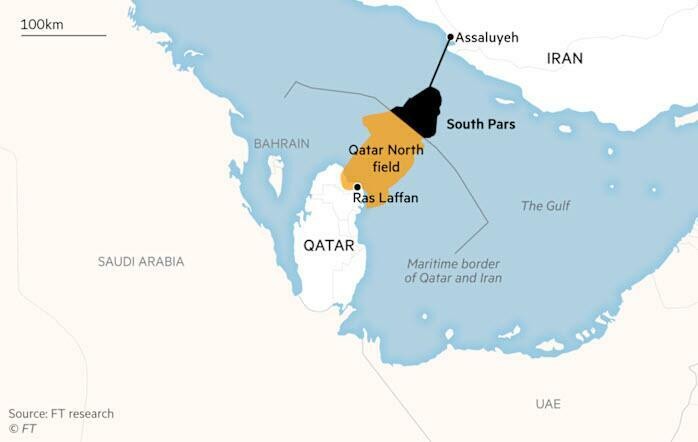

Iran's missile attack on Qatar's Ras Laffan LNG facility has caused approximately 17% of export capacity to be damaged, with a repair period lasting three to five years. Qatar's case is a microcosm, compounded by American oil and gas companies' refusal to expand production and the narrowing of the Federal Reserve's monetary policy space. This mismatch of a "few minutes of destruction and years of repair" is continuously amplifying the cost of the Middle East conflict into a long-term shock for the global economy

Oil and gas infrastructure can be destroyed in minutes, but it takes years to repair. This severe mismatch in timelines is amplifying the cost of each day of conflict in the Middle East into months or even years of sustained damage to the global economy.

According to CCTV News, on Thursday, March 19, Saad al-Kaabi, CEO of Qatar Energy, stated that the LNG export facility damaged by the Iranian missile attack is expected to take three to five years to repair, with a loss of export volume of approximately 12.8 million tons per year, leading to an estimated annual revenue loss of about $20 billion.

Unlike the oil market, the LNG market has almost no strategic reserve buffer mechanism. Neil Beveridge, head of research at Bernstein, bluntly stated:

LNG has no strategic reserves.

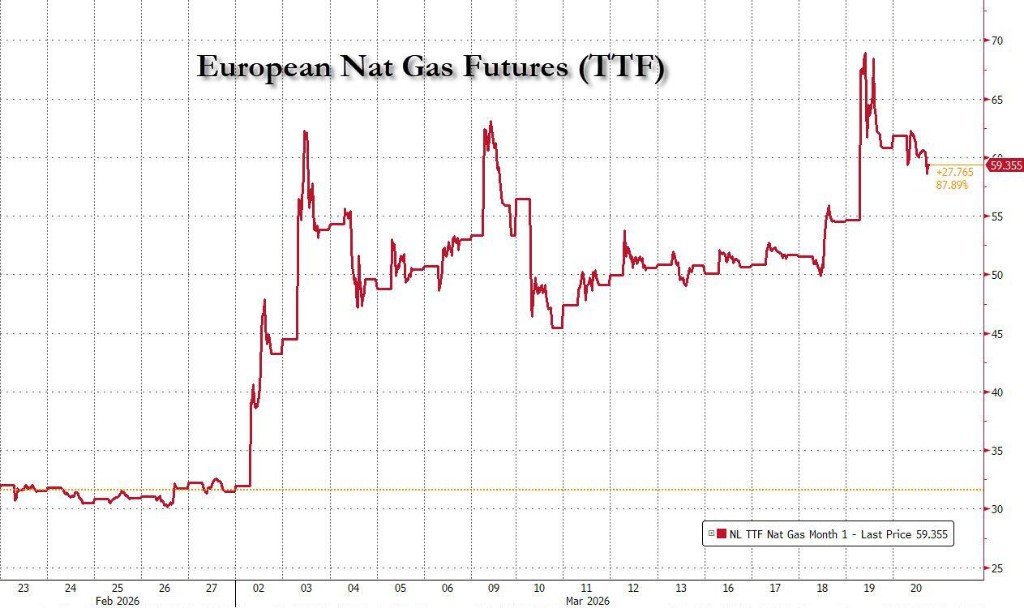

This means that once supply drops sharply, there is almost no buffer space in the market. Following the news, European natural gas futures prices surged by 35% on the same day, more than double the levels before the Iranian conflict. On Friday, prices slightly retreated.

The impact of this event has far exceeded the energy market itself. As Bloomberg commentator Tracy Alloway pointed out, the current situation in the Middle East creates a "huge mismatch in timelines," with each day of conflict impacting the global economy by months.

As the reality of long-term LNG supply contraction gradually emerges, global inflationary pressures and the repricing of energy markets are accelerating.

Qatar's Wound: One Strike, Five Years of Cost

According to CCTV News, some petrochemical facilities in Iran's southern Bushehr Province were attacked by U.S. and Israeli airstrikes. Iran subsequently announced strikes on oil facilities in Gulf countries such as Saudi Arabia and Qatar related to the United States.

Reports citing informed sources indicate that the target of the Iranian missile attack was the LNG production facility located in Qatar's Ras Laffan Industrial City.

It was reported that the 4th and 6th liquefaction trains among the 14 production lines were damaged, while the condition of the 5th train, located between the two, remains unclear. Additionally, one of the two gas-to-liquid (GTL) facilities was also affected Saad al-Kaabi stated that the damaged production capacity accounts for about 17% of Qatar's total LNG exports, and Qatar Energy will be forced to declare force majeure on some long-term contracts with European and Asian customers, with a maximum duration of up to five years.

Meanwhile, Qatar's condensate exports may decline by nearly a quarter, and liquefied petroleum gas (LPG) exports may also decrease by 13%.

The facility had previously halted production due to a drone attack, but this round of attacks is larger in scale and more destructive. Saad al-Kaabi clearly stated that production recovery is out of the question until hostile actions cease.

JP Morgan warns that the supply gap far exceeds previous expectations

JP Morgan's commodity analyst Otar Dgebuadze, in the latest research report, has lowered the normal production capacity utilization rate of Qatar's LNG from 90% to 80%, and significantly raised the estimate of Qatar's supply losses for the summer (March to October).

If the Strait of Hormuz reopens within a month after the conflict ends, the loss will reach 36 billion cubic meters, higher than the previous estimate of 25 to 30 billion cubic meters, and for every additional month of delay, the monthly loss risk will increase by another 7 billion cubic meters.

The bank assumes that LNG exports will start the restart process 30 days after the Strait of Hormuz reopens, expecting to reach 40% utilization within two weeks and recover to 80% within two months. An 80% utilization rate will become the new normal upper limit for Qatar's facilities in the medium term.

JP Morgan also warns that the risk direction of the above estimates is biased downward, and the actual recovery progress may be slower. Based on this, JP Morgan concludes that this incident further undermines the market's previous judgment of an LNG supply surplus.

Combining the delays in Qatar's new capacity trains before the Middle East conflict and the greater uncertainties facing expansion plans, the bank believes that long-term European natural gas benchmark prices have not fully reflected the above risks.

Asymmetry of the timeline and the deeper logic of energy shocks

Qatar's case is just a microcosm of a larger crisis of timeline mismatch.

Bloomberg commentator Tracy Alloway pointed out that it takes only minutes to destroy energy infrastructure, but rebuilding takes months or even years. This reality determines that for every day the Iran conflict continues, its impact on the global economy will accumulate exponentially.

Wall Street Journal previously mentioned that Goldman Sachs reviewed the five largest supply shocks in the past 50 years and calculated that the affected countries still have an average production loss of 42% four years later. The main reasons are usually the physical destruction of infrastructure such as oil fields, pipelines, and ports, as well as severe underinvestment in subsequent periods.

Therefore, Goldman Sachs emphasizes that if Iran and the surrounding region's production potential suffers substantial damage, oil prices may remain above $100 in risk scenarios for a much longer time than the market currently expects.

Meanwhile, even the United States, which is usually seen as energy independent, finds it difficult to remain unaffected. According to Baker Hughes data, the gap between the number of oil and gas rigs in the United States and the soaring oil prices is rapidly widening, and the surge in oil prices has not led to an immediate supply response.

According to the Financial Times, U.S. oil and gas operators are generally reluctant to rashly expand production when prices rise sharply, having deeply learned the lessons from the boom and bust cycle of shale oil in the 2010s, with capital discipline becoming the primary constraint imposed by shareholders on management.

Pressure at the monetary policy level is also rising. Bloomberg reports that Federal Reserve Chairman Jerome Powell's statements have become increasingly hawkish, and the market is currently pricing in a slight expectation of interest rate hikes for the remainder of this year.

Against the backdrop of inflation already being persistently above target and trending upward before the conflict, the oil price shock has further compressed the maneuvering space for monetary policy.

As the conflict enters its third week, the outcome remains unclear, while the global energy market is preparing for a prolonged cost calculation.