Sanhua's 2025 Revenue Reaches 31 Billion Yuan, Up 11% YoY; Net Profit Attributable to Parent Jumps Over 31% | Financial News

Sanhua's 2025 financial report shows full-year revenue of 31.011 billion yuan, a year-on-year increase of 10.97%; net profit attributable to parent company shareholders was 4.063 billion yuan, a year-on-year increase of 31.10%. The net profit margin improved to 13.1%. The refrigeration and air conditioning components business remained stable, while the new energy vehicle thermal management business became a core growth engine. The company successfully listed on the Hong Kong Stock Exchange in June 2025, significantly strengthening its capital base. Additionally, the company is extending its precision manufacturing technology to the field of bionic robot mechatronic actuators, establishing a third growth curve

Sanhua has delivered a solid annual report.

On March 23rd, Sanhua released its 2025 annual report. The financial filing shows that the company achieved full-year operating revenue of 31.011 billion yuan, a year-on-year increase of 10.97%; net profit attributable to shareholders reached 4.063 billion yuan, a significant year-on-year increase of 31.10%, with profit growth significantly outpacing revenue growth, indicating a continuous improvement in profitability quality.

Key financial data are as follows:

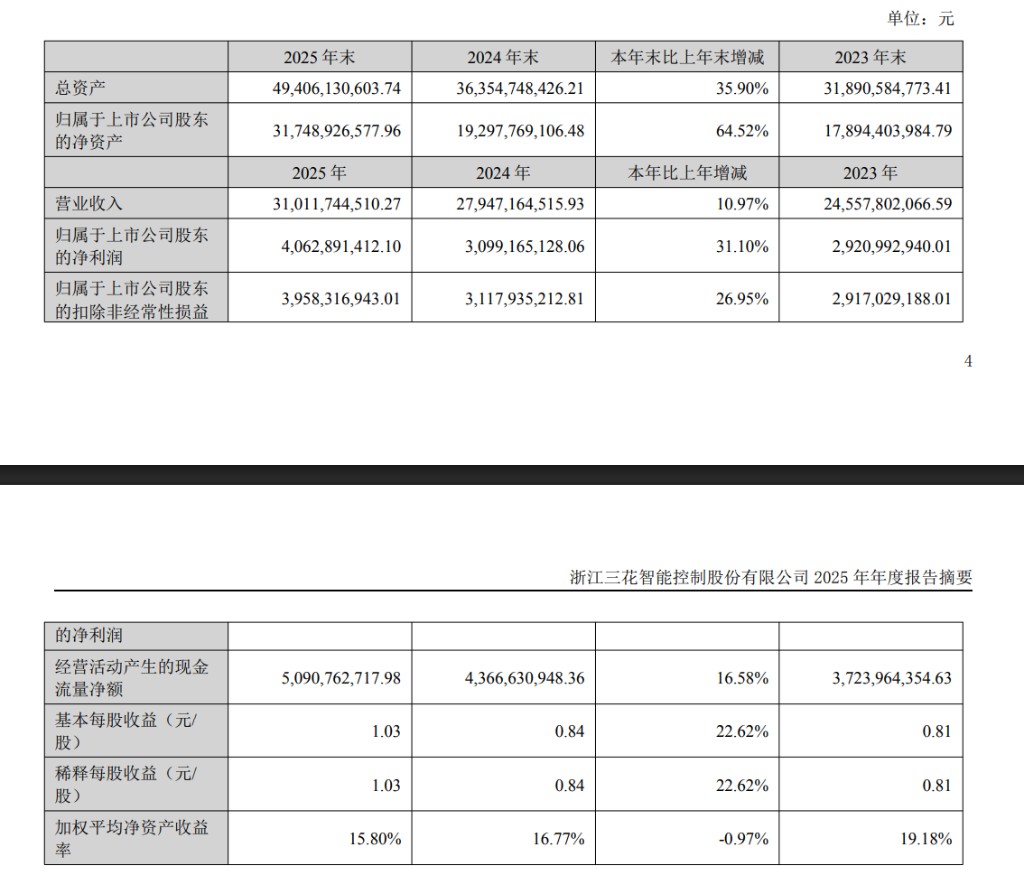

- Full-year operating revenue in 2025 reached 31.012 billion yuan, a year-on-year increase of 10.97%;

- Net profit attributable to parent company was 4.063 billion yuan, a year-on-year increase of 31.10%;

- Net profit after non-recurring items was 3.958 billion yuan, also an increase of 26.95% year-on-year;

- Net cash flow from operating activities was 5.091 billion yuan, a year-on-year increase of 16.58%;

- Total assets were 49.406 billion yuan, a year-on-year increase of 35.90%;

- Net assets attributable to parent company were 31.749 billion yuan, a year-on-year increase of 64.52%.

In terms of asset structure, the company's total assets reached 49.406 billion yuan by the end of the year, a year-on-year increase of 35.90%; net assets attributable to shareholders surged to 31.749 billion yuan, a substantial year-on-year increase of 64.52%. This leap in growth is mainly attributed to the successful listing on the Hong Kong Stock Exchange in June 2025 – the global offering of H shares and the full exercise of the over-allotment option – which injected considerable equity capital into the company, significantly strengthening its balance sheet foundation.

As a core supplier in the global thermal management components sector, Sanhua is accelerating its transformation into a "multi-industry, multi-category" global industrial group, driven by the synergy between its two main businesses: refrigeration and air conditioning components, and new energy vehicle thermal management. The company also announced a cash dividend of 2.80 yuan (including tax) per 10 shares, to reward investors.

Revenue and Net Profit Both Increase, Net Profit Margin Rises to 13.1%, Second Quarter is the Peak for the Year

In 2025, Sanhua achieved operating revenue of 31.011 billion yuan, an increase of over 3 billion yuan from the previous year. Notably, the year-on-year increase in net profit was 31.10%, significantly higher than the revenue growth of 10.97%, demonstrating the effectiveness of economies of scale and cost control. The net profit margin improved from approximately 11.1% in 2024 to about 13.1%.

From a quarterly perspective, the year showed a "high first half, low second half" trend. In the first quarter, revenue was 7.669 billion yuan and net profit was 0.903 billion yuan; the second quarter peaked at 8.593 billion yuan and 1.207 billion yuan, both marking the annual high, aligning perfectly with the peak season for new energy vehicle inventory and the summer demand for refrigeration and air conditioning. The third quarter saw a decline to 7.767 billion yuan and 1.132 billion yuan; the fourth quarter further dropped to 6.982 billion yuan and 0.821 billion yuan, showing a significant seasonal decline, mainly due to factors such as the cooling demand after the withdrawal of domestic appliance subsidies and pressure on export markets.

Dual-Wheel Drive: Steady Performance in Refrigeration Components, Rapid Advancement in New Energy Vehicles

Refrigeration and air conditioning components remain Sanhua's most important bedrock. In 2025, extreme weather conditions drove global demand for air conditioners, while stricter environmental standards in North America and the EU promoted refrigerant substitution and energy efficiency upgrades, creating strong demand for the company's core products such as electronic expansion valves, four-way reversing valves, and microchannel heat exchangers. Despite a slight year-on-year decrease of 1.2% in domestic household air conditioner production and sales, and a 7.4% drop in domestic central air conditioner sales, the company effectively offset domestic sales pressure through its deep partnerships with leading clients like Gree, Midea, Haier, Daikin, and Panasonic, as well as its active expansion into export markets (central air conditioner exports increased by 12.7% year-on-year).

The automotive components business is the core engine driving high profit growth. In 2025, global sales of new energy vehicles reached 22.62 million units, a year-on-year increase of 29.04%, with China's market sales reaching 16.49 million units, up 28.2% year-on-year, achieving a penetration rate of nearly 48%. Sanhua is deeply integrated into the supply chains of leading new energy vehicle manufacturers such as BYD, Li Auto, Nio, Xpeng, and Leapmotor, while also supplying major global automakers like Volkswagen, BMW, Toyota, and Tesla. Its strategic products, including electronic expansion valves, electronic water pumps, and plate heat exchangers, have seen both volume and price increases, fully benefiting from the rapid industry growth.

H-Share Listing: A Key Strategic Move in Capital Operations

On June 23, 2025, Sanhua officially listed on the Main Board of the Hong Kong Stock Exchange under the stock code 2050, with an issue price of HK$22.53 per share. The total number of H shares issued globally (including the exercise of the over-allotment option) was 476,536,400, marking a milestone event in the company's capital operations history.

The H-share listing holds multiple strategic significances for the company: Firstly, it significantly bolstered its capital base, leading to a 64.52% year-on-year increase in net assets, providing ample resources for global capacity expansion; Secondly, it enhanced its international visibility and brand influence, aiding in expanding its customer base in mature markets such as Europe, North America, and Japan; Thirdly, it established diversified financing channels, reducing reliance on a single capital market and strengthening long-term financial resilience.

Research and Development and Emerging Businesses: Strategic Positioning in the Robotics Sector

As of the end of 2025, Sanhua possessed six R&D centers, holding a total of 4,680 granted patents, including 2,560 invention patents. Its R&D investment remained at a high level within the industry. The company adheres to a product iteration strategy of "mass-producing one generation, designing one generation, and conceptualizing one generation," ensuring continuous leadership in technological generational competition.

Notably, the company is extending its accumulated expertise in precision valve and pump manufacturing technology to the field of bionic robot mechatronic actuators, opening up a third business growth curve. Embodied intelligence is becoming a new frontier in global technological competition. The stringent requirements for precision transmission, torque control, and miniaturization in robotic joint actuators align perfectly with the company's precision machining and automated manufacturing capabilities developed in the thermal management components sector. Although this business is still in its early stages of development, success in securing key robot clients could open up new growth avenues for the company in the "post-new energy vehicle era."