Global Central Banks Sold $90 Billion in US Treasuries Since the Iran War

美伊衝突爆發以來,全球外國央行連續五週拋售美國國債,累計規模超 900 億美元,持倉降至 2012 年最低。土耳其領銜,泰國、印度等跟進,各國爭相變現美元儲備以應對外匯干預、能源進口及國防開支壓力。與此同時,摩根士丹利數據顯示,外國投資者持有美債佔比已跌至 32.4%,為 1997 年來最低。

自美伊衝突爆發以來,全球外國央行持續拋售美國國債,規模之大、速度之快引發市場高度警覺,美債市場正面臨多重壓力疊加的嚴峻考驗。

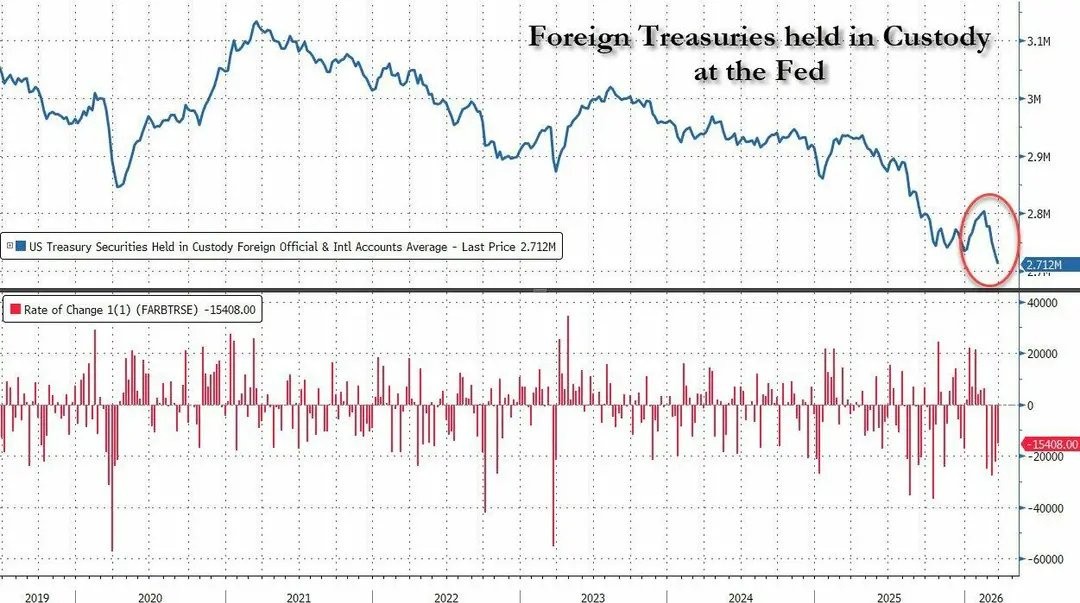

紐約聯儲託管數據顯示,自衝突爆發前一週(2 月 25 日當週)起,外國貨幣當局已連續五週淨賣出美國國債,累計拋售規模超過 900 億美元,且賣壓主要集中於最近三週。美債持倉規模已降至 2012 年以來最低水平。

此輪美債拋售的直接動因在於各國對美元流動性的迫切需求。從外匯市場干預到支付能源進口賬單,再到國防開支融資,美元需求的全面激增正迫使各國央行變現手中最具流動性的美元資產——美債。

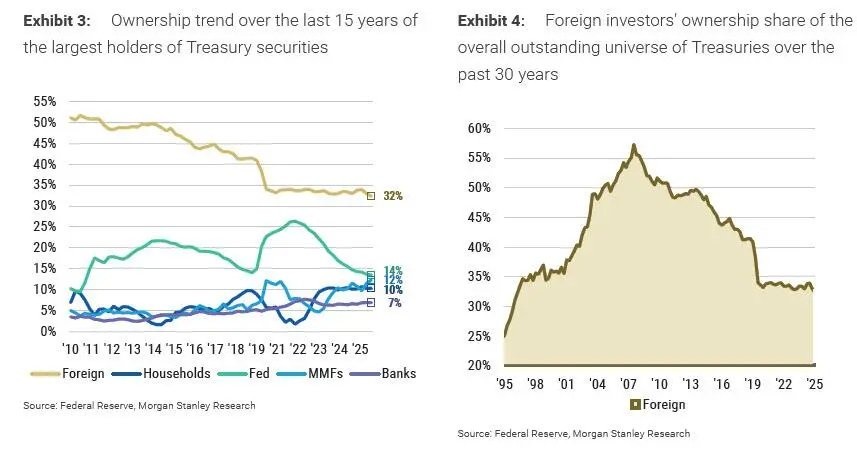

此輪拋售發生在美債市場本已承壓的背景之下,中東衝突引發的通脹擔憂推動兩年期和十年期美債收益率本月漲幅創 2024 年以來最大,政府、企業及居民借貸成本隨之攀升。與此同時,摩根士丹利最新報告顯示,外國投資者持有美債佔比已降至 1997 年以來最低水平,進一步加劇市場對美債需求結構性弱化的擔憂。

五週拋售逾 900 億,賣壓集中於近三週

紐約聯儲託管賬户數據顯示,外國央行自 2 月 25 日當週起連續五週減持美國國債,總計拋售規模超過 900 億美元,持倉降至 2012 年以來最低點。值得注意的是,拋售力度在最後三週明顯加速,表明隨着衝突持續,各國央行的流動性需求愈發迫切。

美國銀行美國利率策略師 Meghan Swiber 表示,"外國官方部門正在出售美國國債",並指出中東產油國可能也在出售相關資產以彌補石油收入缺口。Aegon 資產管理首席投資官 Stephen Jones 則將這一行為描述為各國"囤積戰備資金","他們正在提取應急儲備"。

另有分析人士指出,部分美債持倉或已轉移至紐約聯儲以外的其他託管機構,而非直接出售,但這種可能性相對較低。Swiber 同時強調,自 2012 年以來美債市場規模已擴大約兩倍,當前的拋售規模在此背景下尤為值得關注。

土耳其領銜拋售,多國動用外匯儲備

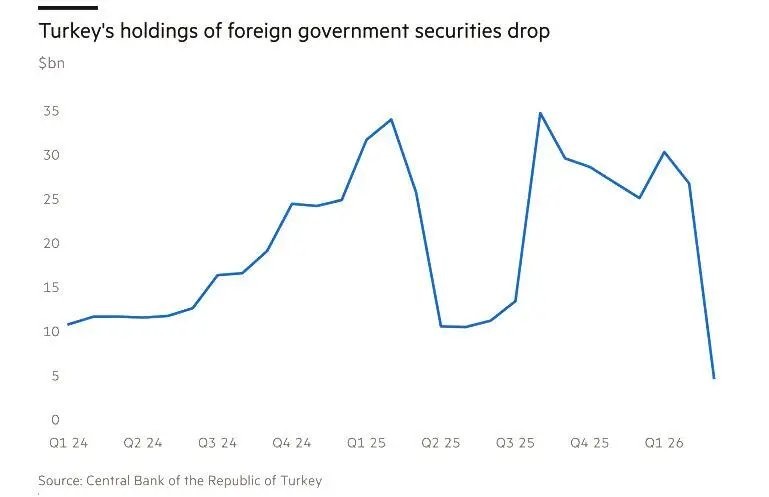

在已披露具體數據的國家中,土耳其的拋售規模最為突出。官方數據顯示,自 2 月 27 日(美國對伊朗發動攻擊前一天)起,土耳其央行已從外匯儲備中出售約 220 億美元外國政府債券,其中以美國國債為主。與此同時,土耳其還出售或互換了約 58 噸黃金,價值逾 80 億美元,此舉對金價形成明顯拖累。

泰國和印度央行的獨立數據同樣顯示,兩國外匯儲備自戰爭爆發以來持續下降,但目前尚不明確減少的部分究竟來自美債出售還是美元存款。分析人士預計,印度和泰國等以美元計價購買石油的國家,將面臨持續的儲備消耗壓力。

科威特、沙特阿拉伯和阿聯酋今年 1 月合計持有 3130 億美元美國國債,三國持倉自 2022 年以來整體呈上升趨勢,尤其是阿聯酋增持明顯。市場普遍預期,上述中東產油國也可能加入拋售行列,以應對戰爭帶來的國防開支和能源價格衝擊。

外國持倉佔比降至 1997 年低點

摩根士丹利利率團隊週末發佈的最新報告為上述拋售擔憂提供了更深層的結構性背景。該行基於美聯儲金融賬户(Z.1)數據的分析顯示,外國投資者持有美債佔總規模的比例已降至 32.4%,為 1997 年以來最低水平。

從細分結構來看,外國投資者持有的美債票息類證券(coupons)在 2025 年第四季度環比減少 563 億美元,是整體外國持倉下降的主要驅動因素;與此同時,短期國庫券(bills)持倉增加 318 億美元,創歷史新高達 1.45 萬億美元。

該行進一步指出,外國投資者持有票息類美債的比例自 2008 年峯值 64.4% 以來持續下滑,目前已接近數十年低點;外國投資者對票息類美債需求的季度環比變化自 2023 年中期以來持續走低,表明外國需求的結構性弱化早於本輪衝突便已形成趨勢。