Deep Dive into Kalshi – When "Everything is Tradable"

Bank of America stated that Kalshi is the fastest-growing prediction market platform in the U.S., holding a CFTC federal regulatory license. Its weekly trading volume has surged from $100 million to $3 billion, capturing over 90% of the U.S. market share. The 2024 election served as a breakthrough for its growth, with sports event contracts (accounting for approximately 80% of trades) becoming the core driver. The platform operates both a B2C application and a B2B exchange, theoretically possessing high profit margins with its fee-based model, generating an annualized revenue of about $1.5 billion and a valuation of $22 billion. Crypto assets are emerging as a second growth curve, with institutional adoption also advancing

Prediction markets are becoming a novel species in the United States: transforming elections, sports, interest rates, weather, crypto assets, and even pop culture into tradable prices through "yes/no" contracts. A research report by BofA Securities on the private company Kalshi is clear – this company has propelled "prediction markets" to the center of public attention with its federal regulatory license, explosive trading volume, and rapid product iteration speed.

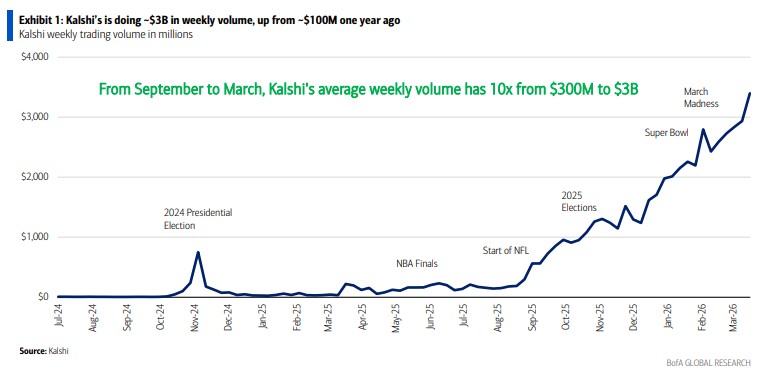

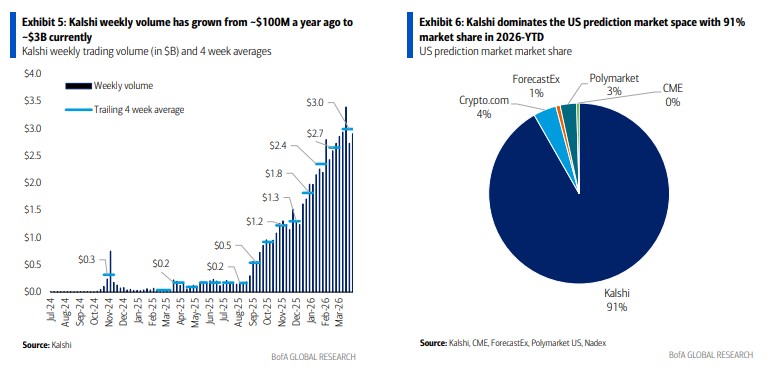

According to the "Chasing Wind Trading Desk," Bank of America Securities analyst Julie Hoover summarized Kalshi's presence in a recent report with one sentence: "Kalshi is the fastest-growing company in the non-AI sector." She highlighted its transformation with two figures – weekly trading volume soaring from approximately $100 million to over $3 billion, and a U.S. market share exceeding 90%. This is not a company whose valuation is propped up by "concepts"; its trading volume is expanding almost weekly.

Growth broke through the ceiling with political events, but sports have truly become the driver of trading volume today. As of March 2026, sports account for approximately 79%-80% of the platform's trades. Simultaneously, Kalshi is shedding its early reliance on channels – Robinhood once contributed about 60% of trades in Q2 2025, but by March 2026, this figure had fallen to about 23%, as Kalshi's own direct-to-consumer (B2C) platform rapidly strengthened.

However, Kalshi's story is not just about "traffic" and "sports." It operates both a B2C application and a B2B exchange, even integrating clearing and market-making capabilities. Its business model is driven by transaction fees, theoretically offering high profit margins. Greater potential lies in institutional use: directly hedging "discrete events" like geopolitical risks, weather, interest rates, and macroeconomic data through binary options, rather than inferring them from asset price correlations. The truly difficult aspect to price is regulation – is it financial trading or gambling? Lawsuits in 14 states, multiple bills in Congress, and disputes over federal and state regulatory authority make the "potential Supreme Court intervention" the biggest variable in this growth curve.

Weekly Trading Volume Jumps from $100 Million to $3 Billion in a Year: Elections Provided the Entry, Sports Delivered Compound Growth

Kalshi's national breakthrough point was the 2024 U.S. Presidential Election. Kalshi won a crucial ruling in its lawsuit with the CFTC in September 2024, securing the space to launch federal-regulated election contracts and subsequently introducing them to the public during the election cycle.

After the election, sports became the true "engine of trading volume." From a chart perspective, event windows like the Super Bowl and March Madness correspond to rapid increases in trading volume; by March 2026, sports trading accounted for approximately 79%. This explains how Kalshi could achieve a growth trajectory comparable to mass-market betting products within the seemingly niche category of "prediction markets."

Sports also offer a systemic advantage: Kalshi, as a federally regulated platform, can offer sports event contracts to all 50 states, whereas traditional online sports betting (OSB) is only legal in 38 U.S. states. Furthermore, Kalshi is open to users aged 18 and above, while most states have a 21-year-old minimum for sports betting. Coupled with Kalshi not bearing state gambling taxes (reports indicate OSB operators' gambling taxes can be around 33% of revenue), its customer base and cost structure are distinctly advantageous.

Operating Both an "Exchange + B2C App": Kalshi Turns Financial Infrastructure into a Consumer Product

Kalshi's positioning is clear from the report: it is a CFTC-regulated financial exchange that matches buyers and sellers through continuous bilateral bidding. The trading instruments are "event contracts" (typically "yes/no" questions, with a contract value of $1; payout $1 if the event occurs, $0 otherwise, with prices trading between 0 and 1).

Its distinctiveness lies in pursuing two paths simultaneously:

- B2C: Building its own app and website to reach users directly. Kalshi's app once climbed to second place overall in the Apple App Store during the Super Bowl. Its UI/UX has evolved from percentage odds to "American odds" similar to sports betting, a dark mode, a "six-icon grid" layout, and the rapid introduction of customizable parlays.

- B2B: Acting as an exchange to provide products and liquidity to third-party brokers and platforms, with partners including Robinhood, Webull, Coinbase, DriveWealth, PrizePicks, and others.

Early liquidity was primarily driven by B2B distribution, but data indicates a "disintermediation" trend: Robinhood's share of Kalshi's trading volume dropped from a peak of approximately 60% in Q2 2025 to about 23% by March 2026. This suggests Kalshi is replicating a common path: first achieving cold starts with large channels, then consolidating users and brand control back to its proprietary front end.

Transaction Fees Are the Core of Everything: The Premise for High Profit Margins is Not Losing Pricing Power to Competition

Bank of America clearly breaks down Kalshi's revenue: transaction fees are the main engine. If trades occur on Kalshi's proprietary platform, the average fee rate is approximately 1.5% of the trading volume (for 50/50 contracts, the fee for market takers is 1.75%, and for market makers, it's about 44 bps; fees are lower at extreme probabilities to encourage liquidity). B2B trades are revenue-shared with partners. The report provides an example: Robinhood charges users a 2% fee and roughly splits it 50/50 with Kalshi (calculated as 1 cent each per contract, totaling 2 cents).

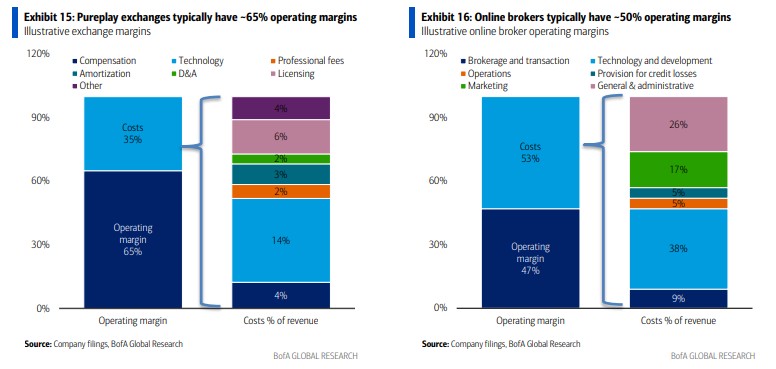

Key cost buckets include payment processing, marketing, personnel, and product technology. Operating purely as an exchange model yields a profit margin of about 65%, while an online brokerage yields 50%-55%. Kalshi's ultimate classification depends on whether it leans towards retail or institutional clients: retail implies higher marketing costs and potentially higher fees; institutional implies lower customer acquisition costs and higher operating leverage, but also potential compression of transaction fees.

In terms of valuation, Kalshi's annualized revenue run rate is approximately $1.5 billion. A $22 billion valuation corresponds to about a 15x revenue multiple, higher than the approximately 11x revenue multiple for public exchanges. This implies a gamble: that growth can be sustained, and that fee rates and regulatory advantages will not be rapidly eroded.

Over-reliance on Sports Isn't a Free Lunch: The Second Growth Curve is Currently Driven by Crypto

Sports contribute about 80% of the trading volume, also bringing concentration risk. The "non-sports" segment is the nascent form of Kalshi's second growth curve: non-sports currently accounts for about 20%, with crypto being the most significant driver – representing about 67% of non-sports trading and becoming the first non-sports category to exceed $1 billion in monthly trading volume in March. Politics (including elections) account for about 15% of non-sports, cultural events about 6%; other small categories include weather, interest rates, and finance.

The report specifically mentions "mention markets" (contracts on whether a certain word will appear in a live broadcast or speech) accounting for about 3%-5% of total trading volume. While they may not generate the most revenue, they are more likely to spread on social media, serving as a tool for brand exposure and user acquisition – this aligns with Kalshi's product direction of packaging its financial matching mechanism as an "always-visible odds information stream."

Institutionalization is Not Just a Slogan: Margin, Clearing, and Liquidity Determine Its Trajectory

Kalshi emphasized the potential for institutional adoption during its research meeting. Prediction markets allow institutions to directly hedge, price, and monitor "discrete events" (geopolitical events, macroeconomic data, weather, interest rates, etc.), rather than inferring them from asset price correlations.

For institutions to enter, the barriers are more stringent. Bank of America highlighted three key areas:

- Margin Trading: Kalshi has received approval to operate as a swap dealer, enabling it to offer margin trading. Previously, full collateral was required for each trade, which was inefficient for institutions' capital.

- Clearer Regulatory and Clearing Frameworks.

- Higher Liquidity (otherwise institutions cannot use it as a hedging tool).

External signals from the institutional side are also emerging. Kalshi is collaborating with Tradeweb and FIS to expand institutional access. It also cited Goldman Sachs CEO David Solomon's statement on an earnings call: "Especially when you look at some of the platforms that are regulated by the CFTC, they look like derivative contract businesses... I certainly see opportunities for those businesses to intersect with us."

Furthermore, Kalshi is laying the groundwork for "information products": its research team evaluates market prediction accuracy. Its research on Federal Reserve predictions shows that for indicators like CPI, the average absolute error of Kalshi's median and mode predictions is significantly lower than Bloomberg consensus expectations, without exhibiting substantially worse performance. CNN and CNBC have also begun incorporating its "official odds" into their content.

Competitors in 2026 Resemble a "Platform Legion": Licenses Are the Entry Barrier, Liquidity Is the Lifeline

At the intersection of finance, crypto, and sports, competition in the prediction market space is intensifying in 2026. New or strengthened players include: Robinhood's vertical integration efforts with Susquehanna, DraftKings, Underdog, and Polymarket's projected expansion of U.S. operations; potential or related players also include FanDuel, Coinbase, and Crypto.com.

Regulatory licenses are a significant barrier, especially since obtaining an exchange license (DCM) can take years. However, recently some "dormant/underutilized" existing DCM licenses have been rapidly acquired, suggesting that supply is not entirely constrained. The real competition that will challenge Kalshi's core business lies in liquidity and fees: the report already flags "fee compression" as a risk, especially as the market expands and more strong B2C brands enter. It is uncertain whether pricing power can be maintained at current levels.

Amidst increasing competition, Kalshi still holds approximately 91% of the U.S. market share; its download share is also close to half. However, its active user base is not leading (citing Sensor Tower comparisons, Kalshi has about 5 million active users, lower than Robinhood, DraftKings, etc.). This implies its moat is derived more from early-mover liquidity and regulatory navigation rather than being a "natural super channel."

The Biggest Variable Remains Regulation: Is It Trading, or Gambling?

Regulatory risks are also evident: state governments and gambling regulators are seeking intervention, with the core debate being whether sports event contracts should be considered state-level sports betting. Current legal actions against Kalshi involve 14 states; meanwhile, several bills are progressing in Congress, focusing on insider trading, anti-manipulation, and restricting certain types of event contracts (including sports, war, etc.). Due to conflicting federal court rulings, the Supreme Court may ultimately have to intervene, and "complete clarity" might not arrive until late 2027 or early 2028.

Under the Commodity Exchange Act framework, there are three paths to restrict sports event contracts: state court restrictions on a state-by-state basis, Supreme Court rulings, or the CFTC changing its stance on sports event contracts. A more realistic risk lies in the regulatory wind: the current CFTC under this administration is relatively supportive of prediction markets, but under different administrations and CFTC leadership, markets like sports could be deemed "contrary to the public interest."

Insider trading is also a point of policy pressure. Kalshi's countermeasures include: restricting political figures and athletes from trading certain markets, establishing a monitoring advisory committee and enforcement head, and collaborating with Solidus Labs and the Wharton Forensic Analytics Lab.

Kalshi's current predicament resembles a "binary bet": on one side are the increasing financial attributes driven by trading volume, product iteration, channel independence, and institutionalization; on the other side are the potential reclassification of sports contracts, the duration of federal-state power struggles, and whether fee rates will be flattened by competition.