TSMC's stock price lags behind peers, is there a "slow bull" opportunity amid the AI chip craze?

TSMC's stock price has risen 116% over the past year. Although its performance is strong, it has underperformed Intel and Micron. Its HPC revenue proportion has exceeded 60% for the first time, with a gross margin surpassing 66%. Market valuations are restrained due to stable pricing in the foundry business, making it a non-highly elastic target. The company has raised its full-year revenue target and expects capital expenditures to reach the upper limit, facing strategic games under full capacity

According to the Zhitong Finance APP, TSMC's (TSM.US) stock price has risen approximately 116% over the past year—an impressive figure in any industry—but compared to Intel's over 500% increase and Micron's over 800% surge, the global leader in foundry services has instead become the "laggard" in this round of the AI chip feast. So, what has caused TSMC to underperform compared to the once-forgotten Intel and the "memory cycle stock" Micron? What strategic logic and risks are hidden behind TSMC's "slow bull" market?

Explosive Performance, Yet Not the "Most Elastic" Target

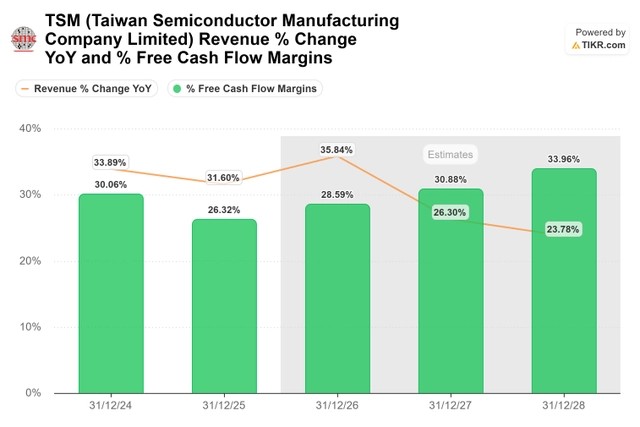

From a fundamental perspective, TSMC is flawless. In the first quarter of 2026, TSMC's consolidated revenue is approximately NT$1.13 trillion (about US$35.9 billion), a year-on-year increase of 35.1%, with a net profit after tax of approximately NT$572.5 billion, up 58.3% year-on-year. The gross margin has historically surpassed 66%, reaching 66.2%, with an operating profit margin of 58.1% and a net profit margin after tax of 50.5%. The revenue from high-performance computing (HPC) has for the first time exceeded 60%, replacing smartphones as the largest source of income.

Chairman Wei Zhejia has raised the annual revenue target to "over 30% growth," and expects capital expenditures in 2026 to approach the upper limit of the range of US$52 billion to US$56 billion.

However, the market has given TSMC an unusually restrained valuation. As of June 19, TSMC's price-to-earnings ratio is approximately 39.8 times, which, while higher than the industry average, is clearly not the "most elastic" target in this round of the AI market compared to Micron (up over 260% this year) and Intel (up over 260% this year).

The fundamental reason is that TSMC is "selling shovels," not "digging for gold." Micron has benefited from DRAM contract prices rising over 300% cumulatively over the past five quarters, while Intel has benefited from a reevaluation of market expectations regarding its 18A process and foundry business transformation. Although TSMC's foundry business is in high demand, its pricing strategy is more conservative—according to previous reports, TSMC is preparing to raise prices by about 15% again in the second half of the year, but this is considered mild compared to the "surge" in memory chip prices.

Full Capacity Yet "Handing Over Orders": Strategic Restraint or Inability?

The core contradiction TSMC currently faces is: unlimited demand, limited capacity. According to media reports, due to the demand for AI infrastructure far exceeding TSMC's advanced process capacity, Samsung Electronics is receiving an increasing number of chip foundry orders from global customers such as Google, AMD, and Tesla. TSMC has locked most of its advanced node capacity for top clients like Nvidia, Apple, AMD, Broadcom, Marvell Technology, and MediaTek, making it nearly impossible for new customers and small batch orders to squeeze in.

A "supply chain migration" is underway. Google is discussing with Samsung the possibility of producing its next-generation Axion processor and is considering transferring some TPU foundry orders from TSMC to Samsung as early as 2028; AMD is also negotiating with Samsung regarding the production of some CPUs in the future; Nvidia's Groq LPU is already being manufactured by Samsung.

Wei Zhejia admitted at the shareholders' meeting in early June that even with continuous global capacity expansion, the company will still be unable to meet the AI-driven chip demand in the coming years. When asked when the peak of capital expenditures would arrive, his answer was, "I don't know, but the next few years look good." "I currently do not see (stopped) indicators."

TSMC is not without expansion. Between 2025 and 2026, TSMC will build and renovate 18 12-inch wafer fabs globally, with new capacity primarily focused on 2nm and 3nm processes. However, the construction of chip manufacturing infrastructure is "a time-consuming and capital-intensive process," and short-term capacity bottlenecks cannot be fundamentally alleviated.

In the face of order outflows, TSMC's attitude is quite intriguing. According to previous analyses, the management does not seem eager to "plug" every inch of capacity gap through aggressive expansion or significant price increases, but rather prefers to maintain long-term stable customer relationships. This "strategic restraint" may mean a concession of market share in the short term, but in the long term, it may lead to healthier customer trust and pricing power. TSMC can still use strategic pricing methods to improve profit margins.

Geopolitics: The Sword of Damocles Hanging Over TSMC

TSMC's capacity is highly concentrated in Taiwan, a structural risk that investors cannot ignore. On the geopolitical front, TSMC recently received a positive signal: the U.S. Department of Commerce has issued an export license for TSMC's Nanjing plant for 2026, allowing it to obtain equipment subject to U.S. export controls without separate applications. This "annual license" ensures that TSMC's production lines in mainland China operate without interruption.

However, long-term risks have not been eliminated. The U.S. government has clearly stated that it will introduce broader and higher comprehensive tariffs. TSMC's capacity in Arizona, USA, is still in the ramp-up phase and cannot fully replace the capacity hub in Taiwan in the short term. Balancing the political pressure of "Made in America" with the cost efficiency of "Taiwanese capacity" will be a core strategic issue TSMC faces in the coming years.

Intel's "Return of the King": The Real Threat to TSMC?

Intel's stock price has skyrocketed from a low of about $19 in mid-2025 to over $133 now, with a cumulative increase of over 600%. The core logic behind this reversal lies in the market's reconstruction of Intel's credibility in advanced process manufacturing capabilities.

On June 16, 2026, Intel disclosed at the VLSI International Symposium that the 18A process has officially entered the risk trial production stage. The 18A process uses fully wrapped gate transistors and back power supply technology, achieving a 9% performance improvement at the same power consumption. More critically, the 18A has completed key stages such as design finalization, customer tape-out, and internal product introduction.

Meanwhile, there are rumors that Intel may reach a strategic cooperation with Apple to design and manufacture chips domestically in the U.S.; Intel is also deepening cooperation with UMC to include the 3nm advanced process in their collaboration. Analysts point out that Qualcomm and AMD are the most likely candidates to consider Samsung as a customer, while Apple and Broadcom are evaluating Intel's technology However, Intel's foundry business is still in the "burning money" stage. In the first quarter of 2026, Intel's total foundry revenue was $5.4 billion, a year-on-year increase of 16%, but revenue from external customers was only $174 million, with the rest coming from internal chips; the foundry business recorded an operating loss of $2.4 billion for the quarter. Under GAAP, Intel still reported a net loss of $3.7 billion in the first quarter.

TSMC's technological barriers remain strong. Shipments of the 3nm process accounted for 25% of its wafer sales in the first quarter, 5nm accounted for 36%, and 7nm accounted for 13%, with advanced processes (7nm and below) collectively accounting for 74% of wafer sales. The chief analyst at SemiAnalysis pointed out that AI workloads are evolving towards complex intelligent agents, and CPUs are facing "extremely severe capacity shortages." In this context, TSMC, as the world's most reliable advanced process supplier, is unlikely to have its position shaken in the short term.

Valuation and Outlook: A "Buy" Opportunity at a 23x Price-to-Earnings Ratio?

From a valuation perspective, the market's pricing of TSMC has not overdrawn the future. As of June 19, TSMC's price-to-earnings ratio was approximately 39.8 times, but considering its expected revenue growth rate of over 30% in 2026 and a stable gross margin of over 66%, TSMC's valuation is close to the industry average when measured by forward price-to-earnings ratio. Previous analyses have indicated that TSMC's valuation is still within a reasonable range of around 23 times, very close to the semiconductor industry's average price-to-earnings ratio of 21.5 times.

Wang Chih-Kai expressed "considerable confidence" in the visibility for 2030. TSMC expects its capital expenditures over the next three years to be "significantly higher" than in the past three years, with capital expenditures in the fiscal year 2028 potentially approaching $75 billion. Such a massive capital expenditure plan not only reflects management's confidence in long-term AI demand but also implies significant execution risks—if an unexpected economic recession occurs or the AI investment boom fades, high depreciation and amortization could significantly suppress profit margins.

However, TSMC's stock price has decisively broken through the key resistance level of $390 without retreating, demonstrating a strong upward momentum. Several well-known Wall Street strategists acknowledged in a joint research report released today that their previous downgrade of TSMC's rating in April "may have been premature." With the proliferation of self-developed chips by tech giants like Amazon and intense competition from Google's AI cloud and Nvidia-supported Neoclouds, the visibility of wafer foundry capacity saturation is very high in the next 3 to 4 years