From "money-burning black hole" to "monetization engine": Meta's computing power monetization opens up valuation ceiling, Deutsche Bank and Morgan Stanley sing bullish together

Deutsche Bank and Morgan Stanley have upgraded their outlook on Meta's cloud business, believing that monetizing excess computing power can enhance EPS. Both investment banks maintain a "buy" rating, with target prices of $810 and $775, respectively. Morgan Stanley views it as "the icing on the cake," pointing out that Meta faces technological and execution barriers, and recommends adopting a "new cloud" model of renting out idle computing power; Deutsche Bank is more optimistic about its strategic potential

The Zhitong Finance APP noted that Meta (META.US) is planning to enter the cloud infrastructure market and intends to open AI computing power and model access services to external developers. Following the news, Deutsche Bank and Morgan Stanley both raised their assessments of Meta's cloud business prospects, believing that "monetizing" excess computing power is a highly attractive EPS gold mine in the short term, which not only effectively reduces the risk exposure of high capital expenditures but also opens up a new imaginative space for the market.

Both investment banks maintained their "overweight" rating on Meta, but there are significant differences in their strategic positioning and performance contribution expectations for this potential new business, reflected in their target prices. Morgan Stanley and Deutsche Bank set target prices of $775 and $810, respectively, indicating an upside potential of 38% to 44% compared to the current stock price.

Morgan Stanley: New cloud is "the icing on the cake," full-stack cloud faces many challenges

Analyst Brian Nowak's team pointed out that if Meta wants to build a large-scale cloud service with a complete ecosystem, it faces extremely high technical and execution barriers.

Morgan Stanley noted that Meta's Muse series models scored poorly in TerminalBench and SWE-bench Verified benchmark tests related to coding capabilities and third-party applicability, indicating that product strength needs iteration to compete with cutting-edge models like Gemini. In addition, Meta lacks an enterprise-level sales team and a mature software service system, making it difficult to compete directly with giants like AWS, Azure, and Google Cloud in the short term. Therefore, Morgan Stanley defines Meta's potential cloud service as a "Neocloud" model, which primarily rents out idle raw computing power rather than providing a full suite of API services. This model does not require large-scale hiring of new employees or building complex software stacks, thus carrying lower execution risks.

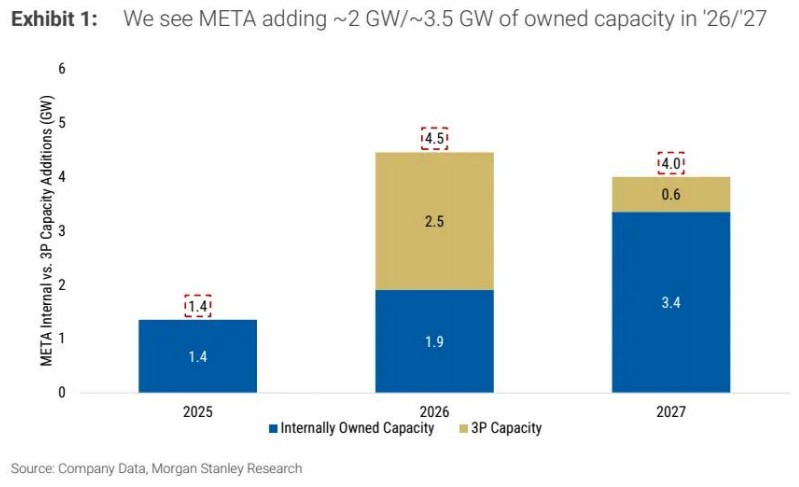

In terms of capacity estimation, Morgan Stanley expects Meta to add approximately 2GW and 3.5GW of its own IT capacity in 2026 and 2027, respectively. Based on the assumption of renting out every 250MW of computing power at $40/Watt for one year, this business is expected to increase Meta's earnings per share by about $3 in 2028, equivalent to an 8% increase.

However, Morgan Stanley emphasized that its core logic for the "overweight" rating on Meta is not based on cloud services, but rather on the improvement of operational efficiency in Meta's main business, the monetization process of Reels, and the empowerment of AI in advertising. The research report believes that computing power leasing is more of a "temporary EPS bridge," and if Meta significantly increases capital expenditures for this purpose, there is an upward risk in capital expenditures for 2027-2028.

Deutsche Bank: Monetizing computing power improves capital expenditure narrative

Compared to Morgan Stanley's prudence, the Deutsche Bank Benjamin Black team's attitude is more optimistic. Deutsche Bank believes that Meta's layout of cloud infrastructure does not mean abandoning the development of cutting-edge AI models, but rather a "tactical" monetization of capacity.

Deutsche Bank analyzes that Meta is likely to reserve the latest chip clusters for internal superintelligence training while putting older or non-core idle computing power on the market. This strategy can both preserve the technological moat and improve market concerns about AI capital expenditures through direct revenue streams. Particularly in the joint data center project that Meta is collaborating on with Blue Owl, the cash flow generated from computing power leasing helps optimize the balance sheet structure.

In financial projections, Deutsche Bank has provided more aggressive expectations. Assuming Meta has 1.2GW to 2.65GW of sellable computing power by 2027, with a utilization rate of 75% and a price of USD 1 billion to 1.5 billion per GW, this business is expected to bring in incremental revenue of USD 9 billion to 30 billion, accounting for about 3% to 10% of market expectations. This will drive Meta's GAAP earnings per share in 2027 to increase by USD 1.40 to 7.50, which is 4% to 21% higher than market consensus expectations.

Deutsche Bank specifically points out that compared to pure bare GPU leasing, model API services similar to AWS Bedrock have higher strategic value. Such businesses have recurring, usage-based billing characteristics and are closer to software attributes, which helps enhance Meta's overall valuation multiple. Of course, Deutsche Bank also acknowledges that Meta currently lacks AWS-level enterprise distribution channels, and to scale up, it still needs to improve infrastructure such as service level agreements (SLA), billing systems, and compliance support.

From "Burning Money" to "Monetization"

The consensus between the two investment banks is that Meta's AI investments are shifting from a pure cost center to a monetizable asset.

Over the past two years, the core market skepticism regarding Meta's AI capital expenditures has been "high investment, low visible returns." The indirect benefits from advertising and recommendations are difficult to quantify, while the cloud plan provides a direct third-party revenue stream—this means the market no longer needs to link all infrastructure investments solely to internal business.

The divergence between Deutsche Bank and Morgan Stanley is reflected in revenue quality and valuation anchors. Deutsche Bank places more emphasis on the "stable, high-quality revenue stream" brought by the API model, with a target price implying a premium for cloud business; Morgan Stanley, on the other hand, promotes the light asset attributes of the "new cloud," emphasizing "monetization without heavy investment."

From a valuation framework perspective, cloud revenue typically enjoys a higher price-to-earnings ratio than advertising. Even if some revenue comes from bare computing power leasing—essentially a "second-hand GPU business"—it can still shift Meta's valuation anchor from a "social advertising company" to an "AI infrastructure platform."