Taiwan Semiconductor's "old script" is hard to copy! SK hynix ADR arbitrage difficulty escalates, with historical data gaps and high volatility becoming the biggest "roadblock."

The newly issued ADR of SK hynix faces increased arbitrage difficulty due to the lack of historical data benchmarks and high volatility, leading to greater spread risks. Market participants point out that it is challenging to replicate the ADR arbitrage experience of Taiwan Semiconductor, and investors need to seek higher returns to compensate for the risks

According to Zhitong Finance APP, arbitrage traders planning to trade SK hynix (SKHY.US) newly issued American Depositary Receipts (ADRs) are revisiting their experiences from past arbitrage trades involving TSMC ADRs. However, many market participants indicate that the comparability between the two is quite limited.

TSMC ADR has decades of trading history, and investors have a clearer understanding of the premiums it typically maintains compared to local stocks. In contrast, SK hynix ADR will be listed for the first time on Friday, leaving arbitrage investors without historical benchmarks to determine what premium is considered normal, making it more challenging to assess whether the current price difference is attractive or has already widened excessively.

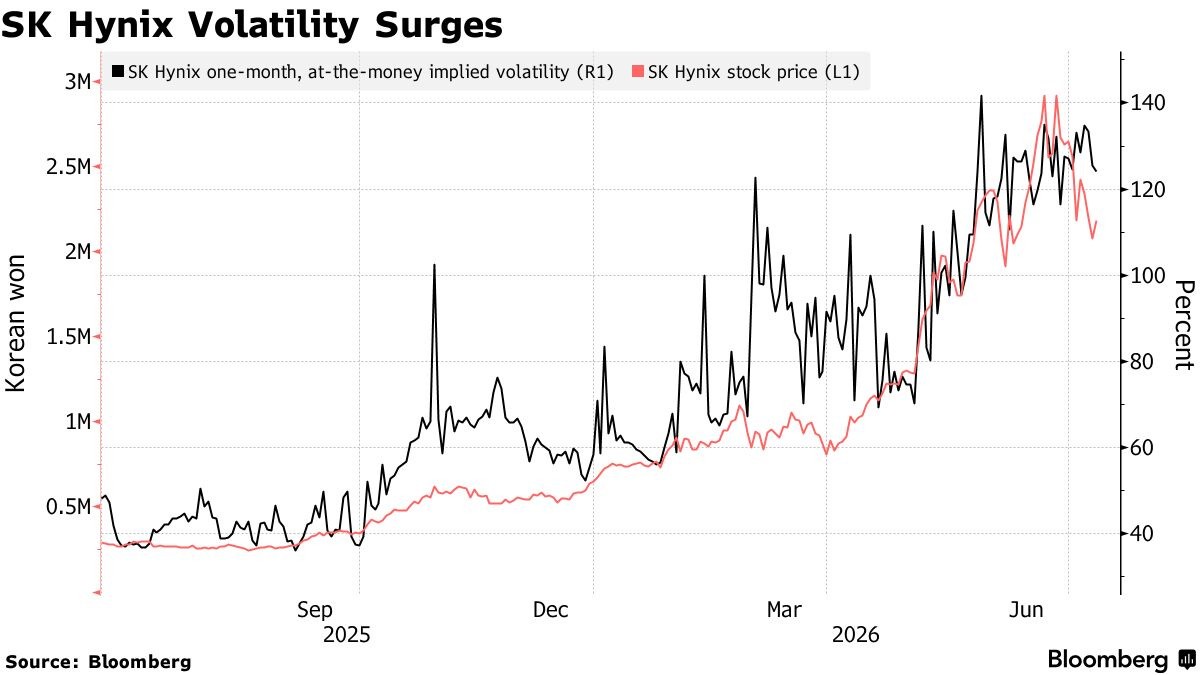

The challenges stem not only from the lack of historical price data. In recent years, SK hynix has become one of the most volatile large-cap stocks in Asia. As investors continue to flock to AI-related memory chip stocks and leveraged products linked to this stock, its price often experiences daily fluctuations that far exceed the market average.

This extreme volatility further increases the so-called "spread risk," meaning that the price movements between the ADR and the stocks listed in Seoul, South Korea, may deviate significantly from the direction that arbitrage traders originally bet on. Alex Au, Managing Director of Alphalex Capital Management HK Ltd. and a veteran in TSMC ADR arbitrage trading, stated, "Due to the higher volatility of SK hynix, the spread risk is also significantly greater. Therefore, investors looking to gain ADR premium returns through arbitrage will inevitably demand a higher rate of return."

Additionally, another uncertainty lies in the extent to which SK hynix's common stock listed in South Korea can be converted into American Depositary Receipts (ADRs). According to a regulatory filing submitted by SK hynix on July 6, ADR holders can cancel their ADRs and exchange them for the corresponding number of common shares listed in Seoul, South Korea. However, investors may not be able to convert these common shares back into ADRs in the future, as this conversion process may require approval from relevant authorities, including South Korean regulators.

In contrast, the market has years of trading experience with TSMC's partially convertible ADR mechanism. Although the premium of TSMC ADR compared to local Taiwanese stocks has temporarily widened due to the AI boom, investors can still rely on historical patterns to determine when the premium has become excessive and will eventually revert to normal levels (mean reversion).

According to compiled data, over the past month, TSMC ADR has averaged a premium of about 16% compared to local Taiwanese stocks. This spread has long exhibited mean-reverting characteristics, making it one of the most popular relative value arbitrage trades globally until the current AI investment frenzy disrupted this pattern.

Currently, several institutional investors have vastly different predictions regarding the potential premium for SK hynix ADR in the early stages of its listing, ranging from about 5% to over 30%, highlighting the significant uncertainty in the market before its official listing.

Currently, several institutional investors have vastly different predictions regarding the potential premium for SK hynix ADR in the early stages of its listing, ranging from about 5% to over 30%, highlighting the significant uncertainty in the market before its official listing.

According to a report sent to institutional clients, Morgan Stanley's sales and trading department predicted on Wednesday that the initial premium for SK hynix ADR would be around 5% to 10%; if this ADR is included in major U.S. stock indices or exchange-traded funds (ETFs) in the future, there is room for this premium to expand further.

Independent special events analyst and Smartkarma contributor Travis Lundy stated, "No one can accurately determine what premium level it should maintain daily until it has traded for a while and formed a mature market." He added, "Historical experience shows that such ADR premiums can indeed rise very high, but they typically do not remain at extremely high levels for long."