U.S. Stock Outlook | The three major index futures are mixed as CPI, major bank earnings, and Waller's congressional debut are set to unfold. IBM's preliminary earnings fell short of expectations, dragging down software stocks

On July 14th, before the US stock market opened, the three major stock index futures were mixed, with Dow futures down 0.57%, S&P 500 down 0.17%, and Nasdaq up 0.42%. Major European stock indices generally fell, while oil prices rose. The market is focused on key events such as CPI data, major bank earnings reports, and the testimony of the Federal Reserve Chairman before Congress. Although implied volatility expectations are moderate, insufficient liquidity may amplify risks

Pre-Market Market Trends

- As of July 14 (Tuesday), U.S. stock index futures showed mixed results before the market opened. As of the time of publication, Dow futures were down 0.57%, S&P 500 futures were down 0.17%, and Nasdaq futures were up 0.42%.

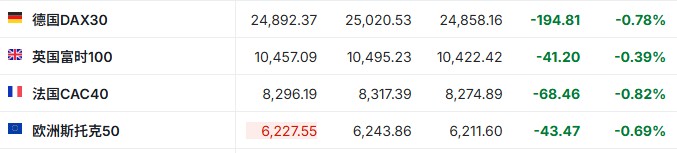

- As of the time of publication, the German DAX index was down 0.78%, the UK FTSE 100 index was down 0.39%, the French CAC 40 index was down 0.82%, and the Euro Stoxx 50 index was down 0.69%.

- As of the time of publication, WTI crude oil was up 2.37%, priced at $79.99 per barrel. Brent crude oil was up 3.84%, priced at $86.50 per barrel.

Market News

"Super Tuesday" is coming! CPI, major bank earnings, and Waller's congressional debut create a three-pronged attack, as U.S. stocks at high levels face a critical pricing window. On Tuesday, the U.S. stock market will see a series of significant events, with various key data and agendas coming in quick succession. However, stock traders appear indifferent, and this nonchalant attitude places the market in a subtly fragile state—after all, U.S. stocks are hovering near historical highs. According to data compiled by Citigroup, the implied volatility of the S&P 500 index on Tuesday is about ±0.7%. For such a significant trading day, this expected volatility is relatively mild—on that day, not only will the crucial Consumer Price Index (CPI) be released, but the first batch of major bank earnings for the earnings season will also be announced, along with the congressional testimony of the Federal Reserve Chair, not to mention the geopolitical risks arising from the escalating situation in the Middle East. It is noteworthy that this implied volatility level is also in line with the average volatility observed on the past 12 CPI release days. According to Piper Sandler, this calm expectation is likely to last at least until Friday: based on the pricing of straddle options on the S&P 500 index, the market expects a volatility range of about ±1.1% this week, the smallest weekly expected volatility since last December. This phenomenon is likely due to the traditional "summer lull" effect—major trading desks are understaffed, leading to thin market trading. However, the risk of insufficient liquidity is that if developments do not meet expectations, market volatility could be sharply amplified.

New York State will temporarily ban the construction of new large data centers. The office of New York Governor Kathy Hochul announced that she plans to sign an executive order on Tuesday to halt the construction of large data centers, with the ban lasting up to one year. The ban takes effect immediately and applies to data centers with a power consumption of 50 megawatts or more This suspension order will buy the state time to formulate data center-related regulations that are both environmentally friendly and ensure the operation of the power grid. This move makes New York the latest state to address the infrastructure challenges posed by the AI boom. No other state has implemented similar suspension measures before. However, dozens of cities and counties across the United States have issued temporary bans on data center construction, and many states have proposed similar ban ideas. As data centers continue to be built across the country, more and more communities are expressing opposition, fueling the development of the anti-AI movement. Opponents argue that these data centers, which support artificial intelligence and computing systems, could overwhelm local power supplies and drive up utility costs for residents. Some voters have even attempted to recall politicians who support data center development.

Masayoshi Son of SoftBank: The AI boom will require $5 trillion in annual investment. Masayoshi Son, founder of SoftBank Group, stated that by 2040, global artificial intelligence infrastructure will require an annual investment of $5 trillion to support the expansion of data centers, power supplies, and humanoid robots, thereby driving a shift from a "human-centered" work model to a new model. He pointed out that as artificial intelligence develops into "artificial superintelligence" (ASI), the revenue generated will justify these massive expenditures. "Artificial intelligence will fundamentally change our lives—and this change will bring profits," said Masayoshi Son.

Four South Korean government departments will hold a meeting on Thursday to discuss response plans for the impact of single-stock leveraged ETFs on the stock market. Leveraged products tracking South Korea's core chip stocks have recently plummeted, significantly impacting the South Korean stock market and financial markets. Data compiled by the industry shows that the prices of several leveraged exchange-traded funds (ETFs) tracking Samsung Electronics (SSNLF.US) and SK Hynix (SKHY.US), which were listed in late May, have nearly halved. According to reports, a high-level coordination mechanism from four major economic departments of the South Korean government will hold a meeting on Thursday to discuss response plans for the impact of single-stock leveraged ETFs on the stock market. This is the first time this issue has officially entered the mechanism for discussion. The mechanism is the highest-level economic coordination platform jointly participated by the Ministry of Economy and Finance, the Financial Services Commission, the Bank of Korea, and the Financial Supervisory Service.

Oil prices nearing $90 reignite inflation concerns, and expectations for interest rate hikes by the Bank of England and the European Central Bank resurface. As soaring oil prices reignite inflation concerns, traders have increased their bets on the Bank of England and the European Central Bank accelerating interest rate hikes. For the first time in a month, traders have fully priced in expectations for a 25 basis point rate hike by the Bank of England before September, followed by another hike before the end of the year. They also expect the European Central Bank to raise rates by 25 basis points in September, with another hike by the end of the year almost a certainty. This shift comes as escalating tensions between the U.S. and Iran are pushing Brent crude prices close to $90 per barrel. Earlier this month, expectations for rate hikes by the Bank of England and the European Central Bank in swap trading were less than 25 basis points until next year. However, U.S. President Trump has renewed the blockade of Iranian vessels passing through the Strait of Hormuz and has imposed payment requirements on all other goods, completely disrupting market calm

Individual Stock News

Bank of America expects SK Hynix's actual new capacity by 2028 to be only one-sixth of the original plan. According to the latest analysis from Bank of America, the actual new storage chip capacity that SK Hynix can add by 2028 may only be one-sixth of the original plan. This assessment not only undermines the South Korean government's capacity expansion blueprint but also provides key evidence for the ongoing collective lawsuit regarding DRAM price manipulation. Due to factors such as the closure of old factories, technological upgrades, and process miniaturization, South Korea's actual annual increase in operational storage wafer capacity is less than 10%, which means that the capacity increment by 2030 will be far below the "doubling of capacity by 2030" target set by South Korean President Yoon Suk-yeol. This assessment directly impacts the supply expectations in the DRAM market.

Samsung denies considering a U.S. listing: No assessment of issuing ADRs. Samsung Electronics denied a media report on Tuesday that claimed the company is in the early stages of exploring the possibility of issuing American Depositary Receipts (ADRs) in the U.S. A Samsung spokesperson stated in a statement, "Samsung has not assessed the possibility of issuing ADRs." Previously, informed sources indicated that Samsung had preliminary discussions with banks but had not yet decided whether to proceed with the ADR issuance plan. Additionally, the report stated that these discussions may ultimately not lead to a listing. Samsung had previously evaluated the possibility of issuing ADRs but ultimately decided to abandon the idea. However, the successful listing of competitor SK Hynix in the U.S. has given Samsung new motivation to reconsider this idea.

IBM (IBM.US) preliminary Q2 revenue falls short of expectations, U.S. software stocks decline collectively. IBM's preliminary revenue data for the second quarter was $17.2 billion, a 1% increase, below the estimated $17.86 billion; software revenue grew by 5%, while infrastructure revenue fell by 7%. Diluted earnings per share were $2.27, down 2% year-on-year; operating (non-GAAP) earnings were $2.93, up 5% year-on-year. IBM stated that it expects infrastructure revenue to decline in single digits starting from this quarter. IBM noted that in the last few weeks of June, they observed customers shifting quarterly capital expenditures towards server, storage, and memory purchases to secure supplies of tight infrastructure before anticipated price increases. As a result of this news, U.S. software stocks fell sharply in pre-market trading, with IBM plummeting nearly 23%, Accenture (ACN.US) dropping over 7%, ServiceNOW (NOW.US) falling 8%, and Microsoft (MSFT.US) declining over 3%.

Market research firm Counterpoint: Q2 global smartphone sales fell 11% year-on-year, Samsung and Apple (AAPL.US) still lead the market. Market research firm Counterpoint Research stated on Monday that global smartphone sales in the second quarter of this year fell 11% year-on-year, while Apple and Samsung Electronics continued to lead the market. Counterpoint noted that from March to June this year, global smartphone shipments declined, reaching the lowest level for a second quarter since 2013, due to a worsening shortage of storage chips. Despite the overall market decline, Samsung regained the top position in the global smartphone market, capturing 24% market share In comparison, Apple's smartphone shipments in the second quarter increased by 3% year-on-year, capturing 20% of the global market share by the end of the second quarter.

CleanSpark (CLSK.US) secures a 20-year leasing agreement for data centers, surging over 23% in pre-market trading. Data center developer CleanSpark announced that it has signed a 20-year infrastructure leasing agreement with a leading global technology company with high investment-grade ratings for its facility located in Sandersville, Georgia, which includes two options for 5-year extensions. The initial lease term is expected to generate approximately $6.6 billion in contract revenue.

Stock market business revenue soars, with JP Morgan (JPM.US) profits exceeding expectations at the highest level in five years. JP Morgan's second-quarter profit performance was impressive, with both investment banking fees and activity accelerating, driving record results across all business segments. Q2 net profit increased by 41.2% year-on-year to $21.16 billion, with earnings per share rising from $5.24 to $7.70, significantly surpassing the average analyst expectation of $5.59. This earnings per share beat is the largest since Q1 2021. Total revenue grew by 27.7% to $57.35 billion, far exceeding the analyst expectation of $51.09 billion. By business segment, corporate and investment banking revenue grew by 27.2% to $24.85 billion, with market and securities business revenue increasing by 33.1% to $13.69 billion, and stock market business revenue soaring by 86% to $6 billion. Investment banking revenue grew by 45% to $3.9 billion. Consumer and community banking revenue increased by 7.6% to $20.27 billion; asset and wealth management revenue grew by 18.9% to $6.85 billion.

Goldman Sachs (GS.US) Q2 net profit skyrockets by 80%, significantly exceeding expectations, with investment banking revenue hitting a record high. Goldman Sachs' net profit in the second quarter surged nearly 80% year-on-year to $6.6 billion, marking the bank's best quarterly performance in five years. The growth in investment banking revenue, combined with record highs in stock trading, jointly boosted the company's net profit. Analysts had previously expected net profit to be only $4.7 billion. Investment banking revenue increased by over 50% year-on-year to $3.4 billion, outperforming institutional expectations; the standout segment in this earnings report remained the stock trading business. Goldman Sachs' stock trading revenue reached $7.4 billion, soaring 72% year-on-year, exceeding analyst estimates by $2.4 billion, setting a new record for quarterly stock trading revenue, surpassing the previous high set in the last quarter.

Wealth management and investment banking drive Wells Fargo (WFC.US) to exceed Q2 performance expectations. Wells Fargo's second-quarter earnings report showed that the bank's performance exceeded Wall Street expectations, thanks to increased fee income from wealth management and investment banking. Non-interest income for the quarter grew by 13% to $10.3 billion, higher than the analyst expectation of $9.44 billion. The bank stated in a statement on Tuesday that the performance included a net gain of $728 million from venture capital. As an important indicator of the profitability of the bank's lending business, net interest income was $12.3 billion, which was basically in line with market expectations As of the end of June, the bank's net profit grew by 17% to $6.4 billion, with earnings per share of $2. Analysts had previously expected adjusted earnings per share of $1.71. Revenue for the quarter increased by 9% to $22.6 billion.

Bank of America (BAC.US) reported second-quarter revenue of $31.6 billion, a year-on-year increase of 15%. Bank of America's total revenue for the second quarter was $31.6 billion, up 15% year-on-year. Diluted earnings per share were $1.21 (up from $0.90 in the previous period), a year-on-year increase of 34%. Net profit was $9.1 billion, a year-on-year increase of 27%. Consumer banking revenue was $11.336 billion, up 5% year-on-year; global markets revenue was $8.022 billion, up 34% year-on-year; global wealth and investment management revenue was $6.871 billion, up 16% year-on-year; global banking revenue was $6.236 billion, up 10% year-on-year.

Citigroup (C.US) reported a 14% increase in second-quarter revenue to $24.8 billion, exceeding market expectations. Citigroup announced its second-quarter financial results for fiscal year 2026 on Tuesday, showing total revenue of $24.8 billion, a year-on-year increase of 14%, outperforming analysts' previous expectations. Meanwhile, Citigroup's net profit for the quarter was $5.8 billion, a significant increase of 45% compared to the same period in 2025. Diluted earnings per share (EPS) soared by 60.7% year-on-year to $3.15.

Important Economic Data and Event Forecasts

Beijing time 20:15: U.S. ADP employment data for the week ending June 27.

Beijing time 20:30: U.S. June CPI.

Beijing time 21:00: European Central Bank President Lagarde and U.S. Treasury Secretary Yellen hold talks.

Beijing time 22:00: Federal Reserve Chairman Waller attends the House Financial Services Committee "Federal Reserve Semiannual Monetary Policy Report" hearing.

Beijing time the next day 00:40: Federal Reserve Governor Barr speaks on artificial intelligence at the Federal Reserve's annual Financial Inclusion Conference.

Beijing time the next day 01:00: 2027 FOMC voting member and Chicago Fed President Goolsbee participates in a fireside chat.

Beijing time the next day 01:30: Federal Reserve Governor Lisa Cook speaks at the Federal Reserve's annual Financial Inclusion Conference.

Beijing time the next day 02:55: Federal Reserve Governor Bowman speaks at the Federal Reserve's annual Financial Inclusion Conference.

Beijing time the next day 04:30: U.S. API crude oil inventory change for the week ending July 10.

Earnings Forecast

Wednesday pre-market: ASML (ASML.US), Johnson & Johnson (JNJ.US), Morgan Stanley (MS.US), BlackRock (BLK.US)