ASML expands production, TSMC increases investment, Anthropic's profit leap: The argument of "excess computing power" is countered, is the AI bull market moving towards the era of reasoning compounding?

ASML raised its performance guidance for 2027, TSMC and Anthropic have strong earnings expectations, and Wall Street institutions believe that the AI computing power industry chain is shifting from a training capital expenditure cycle to a stage of expanding inference demand. These positive signals counter the "excess computing power" rhetoric, indicating that data centers are bidding farewell to the pure cash-burning period and welcoming a cash flow revaluation, providing support for the AI bull market

According to the latest research report released by the well-known Wall Street investment firm Wedbush Securities, the lithography giant ASML (ASML.US) has raised its 2027 performance guidance beyond expectations, which is very favorable for the bullish outlook on AI computing infrastructure themes associated with advanced process logic chips such as CPU/GPU and dynamic random-access memory (DRAM) chips. The latest views from Wall Street institutions like Wedbush, along with the strong performance and optimistic outlook of ASML and TSMC, undoubtedly provide a strong boost for the AI computing theme, which has been severely impacted by overcrowded and highly leveraged long positions leading to extreme sell-offs.

From Wedbush's optimistic bullish stance on the AI computing theme to the explosive performance and strong outlook recently announced by ASML and TSMC, the two most important upstream capacity and supply forces in the AI computing industry chain, and the latest analysis from research firm SemiAnalysis showing that Anthropic is transitioning from long-term losses to a phase of explosive profit growth, an important signal is being released to the global stock market: the AI computing industry chain has gradually shifted from a "super cycle of AI capital expenditure for training AI large models" to a new phase of "exponential expansion of AI inference computing demand driven by large-scale applications of intelligent agents." These latest signals effectively counter the pessimistic view of "computing power surplus" that has recently led to a sharp decline in the AI computing theme, especially in the AI semiconductor sector.

Wedbush's core judgment is that ASML's upward revision of the 2027 outlook and consideration of continued increases in EUV capacity for 2028 aligns perfectly with the nearly endless demand supported by advanced process logic chips (i.e., logic chips such as CPU/GPU/TPU below 5nm process) and high-end DRAM for the construction of AI data centers; the increase in ASML's lithography equipment shipments in 2027 is expected to translate into initial wafer manufacturing output by the end of 2027 to early 2028, especially for high-end DRAM/HBM storage chip capacity. However, the continuous growth of AI-related capital expenditures from chip manufacturing giants like TSMC and global tech giants like Microsoft and Meta still leaves uncertainty about when supply will truly catch up with demand.

Matt Bryson, a senior analyst at Wedbush Securities, wrote in a recent report to clients: "We believe that ASML management's unexpected upward revision of the 2027 outlook, along with the potential significant increase in EUV lithography equipment output for 2028, is nearly consistent with the strong demand growth we are seeing for advanced process logic chips and high-end DRAM aimed at supporting the booming global AI computing infrastructure construction process."

"The timeline for increased shipments also aligns very well with our baseline judgment that the increase in AI computing-related capital expenditures in 2027 will ultimately drive an increase in the output of advanced process logic chips and DRAM by the end of 2027 to early 2028, especially for HBM/DRAM storage chips; however, given that capital expenditures are still on the rise, we remain uncertain about when supply will ultimately catch up with the increasingly expanding demand curve "The analyst team led by Bryson at Wedbush stated.

In addition to the 2027 performance guidance, ASML's management currently expects total net sales for the full year 2026 (i.e., total revenue expectations) to be between €43 billion and €45 billion, significantly higher than the previous forecast range of €36 billion to €40 billion, and also above the average expectation of €39.3 billion from Wall Street analysts.

From EUV to 5GW Super Cluster: Fourfold Industry Chain Signals Break Through "AI Computing Power Surplus Theory"

According to the financial report, ASML's revenue in the second quarter reached €9.326 billion, exceeding the market expectation of €8.8 billion; net profit was €2.918 billion, also surpassing the expected €2.62 billion, with a gross margin of 54%. More importantly, the company significantly raised its 2026 revenue guidance from €36 billion—€40 billion to €43 billion—€45 billion, and increased its gross margin guidance from 51%—53% to 54%—56%, expecting third-quarter revenue to further rise to €11 billion—€12 billion. ASML's management stated that orders in the first half of the year were "extremely strong," with customers accelerating the capacity construction of advanced process logic chips and memory chips. Therefore, they plan to increase the capacity of low numerical aperture extreme ultraviolet lithography machines and immersion deep ultraviolet lithography machines by about 30% by 2027, and are studying an additional increase of about 30% in 2028. This indicates that major customers like TSMC and Intel have committed to years of lithography equipment rather than just verbal forecasts, voting for strong demand for AI computing power in 2027—2028.

ASML's rare large-scale capacity expansion means that advanced logic chip manufacturers like TSMC and Intel are preparing for a larger wafer capacity to meet the demand for customized AI ASIC accelerators such as data center server-level CPUs, GPUs, and TPUs; meanwhile, the latest performance from Samsung and the severe shortage situation released by SK Hynix's CEO on the first day of its U.S. ADR listing further verifies that the demand for AI server systems remains incredibly strong from another core link in the AI computing power industry chain.

More critically, ASML's management plans to increase the annual capacity of about 65 low numerical aperture EUV machines by 30% by 2027 and is studying a further increase of 30% in 2028, with similar expansion paths for DUV immersion lithography machines. This is not a short-term inventory replenishment but a commitment by global wafer fabs to lock in advanced logic, HBM/DRAM, and advanced packaging upstream capabilities with multi-year equipment commitments.

This week's AI industry news indicates that Meta, the parent company of Facebook, has expanded its investment in the Hyperion data center campus in Louisiana from the initially announced $10 billion to over $50 billion, with a super cluster exceeding 5GW of computing power, along with 27,500 Rubin igniting the "Japanese Robot National Team." Additionally, Jensen Huang, CEO of NVIDIA, visited Japan to collaborate with established industrial giants such as Fanuc, Yaskawa Electric, Kawasaki Heavy Industries, and Fujitsu to promote physical AI collaboration, incorporating SoftBank, NEC, Hitachi, Sony, and Preferred Networks into the Cosmos ecosystem. Coupled with TSMC, the exclusive manufacturer of NVIDIA's AI chips, which has recently announced strong and exceeding expectations performance and an increasingly optimistic outlook for AI computing power demand, it is sufficient to prove that the global AI computing power investment cycle is far from over The expansion of computing power is evolving from a single arms race dominated by American hyperscale cloud vendors to a multi-center resonance of "cloud AI, sovereign AI, and physical AI."

TSMC's performance and outlook validate that this demand is not only present in equipment orders: in the second quarter, dollar revenue reached $40.2 billion, a year-on-year increase of 33.7%; net profit reached NT$706.56 billion, a year-on-year increase of 77.4%, significantly exceeding the market expectation of NT$632.6 billion; high-performance computing business accounted for 66% of revenue, and advanced processes of 7nm and below accounted for 77% of wafer business revenue.

More significantly, TSMC's revenue guidance for the third quarter has been raised to $44.6 billion - $45.8 billion. The company also significantly raised its 2026 capital expenditure from $52 billion - $56 billion to $60 billion - $64 billion, increased its full-year dollar revenue growth guidance to slightly above 40%, and added $10 billion in investments in the U.S., bringing the total commitment in the U.S. to approximately $265 billion. As the final capacity planner for core AI chip customers like NVIDIA and the manufacturer fulfilling AI computing power demands, TSMC indicates through profits, utilization rates, and capital expenditures that the visibility of AI computing infrastructure demand around advanced process logic chips, cutting-edge 2nm processes, and advanced packaging is still rising, rather than the global AI computing demand being in a slump.

ASML and TSMC do not mechanically accept customer forecasts but approve capacity expansions only after reviewing data center construction and end-user demand. Therefore, this latest guidance strongly counters the assertion that "systemic computing power surplus has already emerged." The demand side is also continuing to expand: the Japanese government-supported Noetra project plans to procure 27,500 NVIDIA Rubin chips to build physical AI infrastructure, with the project scheduled to start in April 2027 and go live in June 2028; Meta is expanding its Louisiana Hyperion site from an initially announced $10 billion project in 2024 to a supercluster with over $50 billion and 5 gigawatts of computing power. These four industrial chain signals undoubtedly break through the "AI computing surplus theory."

Anthropic is expected to achieve a significant leap in profitability trajectory, as the AI computing bull market enters the "Token Compound Interest Era"

OpenAI and its long-standing strongest competitor in the AI application field, Anthropic PBC, have been competing to develop more advanced artificial intelligence agents (i.e., AI agent products) to streamline workflows across a broader range of fields. Previously, both companies achieved significant success with AI development tools capable of automatically completing code writing and the entire debugging and deployment process. Earlier this year, Anthropic launched a similar product called Claude Cowork, aimed at attracting a broader user base to join the unprecedented wave of AI agents.

OpenAI and Anthropic have both secretly submitted IPO applications. Institutions previously reported that Anthropic is expected to potentially land on the U.S. stock market as early as this fall. OpenAI is also considering going public next year The latest analysis from research firm SemiAnalysis reveals that Anthropic is reshaping the AI commercialization landscape with profitability and growth rates far exceeding its competitors. With a high-margin business model centered around APIs, Anthropic has become a leader in the B2B AI market. A deep report released by SemiAnalysis indicates that the firm expects Anthropic to achieve $1 billion in GAAP EBITDA by the third quarter of 2026, corresponding to a profit margin of about 6%. Meanwhile, its annual recurring revenue (ARR) has skyrocketed from $9 billion at the end of 2025 to over $60 billion currently. The firm predicts that if Anthropic maintains a net new ARR (NNARR) pace of about $15 billion per month, its ARR could reach $300 billion by the end of 2027, corresponding to a $6 trillion enterprise value, making it the highest-valued company in the world.

The turning point for Anthropic's performance stems from the explosive popularity of Claude Code. Statistics compiled exclusively by SemiAnalysis show that Claude Code currently accounts for over 7% of all code submissions on GitHub, directly driving the company's ARR from a monthly addition of $3 billion in January to a staggering $11 billion in March. Additionally, SemiAnalysis's calculations indicate that Anthropic's current overall gross margin has risen to the mid-60% range, compared to a negative 94% in 2024; the gross margin for the API business exceeds 80%.

The so-called grand investment narrative of global capital "seeking silicon-based inflation and weakening carbon-based" this year essentially reflects a shift of capital from traditional manufacturing, automotive, consumer, real estate, and energy sectors—relying on population, resources, and linear economic growth—towards high-end manufacturing chains related to AI computing infrastructure around silicon chips. Therefore, the arrival of GPT-5.6 alongside ChatGPT Work, combined with Anthropic's commercialization data, reinforces a core investment judgment: the unprecedented demand cycle for AI computing infrastructure has not ended but is transitioning from a phase driven by AI large model training to one driven by AI inference application. The true supercycle of AI computing infrastructure may arise from global enterprises deploying AI agents as a new generation of digital employees on a large scale, which also means that the current pullback in the AI semiconductor sector is a healthy adjustment, not a bear market crash driven by "overcapacity."

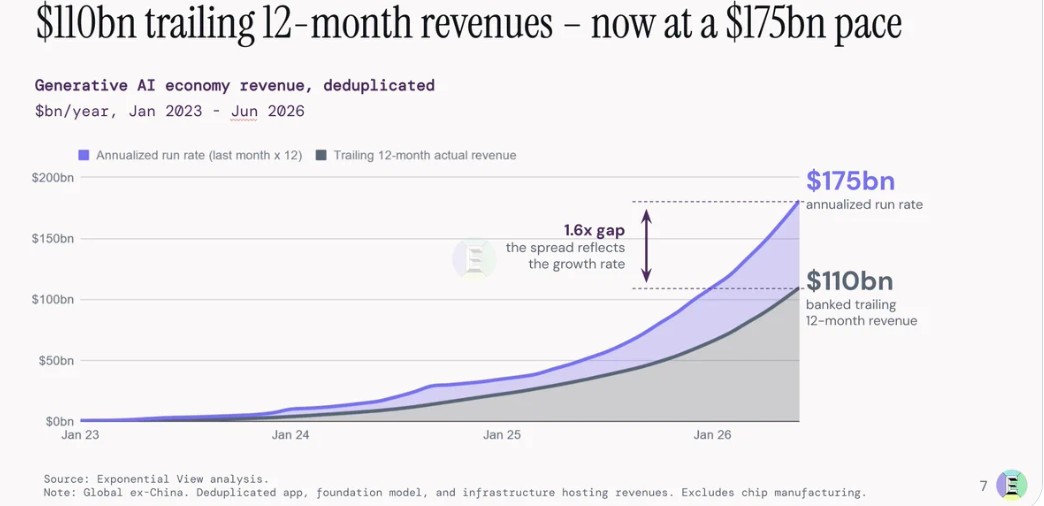

Renowned research firm Exponential View's latest study shows that the AI industry is upgrading from a capital expenditure cycle primarily reliant on cutting-edge model training to a dual-cycle of "training continuous expansion and inference becoming the incremental main engine."

Exponential View's latest calculations, conducted from the bottom up and excluding redundant supply chain path calculations, indicate that the terminal revenue scale related to generative AI has reached $110 billion over the past 12 months, with a recent monthly annualized revenue run rate exceeding $175 billion, growing at about three times the rate of the internet and mobile waves during the same period; more critically, the AI computing infrastructure-related revenue attributable to hyperscale cloud vendors has roughly covered the depreciation costs of newly added computing assets

The exclusive model from Exponential View also shows that for every 10% decrease in Token prices, usage increases by 12% to 18%, which means that a decrease in unit reasoning costs does not necessarily lead to a reduction in total revenue; instead, it may expand overall computing expenditures through demand elasticity. In other words, the construction process led by major AI tech giants like Microsoft, Meta, and Google is transitioning from an expectation of "build first, find revenue later" to an economic closed loop validated by actual Token consumption and enterprise payments