How to Interpret the Bank of Korea's Recent Rate Hike?

On July 16, 2026, the Bank of Korea unanimously raised interest rates by 25 basis points to 2.75%, marking its first rate hike in three and a half years. This move aims to address an overheated economy, high inflation, rising housing prices, and pressure from the depreciation of the South Korean won. Analysts believe that further rate hikes are likely, as real interest rates remain negative and there is a need to hedge against interest rate differentials, with the October meeting potentially serving as the next window for action

Summary

First, the Bank of Korea held its Monetary Policy Board meeting on July 16, 2026, and unanimously raised the base rate by 25 basis points to 2.75%. This marks the first rate hike since January 2023, after an interval of approximately three and a half years. Both the magnitude and timing of the hike were within market expectations.

Second, why did South Korea raise rates? We understand there are primarily four background factors: First, South Korea has benefited from the memory chip cycle this year, resulting in relatively high economic growth. On July 14, the South Korean government raised its 2026 economic growth forecast from 2% to 3%, significantly higher than the potential growth rate of approximately 1.8%. From the central bank's perspective, a rate hike can prevent an Overheated Economy. Second, inflation growth is relatively high; in June, South Korea's consumer price index (CPI) rose by 3.2% year-on-year, the fastest pace since late 2023, and remained above the 2% target for the fourth consecutive month. Third, upward pressure on South Korean housing prices has intensified, particularly with rapid short-term gains in the Seoul metropolitan area. Over the past year, residential prices in Seoul have cumulatively risen by approximately 13.1%. Furthermore, the publicly announced prices for Seoul apartments in 2026 rose by 18.67% year-on-year, the fastest increase in five years, with the average increase in the "Gangnam Three Districts" reaching 24.7%. The rise in housing prices and household debt is also a crucial component of the "financial stability" considerations in this rate hike. Fourth, the South Korean won has been weak this year; its depreciation increases import costs and exacerbates inflationary pressure, while a rate hike can provide support for the exchange rate.

Third, will there be further rate hikes? We believe the probability is relatively high. Firstly, looking domestically, even after this hike, the base rate of 2.75% still corresponds to a negative real interest rate. Monetary policy has not yet entered a restrictive zone and is insufficient to curb inflation and the housing bubble. To demonstrate determination to stabilize the real estate market, South Korean President Lee Jae-myung listed his primary residence for sale at below-market prices on July 15. Secondly, regarding internal and external balance, the interest rate differential between South Korea and the US remains significant. Against the backdrop of sustained high US interest rates and uncertainty in global capital flows, the Bank of Korea may signal a "rate hike cycle" to hedge against pressure from the interest rate differential. Thirdly, the Bank of Korea's statement explicitly pointed out that "it is necessary to continue maintaining a policy stance consistent with further rate hikes" and that "the Committee will determine the timing and pace of further base rate hikes while assessing the degree of inflationary pressure, trends in domestic economic improvement, and financial stability." Following this hike, the meeting on October 22 will be the next window for further rate increases.

Fourth, the South Korean stock market has undergone a significant correction over the past month or so. The KOSPI Index fell by 25% on July 16 compared to June 22. We understand that, firstly, obvious vulnerabilities and leverage risks had accumulated previously. The high point of the KOSPI Index on June 22 was 114.0% higher than the closing price on the last trading day of 2025; as of June 24, the total number of domestic stock trading accounts in South Korea reached 108.7 million (an increase of over 10 million from 98.28 million at the end of 2025), while the total population of South Korea is only about 51.7 million. The balance of credit financing once hit a historical peak of 38.63 trillion South Korean won on June 24—highlighting the market's distinct "leveraged" characteristics. Secondly, fundamental triggers: Market skepticism arose regarding the sustainability of memory chip price increases, with expectations that price gains would slow in the second half of the year. Thirdly, the tightening of monetary policy by the Bank of Korea further triggered expectations of liquidity contraction. Fourthly, external disturbances: The US launch of Section 337 investigations against companies such as Samsung Electronics also had some impact. Simply put, this is a typical case superimposing "accumulated market leverage risk + marginal changes in fundamentals + liquidity tightening boost + external factor disturbances."

Fifth, as there have been no explicit changes in the economic fundamentals or the fundamentals of the technology industry, the South Korean stock market should find stabilization momentum after adjusting to a relatively reasonable level. However, it is worth noting that a fundamental closed loop of the global technology industry cycle this year is US capital expenditure and exports from Asia (China, South Korea). After this adjustment in the South Korean market, unilateral expectations for the global technology supply chain are expected to weaken. From a fundamental perspective, subsequent observations should focus on two areas: first, South Korean semiconductor exports (ten-day data) and TrendForce's quarterly DRAM/NAND contract prices; second, closely monitoring the pace of South Korea's current rate hike cycle.

Main Text

The Bank of Korea held its Monetary Policy Board meeting on July 16, 2026, and unanimously raised the base rate by 25 basis points to 2.75%. This marks the first rate hike since January 2023, after an interval of approximately three and a half years. Both the magnitude and timing of the hike were within market expectations.

Looking back at this cycle, the Bank of Korea raised rates multiple times starting from August 2021, pushing the base rate to a cyclical high of 3.50% by January 2023 and maintaining it for about a year. In the second half of 2024, it shifted into a rate-cutting channel, gradually lowering it to 2.50%, where it remained unchanged for about 14 consecutive months until this restart of rate hikes. All seven committee members voted in favor of the rate hike this time, with new Governor Shin Hyun-song and Deputy Governor Yoo Sang-dae, among others, in attendance without dissent—contrasting with the hawkish divergence seen in the May meeting.

Why did South Korea raise rates? We understand there are primarily four background factors: First, South Korea has benefited from the memory chip cycle this year, resulting in relatively high economic growth. On July 14, the South Korean government raised its 2026 economic growth forecast from 2% to 3%, significantly higher than the potential growth rate of approximately 1.8%. From the central bank's perspective, a rate hike can prevent an Overheated Economy; second, inflation growth is relatively high; in June, South Korea's consumer price index (CPI) rose by 3.2% year-on-year, the fastest pace since late 2023, and remained above the 2% target for the fourth consecutive month; third, upward pressure on South Korean housing prices has intensified, particularly with rapid short-term gains in the Seoul metropolitan area. Over the past year, residential prices in Seoul have cumulatively risen by approximately 13.1%; furthermore, the publicly announced prices for Seoul apartments in 2026 rose by 18.67% year-on-year, the fastest increase in five years, with the average increase in the "Gangnam Three Districts" reaching 24.7%. The rise in housing prices and household debt is also a crucial component of the "financial stability" considerations in this rate hike; fourth, the South Korean won has been weak this year; its depreciation increases import costs and exacerbates inflationary pressure, while a rate hike can provide support for the exchange rate.

Regarding inflation, the CPI year-on-year rate further rose from 3.1% in May to 3.2% in June, the fastest pace since late 2023; the Bank of Korea had already raised its 2026 inflation forecast from 2.2% to 2.7% in May. On the growth side, performance was strong; the central bank raised its 2026 GDP growth forecast from 2.0% to 2.6%, while the government projected 3.0%, both significantly higher than the potential growth rate of approximately 1.8%, with semiconductor exports being the main engine. Exchange rates were a key driver: The US dollar against the South Korean won depreciated to 1,561.5 intraday on June 5, the weakest level in 17 years, creating an inversion of approximately 125 basis points in the policy interest rate differential with the Federal Reserve, exacerbating imported inflation and capital outflow pressures. On the financial stability front, household loans saw their largest increase in nearly one year and ten months. Shin Hyun-song summarized, "Considering price rises above target, improved growth, and rising financial stability risks, it is necessary to raise the base rate at an appropriate time."

Will there be further rate hikes? We believe the probability is relatively high. Firstly, looking domestically, even after this hike, the base rate of 2.75% still corresponds to a negative real interest rate. Monetary policy has not yet entered a restrictive zone and is insufficient to curb inflation and the housing bubble; to demonstrate determination to stabilize the real estate market, South Korean President Lee Jae-myung listed his primary residence for sale at below-market prices on July 15. Secondly, regarding internal and external balance, the interest rate differential between South Korea and the US remains significant. Against the backdrop of sustained high US interest rates and uncertainty in global capital flows, the Bank of Korea may signal a "rate hike cycle" to hedge against pressure from the interest rate differential; thirdly, the Bank of Korea's statement explicitly pointed out that "it is necessary to continue maintaining a policy stance consistent with further rate hikes" and that "the Committee will determine the timing and pace of further base rate hikes while assessing the degree of inflationary pressure, trends in domestic economic improvement, and financial stability." Following this hike, the meeting on October 22 will be the next window for further rate increases.

It is worth noting the change in wording in the forward guidance: For the first time, the decision document added the term "pace" to "timing and pace of additional rate hikes," with an intent similar to the Federal Reserve's logic of conveying signals through subtle adjustments in statement wording, leaving room for flexibility in batched, gradual rate hikes. Regarding internal stance, the May meeting saw a 5-to-2 hawkish split, with two members advocating for an immediate rate hike at that time, whereas this time it converged to a unanimous vote—indicating that the committee's focus has overall shifted towards "tightening again." The market generally expects no move in August, another hike in October, a year-end base rate of 3.0%, and a terminal rate for this cycle of approximately 3.0%–3.5% (to be reached in the first half of 2027). It is worth noting that the new Bank of Korea Governor, Shin Hyun-song, comes from the Bank for International Settlements (BIS), with a distinct focus on financial stability and macro-prudential policy. This resolution's attention to household and stock market leverage bears his distinct policy imprint.

The South Korean stock market has undergone a significant correction over the past month or so. The KOSPI Index fell by 25% on July 16 compared to June 22. We understand that, firstly, obvious vulnerabilities and leverage risks had accumulated previously. The high point of the KOSPI Index on June 22 was 114.0% higher than the closing price on the last trading day of 2025; as of June 24, the total number of domestic stock trading accounts in South Korea reached 108.7 million (an increase of over 10 million from 98.28 million at the end of 2025), while the total population of South Korea is only about 51.7 million. The balance of credit financing once hit a historical peak of 38.63 trillion South Korean won on June 24—highlighting the market's distinct "leveraged" characteristics. Secondly, fundamental triggers: Market skepticism arose regarding the sustainability of memory chip price increases, with expectations that price gains would slow in the second half of the year. Thirdly, the tightening of monetary policy by the Bank of Korea further triggered expectations of liquidity contraction. Fourthly, external disturbances: The US launch of Section 337 investigations against companies such as Samsung Electronics also had some impact. Simply put, this is a typical case superimposing "accumulated market leverage risk + marginal changes in fundamentals + liquidity tightening boost + external factor disturbances."

This round of adjustment stems from the resonance of multiple factors. First, the shaking of fundamental expectations: Memory chip price increases have not yet turned into declines, but rather the "slope of price increases has slowed"—TrendForce data shows that regular DRAM contract prices rose quarter-on-quarter by about 93%–98% in Q1, about 58%–63% in Q2, and server DRAM narrowed to about 13%–18% in Q3. Coupled with doubts about whether large cloud service providers (CSPs) can maintain AI capital expenditure, this has shaken market confidence in the technology sector as a whole. Second, passive deleveraging under changing fundamental expectations: Under the high-leverage structure composed of 108.7 million accounts, 38.63 trillion South Korean won in financing balances, and single-stock leveraged ETFs listed in late May, forced liquidations mechanically amplified the decline, turning a cooling at the fundamental level into a stampede at the index level.

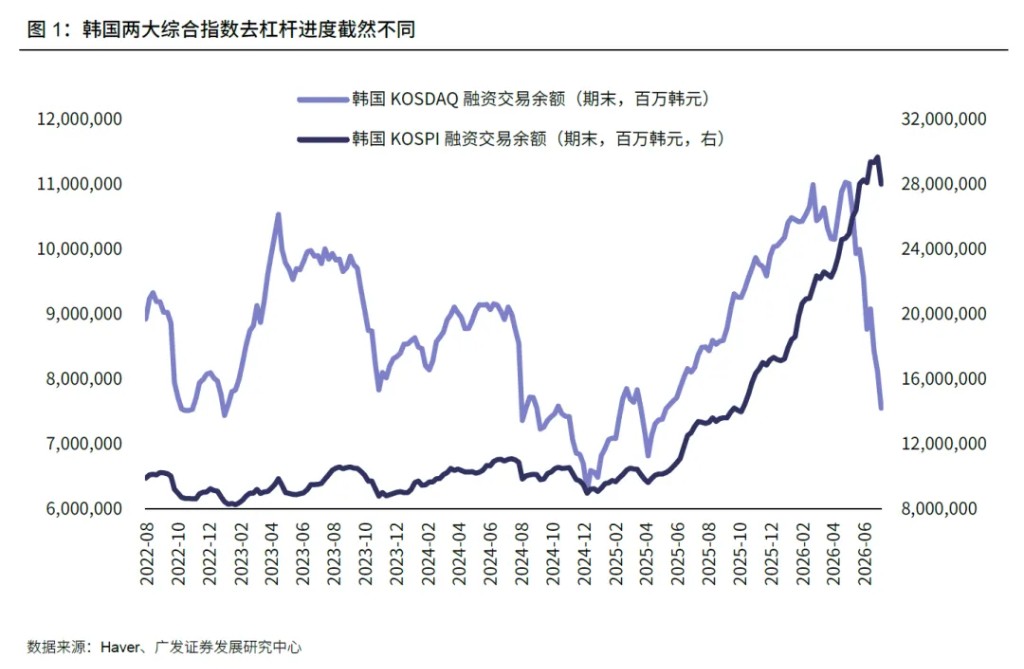

It is worth emphasizing that the progress of deleveraging differs significantly between two sectors: KOSDAQ financing balances have fallen sharply from their peak, with leverage basically cleared; whereas KOSPI financing balances have only decreased slightly, and due to simultaneous shrinkage in market capitalization, the financing-to-market-cap ratio has actually risen instead of falling, returning to historical highs near the peak of the 2021 bull market—leverage on the main board has not truly been cleared. This means that rate hikes and the Section 337 investigations are more of a boost and disturbance rather than the primary cause (the 25 basis point hike was fully expected, and semiconductors continued to adjust against the backdrop of weakening US PPI, precisely confirming that the adjustment was driven by sector sentiment rather than monetary factors); the core issue remains whether the memory chip price increases can be falsified. If contract price gains narrow further in the second half of the year and the mass production timeline for HBM4 is delayed again, the high-level leverage in KOSPI that has not yet been cleared poses a tail risk of triggering a second wave, concentrated in deleveraging of weighted stocks; conversely, once the slowdown in price increases is falsified and profit expectations are revised upward, this round of adjustment, dominated by leverage and sentiment, also possesses the elasticity for a rapid recovery.

As there have been no explicit changes in the economic fundamentals or the fundamentals of the technology industry, the South Korean stock market should find stabilization momentum after adjusting to a relatively reasonable level. However, it is worth noting that a fundamental closed loop of the global technology industry cycle this year is US capital expenditure and exports from Asia (China, South Korea). After this adjustment in the South Korean market, unilateral expectations for the global technology supply chain are expected to weaken. From a fundamental perspective, subsequent observations should focus on two areas: first, South Korean semiconductor exports (ten-day data) and TrendForce's quarterly DRAM/NAND contract prices; second, closely monitoring the pace of South Korea's current rate hike cycle.

Guo Lei Macro Tea House

Risk Warning and Disclaimer

The market involves risks; investment requires caution. This article does not constitute personal investment advice, nor does it take into account the specific investment objectives, financial status, or needs of individual users. Users should consider whether any opinions, views, or conclusions in this article align with their specific circumstances. Investment based on this content is at your own risk.