Car deliveries are the foundation, physical AI is the bull market engine! Tesla's performance is coming, Morgan Stanley is closely watching Robotaxi, Optimus Prime, and energy storage "three arrows in unison."

Morgan Stanley raised its target price for Tesla from $415 to $417, maintaining a "Hold" rating. Analysts believe that while improvements in automotive and energy storage deliveries have enhanced the earnings floor, the key to whether Tesla can be re-rated lies in whether Robotaxi, FSD, and the Optimus humanoid robot can prove that its physical AI system has entered a scalable commercial phase. Currently, the market still faces pressure testing on the realization of its AI valuation

According to the Zhitong Finance APP, the South Korean stock market, known as the "AI computing power barometer," has recently frequently fallen into both upward and downward circuit breakers. Coupled with the extreme and severe sell-off caused by the overcrowded and highly leveraged long positions in global AI computing power theme stocks and the semiconductor sector, Wall Street financial giant Morgan Stanley has taken a cautious stance on the valuation outlook and target price expectations for Tesla (TSLA.US), a leader in electric vehicles, AI, autonomous driving, and robotics. The analysis team led by senior analyst Andrew Percoco at Morgan Stanley has slightly raised Tesla's target price from $415 to $417, maintaining an "Equal-weight" rating. In contrast, Tesla's stock price closed at $391.06 on Thursday.

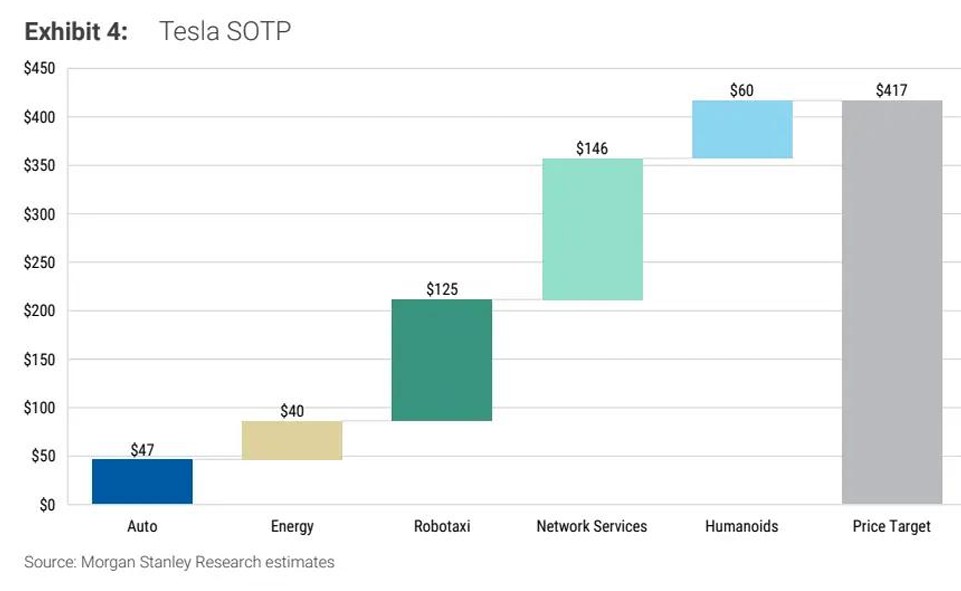

Morgan Stanley's valuation framework shows that the electric vehicle business contributes only $47 to the target value, while Robotaxi, network services, and humanoid robots collectively contribute $330; the recent delivery of 480,100 vehicles and the deployment of 13.5 GWh energy storage systems (which may be closely related to AI data centers) have strengthened Tesla's AI fundamental base. However, the increasingly large artificial intelligence capital expenditure exceeding $25 billion, continued negative free cash flow, and the speed of Robotaxi demand and capacity expansion, along with the mass production schedule and demand expansion pace of the Optimus humanoid robot, remain core pressure tests related to whether the extremely optimistic market valuation associated with Tesla's uniquely built AI computing power infrastructure and AI applications can be realized.

It is reported that the core judgment logic of Morgan Stanley's analyst team regarding the target stock price expectation for Tesla, one of the Magnificent Seven in the U.S. stock market, is very clear: stronger-than-expected improvements in electric vehicle deliveries have improved the recent earnings floor, but what determines whether Tesla can be re-rated is not just selling a few more thousand cars, but whether the massive energy storage systems related to Robotaxi, FSD, Optimus, and AI can prove that Tesla's uniquely possessed physical AI system has entered the stage of scaled commercialization.

$417 is a highly "AI-driven" valuation, not an automotive valuation: the automotive recovery is just the base, while physical AI is the bull market engine for stock prices.

Tesla will announce its quarterly results next Thursday morning Beijing time. Morgan Stanley expects second-quarter revenue to be $28.363 billion, 11% higher than the market consensus; adjusted EPS is expected to be $0.69, 41% higher than expectations; the gross margin of the automotive business, excluding credits, is expected to be 18.1%, slightly above the market expectation of 18.0%. However, the full-year outlook is not entirely optimistic: the revenue forecast for 2026 is $102.4 billion, slightly lower than market expectations; adjusted EBITDA is expected to be $16.181 billion, and EPS is expected to be $2.20, both exceeding market expectations by 3.4% and 13.4%, respectively; meanwhile, capital expenditures are expected to reach $26.8 billion, and free cash flow is expected to be negative $11.432 billion, significantly worse than the market expectation of negative $8.136 billion In other words, according to the analysts at Morgan Stanley, Tesla is using the cash flow base formed by the phased recovery of its automotive business to fund an unprecedented arms race in cutting-edge AI, FSD autonomous driving software, Robotaxi, energy storage systems, humanoid robots, and AI chip manufacturing infrastructure dominated by Musk's "Terafab" vision.

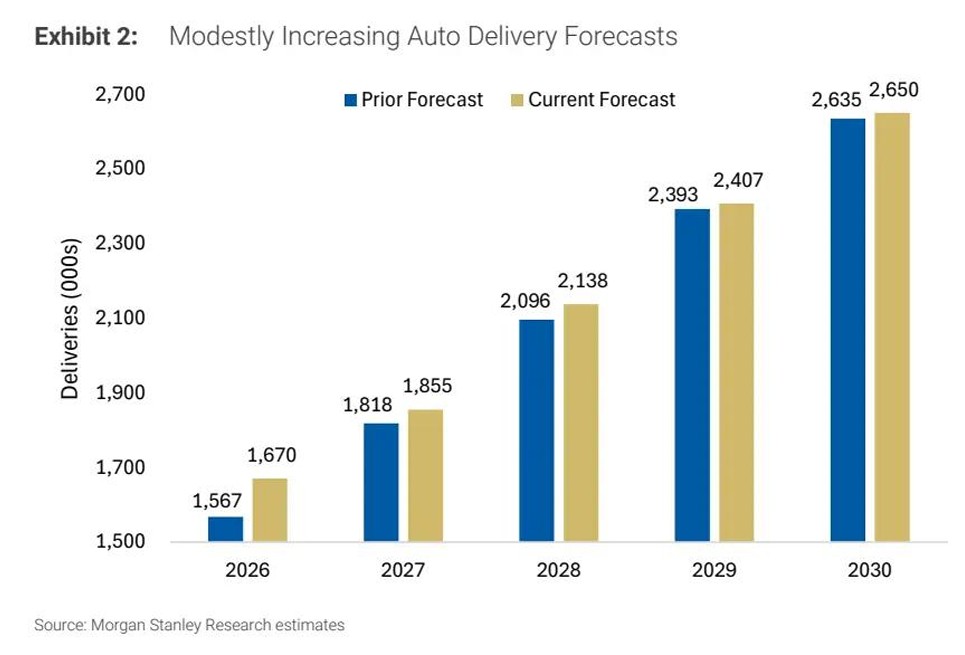

Morgan Stanley's forecast path implies that from 2026 to 2028, the compound annual growth rate of revenue will be about 17%, but it will continue to burn cash in 2026 and 2027, only returning to positive free cash flow in 2028. Therefore, Morgan Stanley's outlook for Tesla's future performance is a moderate recovery in revenue and deliveries, stabilization of traditional automotive profits, but AI investments will first consume cash flow before waiting for commercialization to materialize. Their model does not assume that the traditional automotive business will re-enter hyper-growth: the delivery forecast for 2030 is only slightly increased from 2.635 million to 2.65 million; the real long-term profit elasticity comes from the expansion of AI-driven energy storage systems, FSD subscriptions, Robotaxi platform commissions, fleet services, and strong demand for Optimus.

Morgan Stanley's target price of $417 consists of five parts: $47 for traditional automotive business, $40 for energy storage and energy business, $125 for Robotaxi/Tesla Mobility, $146 for Network Services, and $60 for Humanoids (i.e., the Optimus humanoid robot business). This means that network services, Robotaxi, and humanoid robots contribute approximately 79% of the target valuation, while traditional automotive contributes only about 11%.

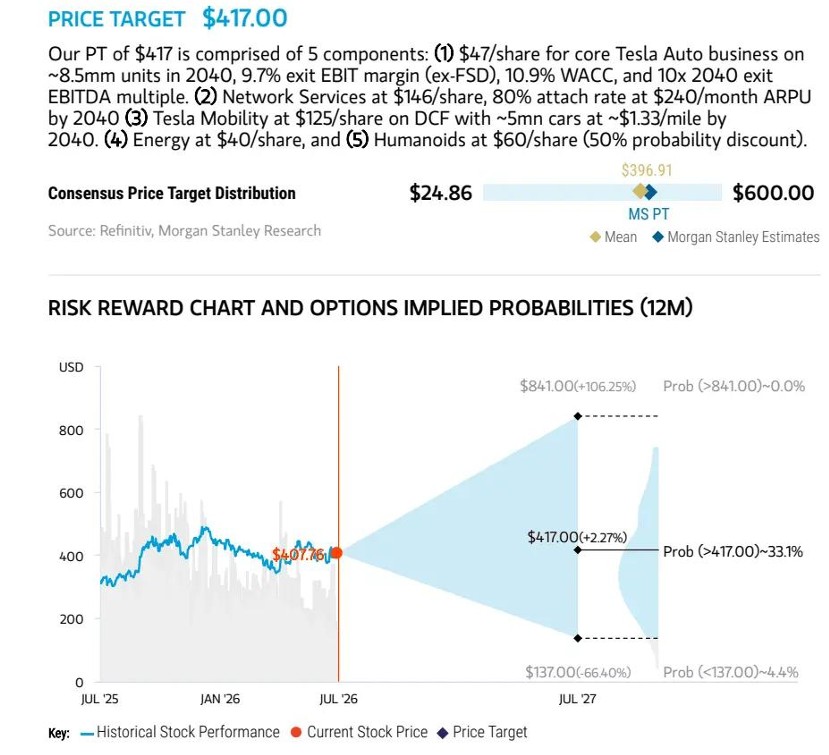

Even in the baseline forecast scenario, the overall valuation given by Morgan Stanley still corresponds to about 53 times the expected EV/EBITDA for 2030; the bull market scenario target price is $841, while the bear market scenario is only $137. This extremely wide valuation range indicates that Tesla is no longer priced linearly based on vehicle sales and per-vehicle profits, but rather on whether the physical AI system of Tesla, including autonomous driving and robotics, can form a giant platform economy.

In terms of FSD and Robotaxi, the underlying technological progress is indeed accumulating: Tesla claims that FSD v14.3 has restructured the reinforcement learning phase, improved low-visibility visual encoders, and reduced inference latency by up to 20%; the next-generation AI5 inference chip has completed its final design. The paid mileage for Robotaxi nearly doubled quarter-over-quarter, with Austin, Dallas, and Houston advancing towards unmanned operations, and expanding to Miami in July Morgan Stanley expects that by the end of 2026, there will be approximately 1,500 supervised and unmanned Robotaxis, and about 30,000 by 2030. However, it also emphasizes that the absolute fleet size this year will not contribute significantly to profits; what the market is really observing is urban expansion, operation without safety drivers, and the production speed of Cybercab.

Optimus is also transitioning from laboratory prototypes to manufacturing readiness: Tesla has begun installing the first generation of production lines. Morgan Stanley's supply chain survey shows that the company has asked some suppliers to increase their component production capacity to about 1,000 sets per week before September, reaching 2,000 to 2,500 sets per week by the end of the year. However, key obstacles remain, including final design freeze, reliability of dexterous hands, actuator lifespan, industrial safety certification, and unit manufacturing costs. Therefore, supply chain stocking cannot be equated with robots having achieved large-scale commercial delivery. Morgan Stanley only values Humanoids at $60 with an additional 50% probability discount, which already reflects the judgment of the coexistence of this enormous potential market and high execution risks.

The energy storage business is the intersection where Tesla and AI infrastructure are most easily underestimated. The deployment of 13.5 GWh in the second quarter reached a strong level, and Megapack 3 is still planned to enter mass production in 2026. As AI data center loads exhibit high power and strong volatility characteristics, battery storage can be used to smooth peak loads, improve transmission capacity utilization, respond to power outages, and reduce reliance on diesel backup units. However, Morgan Stanley expects a total deployment of 57.7 GWh for the year, lower than the market expectation of 60 GWh, and the forecast for energy gross margins is also below consensus, indicating that demand is not the issue; the short-term bottleneck mainly lies in the supply chain, project grid connection, and product mix. Strictly speaking, the Megapack energy storage project is not an absolutely independent "AI computing power energy storage business," but rather Megapack is becoming an important supporting asset for the power infrastructure of AI data centers.

Morgan Stanley has left a hand with an "841 USD bullish target price" to respond to Musk's ambitious push for physical AI

According to the baseline target price expectation scenario from Morgan Stanley's analyst team, there is not a very strong upside potential; under the scenario of successful AI realization, there is significant convexity. Based on Tesla's latest stock price of approximately $391.06, Morgan Stanley's target price of $417 corresponds to only about a 6.6% potential increase, which is entirely consistent with its "Equal-weight" rating.

However, the bullish scenario of $841 corresponds to about 115% upside potential and a potential market value of nearly $2.98 trillion. The $841 bullish target price is based on the assumption that various businesses such as Robotaxi, network services, FSD autonomous driving subscriptions, energy storage systems, humanoid robots, and the potential chip manufacturing plant Terafab will achieve much more optimistic realizations under the leadership of CEO Musk, rather than the 12-month baseline target price.

Morgan Stanley analysts stated that the $841 target price is not an official target but a scenario valuation based on the simultaneous realization of the Robotaxi fleet, high FSD attachment rates, high ARPU from network services, commercialization of Optimus, and expansion of the energy business. Currently, Tesla's market capitalization is approximately $1.38 trillion, with a static P/E ratio of about 359 times, which has already factored in a significant probability of AI success. Therefore, future stock prices will not continue to rise solely due to "progress" in AI computing power, AI applications, and physical AI-related projects, but will need to demonstrate that these businesses can generate sustainable cash flow through unsupervised safe mileage, Robotaxi fleet utilization, FSD subscriptions and gross margins, Optimus production yield, and capital expenditure return rates.

Morgan Stanley analysts stated that the $841 target price is not an official target but a scenario valuation based on the simultaneous realization of the Robotaxi fleet, high FSD attachment rates, high ARPU from network services, commercialization of Optimus, and expansion of the energy business. Currently, Tesla's market capitalization is approximately $1.38 trillion, with a static P/E ratio of about 359 times, which has already factored in a significant probability of AI success. Therefore, future stock prices will not continue to rise solely due to "progress" in AI computing power, AI applications, and physical AI-related projects, but will need to demonstrate that these businesses can generate sustainable cash flow through unsupervised safe mileage, Robotaxi fleet utilization, FSD subscriptions and gross margins, Optimus production yield, and capital expenditure return rates.

Regarding the most optimistic benchmark target price on Wall Street, according to mainstream sell-side 12-month target price estimates, the highest currently is the $600 benchmark target price given by Wedbush analyst Dan Ives. Based on the latest price of $391.06, this implies an upside potential of approximately 53.4%, corresponding to a potential market capitalization of about $2.12 trillion.

Similar to Morgan Stanley's predictions, Ives' core logic is not about the electric vehicle sales cycle, but rather that investors underestimate Tesla's transformation from an electric vehicle manufacturer to a "physical AI super platform": Tesla's AI supercomputing system-driven FSD autonomous driving software transforms the existing fleet into a high-margin software network, Robotaxi turns autonomous driving into a mileage-based mobile service, and Optimus further extends the same set of vision, reasoning, and control capabilities to the general labor market. In other words, the $600 benchmark target price given by Wedbush analyst Dan Ives bets on cutting-edge AI technology, autonomous driving and robotics, and energy storage systems jointly driving the reconstruction of Tesla's business model and valuation multiples; if the Robotaxi expansion plan or Optimus mass production is delayed, the valuation premium on which this target relies will also quickly shrink