NVIDIA's Q2 earnings report falsification and inflated stock price? Wall Street analysts refute: Don't blindly believe everything you see online, guys.

社交媒體上的陰謀論者質疑,英偉達參投的 AI 初創企業 Coreweave 協助做局增厚二季度收入,更多大廠可能也合謀以抬升股價,財報多個方面看似 “疑點重重”。這背後證明多空博弈非常膠着,底層邏輯是擔心 AI 泡沫一旦破裂將拉垮整個大盤。

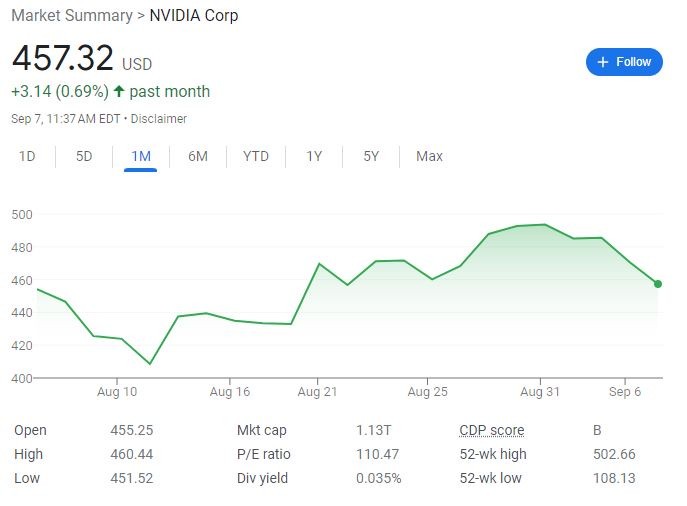

近日,有關英偉達二季度 “破紀錄” 財報涉嫌造假的陰謀論正在社交媒體和投資者論壇中甚囂塵上,令 9 月 6 日和 7 日的股價均跌約 3%,抹去 8 月 23 日盤後公佈二季報以來的全部漲幅。

英偉達的不佳表現,拖累芯片行業基準——費城半導體指數週四盤初跌超 3%,其在 GPU 領域的競爭對手 AMD 一度跌近 4%,蘋果、微軟、谷歌等受益於 AI 熱潮的大型科技股也持續低迷。

英偉達跌價的原因,除了與 “油價漲至近十個月最高,以及美國經濟數據保持韌性,令市場對 11 月美聯儲再度加息的預期升温,進而推動美債收益率連續上漲,令股市等風險資產承壓” 這一邏輯有關,針對其財報後股價創歷史新高、且年內大漲逾 200% 的華爾街多空交戰也尤為激烈。

英偉達成本沒增加但收入同比翻倍?渠道調查顯示企業並未大幅增加 AI資本支出?

據研投機構 Macrotips Trading 總結,儘管英偉達二季報遠超預期並對未來收入的指引更為強勁,但人們有理由對 “可疑的披露和管理行為感到擔憂”,特別是該公司直接投資支持的一家 AI 初創公司參與推動了收入增長,毛利率擴張、股票回購時機古怪和內部人士拋售也發出了危險信號。

該機構撰文稱,在剛剛過去的第二季度,英偉達總收入同比翻倍增長 102% 至 135 億美元,比分析師的預期高出 24 億美元。其中,鑑於對支持大語言模型和生成式人工智能的 GPU 需求強勁,其數據中心收入同比增長 171%、環比增 141% 至 103 億美元,較市場預期高出 23 億美元:

“更令人難以置信的是,英偉達是在幾乎沒有增加成本的情況下實現了驚人增長,其收入成本同比僅增長了 6.8%,毛利率卻達到聞所未聞的 70.1%。

英偉達還為第三季度收入制定了 160 億美元的宏偉目標,遠高於分析師預期的 125 億美元。英偉達市值 1.2 萬億美元,以前如此巨量規模的公司季報從未以如此大的幅度超出過市場預期。

這不禁令人驚訝為何華爾街的預期完全沒有押中其快速增長。按理説,超過 40 名覆蓋該公司的分析師在財報前至少都用 10 種方式開展和分析過每一種可以想到的渠道檢查了。

例如,在財報發佈前,丹麥盛寶銀行分析了主要人工智能參與者的第二季度資本支出,卻沒有發現有資本支出高企的跡象能表明對英偉達 GPU 需求如此強勁。”

這便令人質疑 “在生成式 AI 需求激增基礎之上的英偉達數據中心收入大漲” 究竟是如何做到的。一些市場參與者馬上將目光投到了英偉達支持的 AI 初創公司 Coreweave 身上。

陰謀論者質疑英偉達投資的 Coreweave協助做局增厚二季度收入,更多大廠可能也合謀!

上述文章稱,有理由懷疑,英偉達直接資助的 Coreweave 公司是英偉達收入激增的背後主因。

首先,Coreweave 向英偉達等多家投資者出售了 4.21 億美元股權,可能令英偉達對前者的購買決策產生控制權。同時,Coreweave 在 8 月初通過抵押英偉達 GPU 完成了債務融資 23 億美元,這一數額恰恰等於包含 AI 芯片業務的英偉達數據中心二季度收入超過市場預期之規模:

“雖然這可能是完全合法的,但英偉達資助了這家初創公司,後者又通過由抵押英偉達 GPU 得到的貸款來購買了上述這批 GPU,這種做法要求英偉達理由更好地披露與其客户的關係。”

還有懷疑論者認為,向英偉達下了數十億美元訂單的 AI 科技公司 Coreweave 甚至可能都不是一家真正的公司,而是由英偉達最大股東、資管巨頭貝萊德與英偉達合作創建並支持的空殼機構。

有人説,英偉達還與微軟、亞馬遜 AWS 和全球排名第三的大模型初創公司 Inflection 等 “大廠” 合謀做局,主要業內玩家給英偉達下了較多訂單,這些訂單都有問題,是為了配合英偉達做收入:

“有一個讓人難以置信的理論在 X/Twitter 上越來越受到關注,認為英偉達今年的驚人財報表現是通過向虛假且不存在的客户出售假 GPU 來推動的。

一些人已經開始將這個事件與 FTX 金字塔騙局慘敗進行類比,並擔心這樣的騙局可能會拖垮整個 AI/芯片市場。”

分析:陰謀論證明對英偉達多空博弈非常膠着,底層是擔心 AI泡沫破裂拉垮整個大盤

但券商伯恩斯坦的分析師拉斯貢(Stacy Rasgon)對這種陰謀論表達了強烈的不滿,本週其最新研報直言:“客户老鐵們,拜託不要相信從社交媒體上隨便看來的幼稚投資論點。”

對於英偉達收入同比翻倍、銷售成本僅增長 7% 的懷疑觀點,拉斯貢稱,這是因為英偉達二季度錄入的費用中包括了約 12.2 億美元的庫存準備金,這在去年二季度被算進了銷售成本,“當排除這些費用時,與一年前相比,第二季度的銷售成本實際上增加了約 70%,屬於完全正常的範疇。”

第二個主流質疑涉及從北美最大以太坊礦工轉型為 GPU 雲供應商的 Coreweave,拉斯貢提醒稱,該公司抵押英偉達 H100 芯片換取的是黑石集團(Blackstone)主導債務融資,不是英偉達大股東貝萊德集團(Blackrock),陰謀論的這個解讀錯誤本身就夠滑稽了,而且:

“英偉達也不需要來自 Coreweave(或其他任何人)的幫助來刺激二季度銷量,英偉達的產品早都已經分配出去了。

況且,這項債務協議是在 8 月 3 日二季度完結之後宣佈的,債務發行方暗示資金部署可能尚未發生。(這又如何來虛假增厚二季度英偉達的財報呢?)”

還有分析指出,8 月融資以前 Coreweave 的自有資金僅為 3.71 億美元,這種體量的公司怎麼有能力與二季度數據中心收入突破 100 億美元的英偉達聯合操作收入呢:

目前根本沒有直接證據指向兩者做局,唯一被人詬病的就是英偉達在產能奇缺時特別支持了自己投資的公司而已。

支持英偉達的人們普遍認為,社交媒體上流行的陰謀論只能説明一點,即目前針對英偉達的多空博弈非常膠着。其底層邏輯可能是對 “AI助推下一個科技泡沫破裂” 觀點的深深恐懼與擔憂。

在定量投資界知名的羅布·阿諾特(Rob Arnott)本週便稱,英偉達是即將破裂的 AI 股票泡沫領頭羊,被刺破後可能拖垮整個市場,英偉達今年大漲正是 “重大市場錯覺” 的教科書案例:

“要記住一點,每當牛市出現在僅能推動一小部分受歡迎公司股價上漲的強大敍事中時,這些股票在未來幾年可能會令人失望。2000 年科技泡沫和 2008 年金融危機後都上演了這種範式。

人工智能將改變我們的世界,這一點毋庸置疑。但英偉達的股價表明,市場認為其未來不會受到同行業新進入者,或者質疑其主導地位的監管機構的挑戰,這種説法已超出了合理的現實。”

質疑英偉達二季度財報造假的人還有哪些疑慮?股票回購時機、高估值不可持續

再回到文初 Macrotips Trading 的質疑文章中,與社交媒體上刻意渲染焦慮情緒的懷疑論不同,這篇分析文深度剖析了英偉達二季度財報,並提出了幾個值得人思考的觀點。

首先,英偉達過去幾個季度的毛利率 “擴張令人難以置信,從去年二季度的 43.5% 飛躍至今年一季度的 64.6%,並在今年二季度擴大至 70.1%,競爭對手 AMD 的毛利率卻同比保持穩定:

“也許英偉達毛利率擴張,只是反映了其 GPU 在炙手可熱的人工智能和生成式 AI 芯片市場中的需求量之大,客户願意為英偉達芯片支付雙倍價格,從而在不過多增加成本時將其收入翻倍。

但需要考慮英偉達針對許可和開發安排(License and Development Arrangement)的收入確認規則。與產品發貨導致控制權轉移便能確認收入的產品銷售不同,數據中心收入的一部分可能來自軟件許可,在軟件可供客户使用時便能預先確認收入,即便客户實際付款是稍後才進行的。

這種即使尚未收到付款也能提前確認收入的政策,可以解釋為什麼英偉達二季度的應收賬款環比躍升 30 億美元至 71 億美元。而且,今年二季度的應收賬款還受益於客户在發票到期日之前付款的 12.5 億美元。這些都推動英偉達的季度整體收入環比增長了 63 億美元之多。”

第二,文章還質疑英偉達股票回購的時機。在二季度末剩餘 40 億美元此前批准回購計劃有待執行的基礎上,該公司董事會又批准了 250 億美元的最新回購計劃:

“英偉達管理層的選擇令人費解。財報顯示,一季度其沒有回購任何股票,二季度以 32.8 億美元回購了 750 萬股,還於今年 7 月 31 日至 8 月 24 日期間以 9.98 億美元回購了 200 萬股。

計算可知,750 萬股價值 32.8 億美元,等於平均回購股價為 437 美元,200 萬股價值 9.98 億美元,等於平均股價 499 美元。

而在截至 7 月 30 日的英偉達財年二季度中,僅有幾天交投高於 437 美元,為了令平均價格為 437 美元,這代表該公司必須在第二財季末回購股票,當時該股已經接近歷史最高。同理,7 月 31 日至 8 月 24 日之間,僅 8 月 24 日當天股價超過 499 美元,代表大部分回購肯定在這一天發生。

(玄妙的是,英偉達幾乎選擇股價接近歷史最高點時才出手回購),但大多數公司在回購股票時,都會通過較長時間內的成交量加權平均價格等計劃來回購,以免過度影響股價。”

第三,該文章還質疑,在該公司不斷以歷史高點回購股票時,英偉達內部人士一直在加速拋售持股:

過去 6 個月中,內部人士出售了 2.34 億美元的股票,其中 CFO 在 8 月 28 日出售 230 萬美元、在 5 月 30 日出售 250 萬美元,CEO 黃仁勳近期行使了股票期權將於 9 月 1 日出售 1.17 億美元。

最後,文章稱英偉達當前估值 “已高出天際”,交易價格是未來企業銷售價值(Fwd EV/Sales)的高達 16.7 倍,以及滾動市盈率(trailing P/E)的 117 倍:

“即使分析師的預測正確,即英偉達可以在 2027 財年(2026 日曆年)將收入增至 1110 億美元,該公司當前 1.2 萬億美元的企業價值仍然超過 EV/銷售額的 10 倍。

雖然人工智能和英偉達 GPU 很可能會改變我們所知的世界,但以未來三年預計銷售額的至少 10 倍來估值英偉達,將令其泡沫甚至比 2000 年的互聯網泡沫更令人震驚。

隨着內部人士拋售加速,持有英偉達股票的風險似乎也在上升。我個人對持有一家估值建立在三年後預期收入 10 多倍的公司感到不舒服。我不會做空英偉達股票,但當前持有者應該賣出。”

英偉達高管和業內主流人士沒有在怕:AI市場規模可達 6000億美元,趨勢毋庸置疑

但英偉達高管似乎無懼市場上的懷疑論聲音。

在本週高盛舉辦的科技會議上,英偉達主管企業計算的副總裁達斯(Manuvir Das)預言,人工智能的長期潛在市場價值高達 6000 億美元。

這將由 3000 億美元的芯片和系統、1500 億美元的生成式人工智能軟件,以及 1500 億美元的全宇宙(omniverse)企業軟件構成,被英偉達提倡的 “加速計算”(accelerated computing)所助力。

達斯稱,英偉達正在利用一個不可避免的行業趨勢資本化,即最終企業運營將走向數字化,並以從前難以想象的方式提高效率:

“看待英偉達最簡單的方式就是我們下了個大賭注(而且賭贏了),此前我們為此已經醖釀了幾十年了。”

數字化基建解決方案供應商 EdgeCore 的數字基礎設施戰略高級副總裁 Tom Traugott 也稱,人工智能熱潮下,關鍵基礎設施正在發生變化,可能會產生深遠影響:

“企業們將不得不通過改進現有系統來滿足對 AI 的需求,進而推動對支持數據中心向更高效 GPU 轉型的英偉達芯片需求。

一家公司可能擁有 AI 芯片供分配,但下一個關鍵問題是他們是否擁有使這些芯片可以發揮用途的數據中心容量。人工智能正在推動數據中心建築比以往更大、更密集。”

與網上陰謀論不同,據 FactSet 統計,在覆蓋英偉達的 51 位華爾街專業分析師中,有 47 人給予 “買入” 評級,4 人評級 “持有”,無人評級賣出,平均目標價為 649.22 美元,還有 42% 的漲幅空間。