🦎 CHINA REIT YIELD VS. THE REAL COST

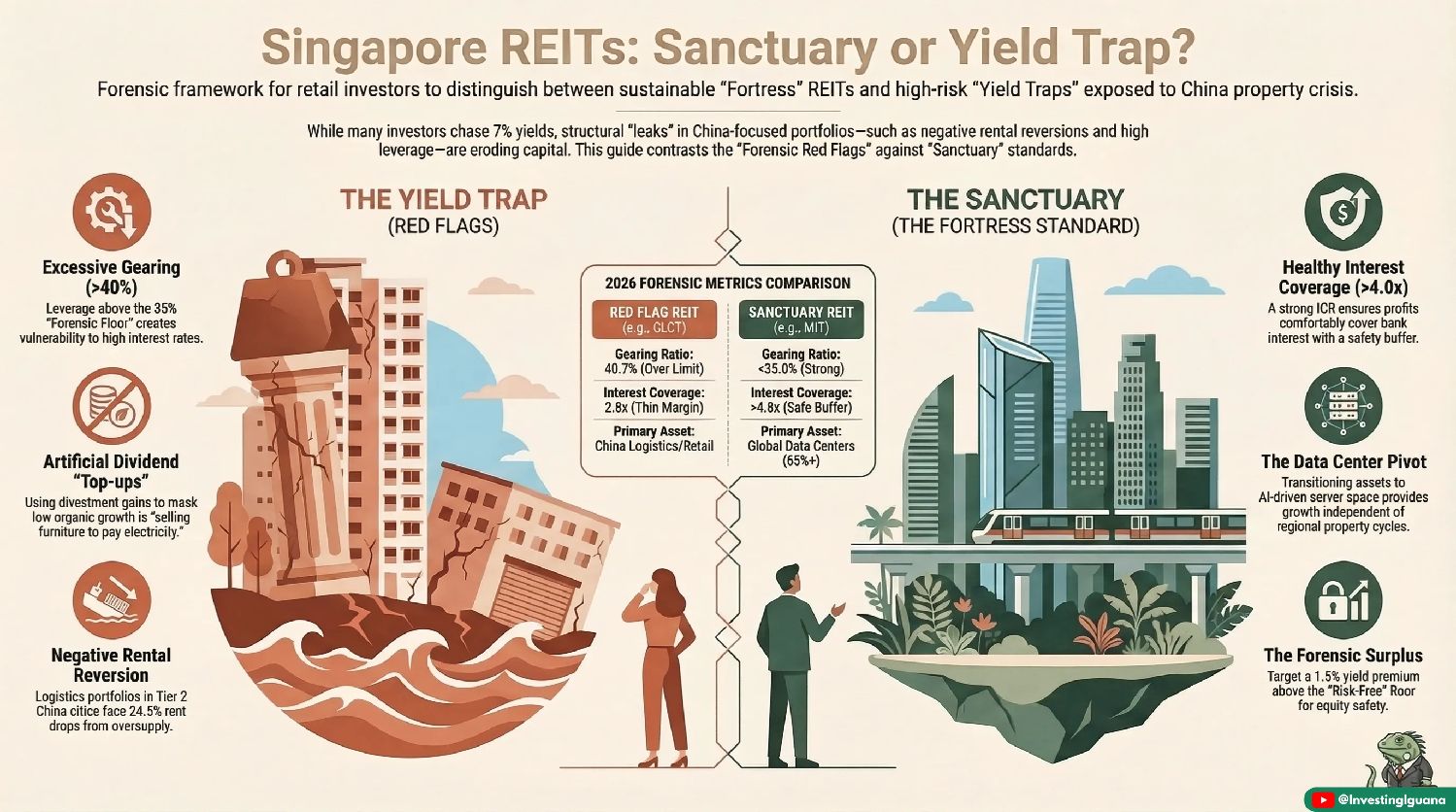

There’s a quiet tax sitting inside many China-heavy REITs. On the surface you see 6–7% yield. Under the hood, you’re looking at 40.7% gearing, 2.8x interest cover and a 2027 refinancing wall where higher interest costs meet falling rents. That is when your “passive income” becomes the buffer to save the balance sheet, not your retirement.

Gearing at 40.7% already fails my <35% Forensic Standard. An ICR of 2.8x vs my >4x rule means for every S$1 of interest, there’s only S$2.80 of profit. Add in negative rental reversions and divestment gains topping up DPU, and you get the classic Yield Trap: your income looks fat, your capital quietly bleeds. Compare that to a Sanctuary like MIT with a 5.8% yield and a 1.1% surplus over my 4.7% hurdle. Same headline ballpark, totally different risk profile.

Gearing <35%. ICR >4x. Yield must clear 4.7% to count as a Sanctuary.

📺 YouTube: https://youtu.be/PZqiWfav4xM

📩 Substack: https://investingiguana.substack.com/p/capitaland-china-trust-clct-divestment

🦎 Brought to you by Longbridge SG — Iggy's exclusive pilot programme.

🔗

https://tinyurl.com/iggyinvesting

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.