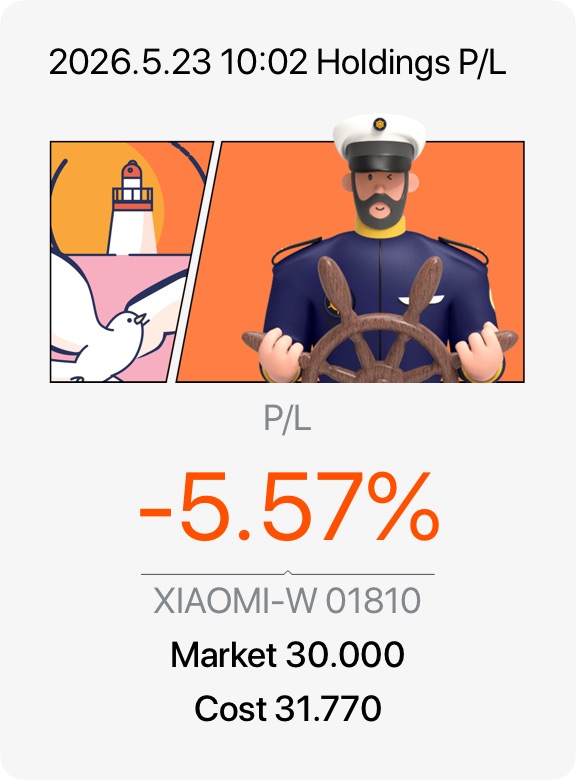

$XIAOMI-W(01810.HK)

Next Tuesday (May 26) is a critical milestone for Xiaomi as they report their Q1 2026 earnings. I am particularly focused on management’s forward profit guidance and updates regarding the overseas expansion strategy for their EV lineup.

The Current Valuation Snapshots are as below:

1️⃣ P/E Ratio (TTM): 16.81 (Trading below the Asian Tech Industry average of ~21.5x, offering strong relative value)

2️⃣ P/B Ratio: 2.63 (Reflects solid asset backing from its massive smartphone/AIoT inventory and cash)

3️⃣ P/S Ratio: 1.43x (Indicating the market is valuing its massive RMB 100B+ quarterly revenue engine quite conservatively)

4️⃣ Forward P/E: 20.9x (Factoring in near-term margin digestion from the EV ramp-up).

Given the weekend news of renewed Chinese regulatory pressure on cross-border brokerages, are you buying at current valuations or waiting for a potential market dip on Monday? Let’s discuss😉.

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.