Nomura Securities refutes the claim that "the semiconductor market has peaked." Nomura Securities warns that the AI semiconductor cycle is far from its peak, and an "epic" supply chain mismatch may occur in the second half of 2026. It is recommended that you save this information. Cloud service providers continue to expand capital expenditures. Shortages of components such as advanced packaging, printed circuit boards (PCBs), and copper-clad laminates (CCLs) will drive up prices and raise profit expectations.

> In the second half of 2026, the market will face the most severe supply chain mismatch in history. Supply bottlenecks will shift to wafer-level substrates (WoS) and small components such as printed circuit boards (PCBs) and copper-clad laminates (CCLs).

> Forecasts 78% growth in AI server revenue in 2026 and 76% in 2027. Based on this, the company reiterated its "buy" ratings for nine Asian AI technology companies, including TSMC ($TSMC) and MediaTek.http://2454.TW )$ASE, and raised all target prices, advising investors to buy during market weakness. > The rise of agent AI has unexpectedly driven a surge in demand for traditional server CPUs, opening up new market opportunities for the semiconductor testing and packaging industry.

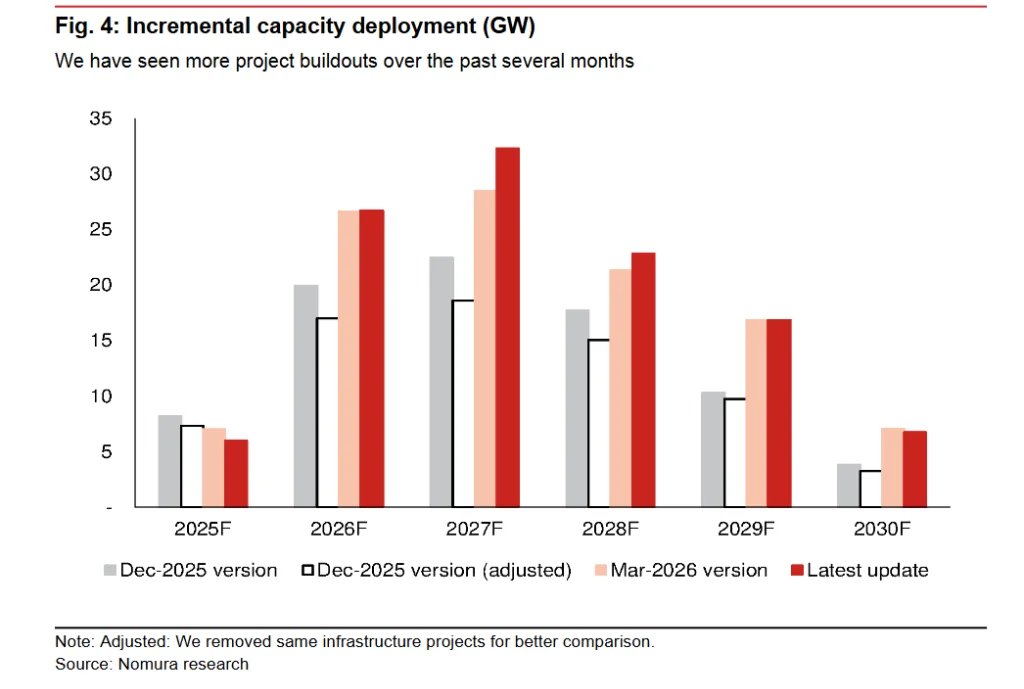

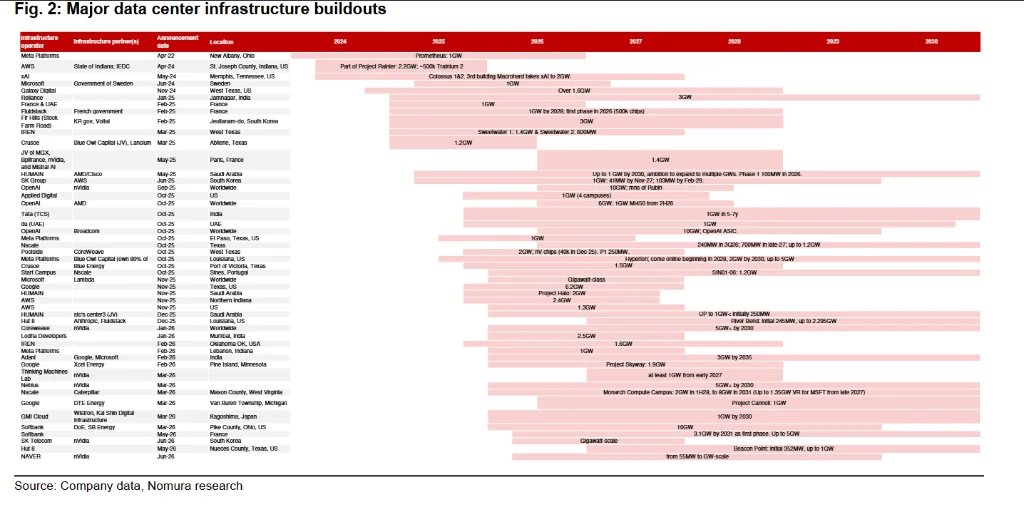

> In addition to memory, CPUs, etc., bottlenecks are also expected in these areas due to shortages of integrated circuit substrates, high-end capacitors, power management integrated circuits, and optical components. Demand in the consumer electronics and automotive sectors is expected to grow. > Nomura's proprietary data shows that the number of global data center projects it tracks has increased from 240 to 280, with gigawatt (GW)-scale projects increasing to about 50. The company expects 32 GW of new computing capacity to be deployed in 2027, of which 23 GW is already confirmed to be operational by 2028.

> The Chinese government has formulated an unprecedented national AI computing infrastructure plan, planning to invest $295 billion over the next five years, aiming to achieve nationwide interconnection of distributed data centers by 2028.

> Nomura predicts that TSMC's CoWoS capacity target for 2027 will reach 2 million wafers. However, due to bottlenecks in WoS and other small components, actual CoWoS output in 2027 may only be 1.8 million wafers.

> ForecastsNVIDIA will still account for about 55% of TSMC's CoWoS capacity in 2027, while Google's TPU market share will soar from 23% to 27% by 2026. This "battle of the giants" will severely squeeze available capacity for other players, such as $AMD(AMD.US) and Amazon

$Intel(INTC.US)'s EMIB-T technology is gradually becoming the biggest potential threat to TSMC's dominance in advanced packaging. Google's next-generation TPU v9 project is collaborating with MediaTek and plans to adopt Intel's EMIB-T packaging solution. Forward this message to those who are skeptical about the AI/semiconductor industry. Which stock do you think will be the biggest beneficiary of this long-term bottleneck? (Source)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.