SATS | Maybank Research | BUY | Target Price S$5.09 | 01 Jul 2026

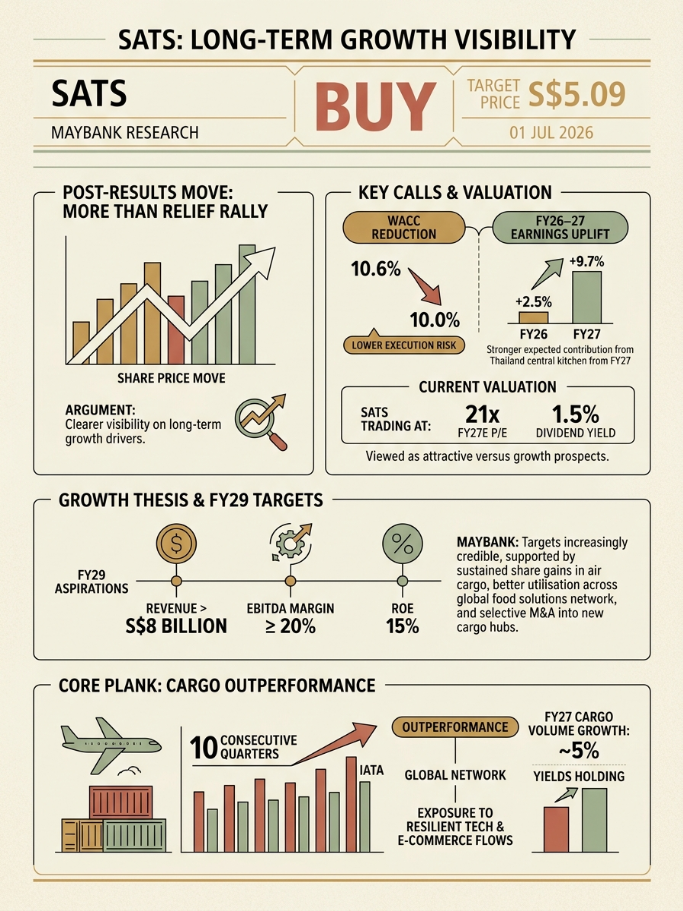

Maybank keeps SATS at BUY, raises its DCF-based target price to S$5.09, and argues the post-results share price move is more than a short-term relief rally due to clearer visibility on long-term growth drivers.

Key calls and valuation

The analysts lower WACC from 10.6% to 10.0% as they see lower execution risk, and lift FY26–27 earnings by 2.5% and 9.7% respectively, mainly on stronger expected contribution from the Thailand central kitchen from FY27.

At the time of writing, they highlight SATS is trading at about 21x FY27E P/E with a 1.5% dividend yield, which they view as attractive versus growth prospects.

Recommendation is BUY with a raised target price of S$5.09, based on DCF.

Growth thesis and FY29 targets

Management reiterates FY29 aspirations of revenue above S$8 billion, EBITDA margin of at least 20%, and ROE of 15%.

Maybank sees these targets as increasingly credible, supported by: sustained share gains in air cargo, better utilisation across the global food solutions network, and selective M&A into new cargo hubs.

A core plank is cargo, where SATS’ volumes have outperformed IATA for 10 consecutive quarters, aided by its global network and exposure to resilient tech and e‑commerce flows; Maybank projects about 5% cargo volume growth in FY27 with yields holding.

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.